European securitization at the regulatory crossroads

Blog post

June 17, 2019

- In Q1 2019, firms issued only EUR 32.4 billion of securitized products throughout the European continent — a decrease of 63% from Q4 2018.

- The drop-off occurred as firms adjusted to the new regulatory demand that securitizations comply with the European Banking Authority's January 2019 guidelines on the simple, transparent and standardized (STS) criteria.

- The EU's reform efforts remain incomplete. Many important technical standards — which will govern the specifics of implementing the STS criteria and other securitization reforms — have not been finalized yet. Investors worldwide may want to consider this regulatory uncertainty.

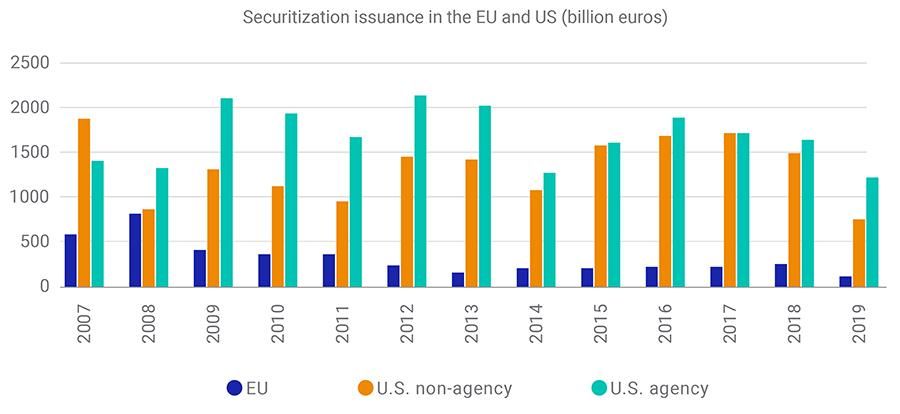

The EU and US: A tale of two post-crisis markets

The recent European drop-off represents a continuation of longer-term trends in the European and U.S. securitization markets. The EU's 2018 issuance of EUR 269 billion was significantly below its peak issuance of EUR 819 billion in 2008.3 By contrast, the U.S. securitization market has generally recovered to pre-crisis levels, albeit with a different asset mix. For example, increased U.S. issuance in consumer asset-backed securities (ABS) and collateralized-loan obligations (CLOs) has replaced the diminished volume of nonagency mortgage securitizations.

Source: SIFMA, AFME. The 2019 numbers are annualized Q1 2019 numbers.

The global financial crisis was a securitization crisis

The global financial crisis of 2007-2008 tarnished the reputation of the securitization market. The crisis was initiated by the performance of U.S. subprime mortgage securitizations. In fact, the most acute default rates experienced by all securitization sectors occurred in U.S. residential mortgage-backed securities (RMBS), whose overall default rates reached 30%. This figure was much higher than the default rate of European securitized products over the same stretch of time, as shown in the exhibit below.

US RMBS defaults spiked during the crisis

Deal Type | US Issuance (USD Billions) | US total Default % | Unnamed: 3 | EU Issuance (EUR Billions) | EU total Default % |

|---|---|---|---|---|---|

Deal Type RMBS | US Issuance (USD Billions) 407 | US total Default % 32.9% | Unnamed: 3 None | EU Issuance (EUR Billions) 48 | EU total Default % 0.65% |

Deal Type Auto ABS | US Issuance (USD Billions) 75 | US total Default % 10.2% | Unnamed: 3 None | EU Issuance (EUR Billions) 4 | EU total Default % 0.50% |

Source: Intex Solutions. The default rates are calculated for U.S. and EU securitizations issued in 2007.

Securitization reforms take center stage in Europe

Recognizing securitization's importance in providing credit to business and consumers, both the U.S. and EU issued a series of post-crisis reforms of their respective markets. The U.S. securitization reforms covered a wide range of issues, including new accounting and disclosure rules, capital and liquidity requirements, risk-retention rules for underwriters and rating-agency reforms.

In addition to the EBA's new STS standards, the EU's broader securitization reforms increased the requirements for due diligence, risk retention by underwriters and transparency and disclosure across all securitization markets. They created a new securitization class that complies with the concept of STS ABS. The new STS securitization criteria also require tighter underwriting and more homogenous collateral, as well as a system of registration and supervision and reporting to repositories of loan-level data. It explicitly rules out opaque and risky structures, such as synthetic securitization, securitization special-purpose entities (SSPEs) with actively managed portfolios, commercial mortgage-backed securities and self-verified RMBS, re-securitizations and securitizations that rely on asset sales.

The uncertain future of European securitization

The EU's reform efforts remain incomplete. Many important technical standards — which will govern the specifics of implementing the STS criteria and other securitization reforms — have not been finalized yet. But AFME has reported progress: Several new transactions in the pipeline aim to be compliant with the new STS regime.

AFME's soon-to-be-released second-quarter issuance numbers will shed light on firms' success in complying with the STS criteria and other EU standards — and maybe offer a glimpse of the future of European securitization.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1“Final Report on Guidelines on the STS criteria for non-ABCP securitization” and “Final report on Guidelines on the STS criteria for ABCP securitization.” European Banking Authority, Dec. 12, 2018.2“AFME Securitisation: Q1 2019.” Association for Financial Markets in Europe, May 9, 2019.3“Q1 2019 Quarterly Results.” Vale.com, May 9, 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.