Equity valuations resist running with the bulls

Blog post

August 23, 2018

The U.S. bull market is now the longest in history, leading the way for strong global equity returns over the 10 years since the financial crisis. What does this mean for valuations? We found that while they are high, they have not reached extreme levels. What's more, there are distinct valuation characteristics across regions, sectors and factors that may create potential investment opportunities.

SOME, BUT NOT ALL, REGIONS LOOK EXPENSIVE

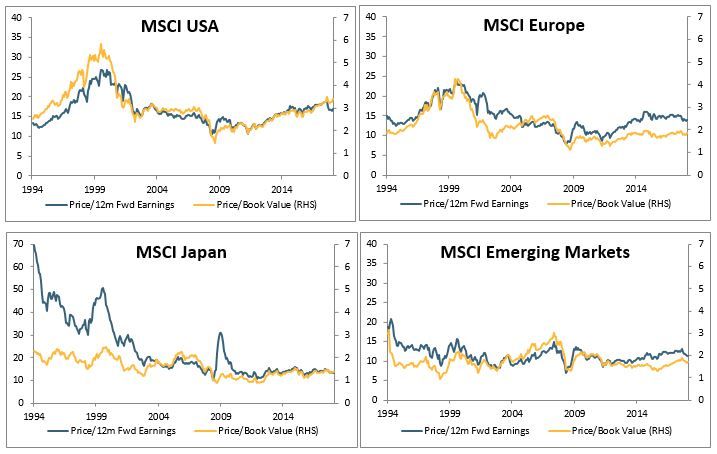

Strong equity performance has resulted in elevated valuations for the broader markets, but the valuations do not appear extreme when we look at index valuations since 1994.

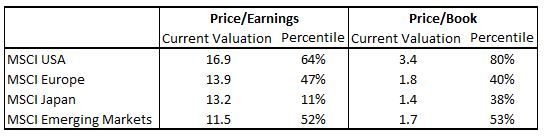

When we look at where current valuations for each region, as of the end of July 2018, rank within its own history, the U.S. seems overvalued with current valuations in the 64th percentile on a price/earnings basis and the 80th for price/book; emerging markets and Europe remain in the 50s and 40s ranges, respectively. Japan, in contrast, appears relatively undervalued on both valuation measures.

VALUATIONS OF DEVELOPED AND EMERGING MARKETS

Source: MSCI

Percentile of the Current Valuations

EXTREME VALUATIONS FOUND IN ONLY A HANDFUL OF SECTORS

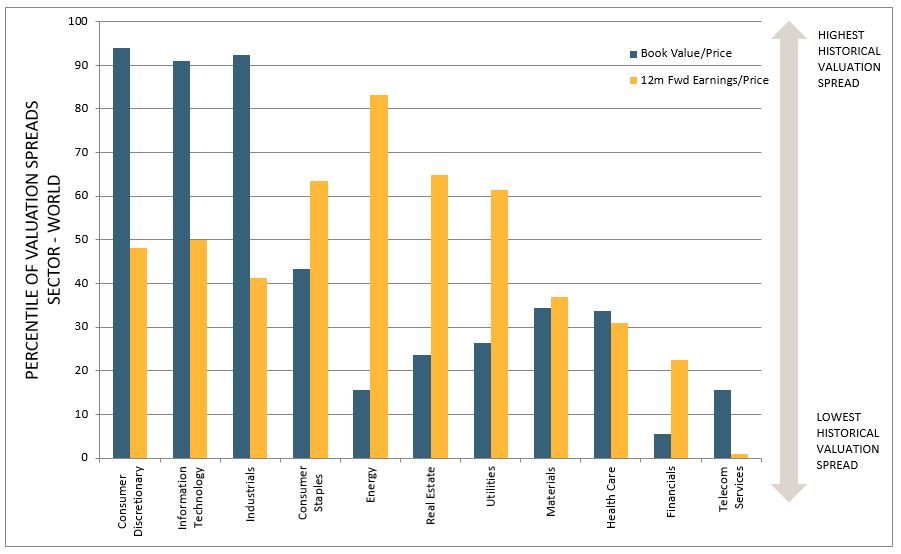

When looking at the sector valuations, we calculate the differential of the sector valuations (12m forward earnings yield and book value yield) and those of the broader market to compute the relative valuations. We then compare the relative valuations to the sector's history to evaluate if it has been over/under valued.

In the next exhibit, we show the percentile rank of the current valuations for MSCI World GICS® sector indexes using monthly data since June 1994 (except for real estate where data is available from April 2003) through July 20181. We see a significant disparity across the sector relative valuations. While sectors, such as telecom services and financials are close to their lowest relative earnings/price and book value/price valuations, the information technology, consumer discretionary and industrials sectors are all close to their peak relative valuations on a book value/price basis. Though not indicative of future results, Information Technology significantly outperformed broader market measures over last five years, pushing its weight in developed markets to 20% -- the highest since the Tech bubble when it peaked at 26%.

In emerging markets, consumer staples and consumer discretionary were the most "expensive" sectors while financials and real estate were the "cheapest" in terms of valuation.

PERCENTILE OF CURRENT RELATIVE VALUATIONS OF DEVELOPED MARKET EQUITY SECTORS

CYCLICAL FACTORS APPEARED CHEAP VERSUS DEFENSIVE ONES

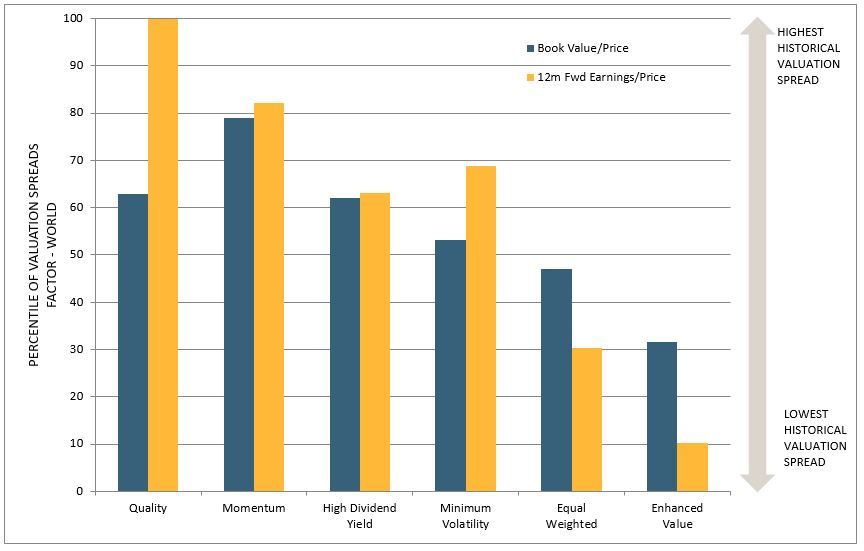

Similar to the relative valuations of sectors, when we look at the percentile of relative valuation of factors in the developed markets since December 1997, there emerges a clear distinction between the defensive and cyclical factors. Defensive factors, such as quality, high dividend yield and minimum volatility are currently priced at expensive relative valuations, while cyclical factors, such as enhanced value and equal weighted are valued cheaply.

Given investor concerns about the sustainability of global economic growth and heightened geopolitical risks, it's not surprising that quality has been outperforming; high-quality companies are trading at premium valuations. The MSCI World Momentum Index is currently overweight in relatively expensive sectors, such as information technology and consumer discretionary and priced close to its peak relative valuations. Momentum's high valuations can be attributed to recent outperformance, as well as to the nature of the factor itself. That is, it can swing rather sharply as it follows outperforming stocks and sectors. For example, the MSCI World Momentum Index was cheaply valued as late as November 2017. We saw a similar distinction in factor valuations in emerging markets, but the difference in relative valuations for the cyclical and defensive factors was not as wide.

PERCENTILE OF CURRENT RELATIVE VALUATIONS OF FACTORS IN DEVELOPED MARKETS

Source: MSCI Factor Indexes

To conclude, market valuations across the globe are high, but have still not reached nosebleed territory on a historical basis. Within the broader equity markets, we saw a significant dispersion in valuations, likely offering investors cheaper investment themes across different regions, sectors and factors.

The author thanks Jean-Maurice Ladure for his contribution to this post.

1 GICS is the global industry classification standard jointly developed by MSCI and Standard & Poor's.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.