Evaluating Emerging-Market Stocks through a Governance Lens

Blog post

February 21, 2019

Historically, emerging-market stocks are perceived to have lower governance standards than their developed-market counterparts. They are frequently less transparent, requiring investors to dig deep for relevant data. Some emerging-market companies also may disadvantage minority shareholders, particularly those firms dominated by controlling shareholders and those that are state-owned enterprises (SOEs). How can institutional investors address these issues?

We have previously discussed how active equity managers can integrate environmental, social and governance (ESG) data and ratings into the investment process for developed-market portfolios. Now, we extend this approach to emerging-market portfolios, particularly focusing on governance issues. It's not easy, as some companies may not make detailed company-level information readily accessible to all investors. Some elements for integration may include shareholder-manager alignment, voting rights, compensation incentives and accuracy of financial statements.

What are the key governance characteristics in emerging markets?

Identifying management quality within emerging markets is becoming a key trend in ESG investing, as we noted last year in "2018 ESG Trends to Watch." Using MSCI ESG Research's corporate governance scores — which evaluate firms across four main criteria, namely board, ownership and control, pay and accounting practices — we can assess how emerging-market companies, in general, differed from developed-market firms. A company's corporate governance assessment may help investors gain insight into how well the company's governance affects the interests of its minority investors.

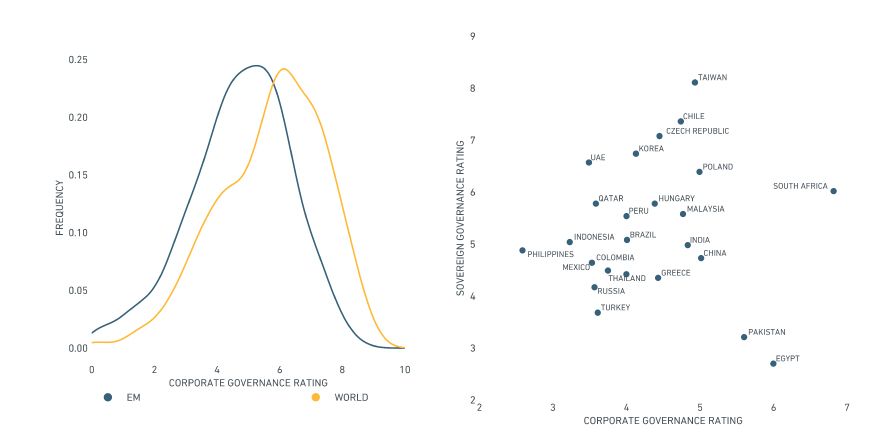

A look at our ratings across MSCI ACWI at the end of last year shows that firms in emerging markets (represented by the MSCI Emerging Markets Index), on average, scored lower on governance than their developed-market counterparts (represented by the MSCI World Index), as illustrated in the left panel of the exhibit below. However, within Emerging Markets, there are a number of firms that achieved higher scores.

Emerging markets scored lower on governance criteria than developed markets

Corporate governance scores as of December 2018. Sovereign governance scores as of October 2018. The average corporate governance scores across all firms in a country is shown in the right plot.

The right plot illustrates that the wide distribution in governance across emerging-market companies is closely linked to a firm's country of domicile. MSCI ESG Research's Sovereign Governance Ratings measure country-level risks. Firms located in countries with stronger regulatory institutions, rule of law or contract enforcement tended to also have stronger corporate governance profiles.

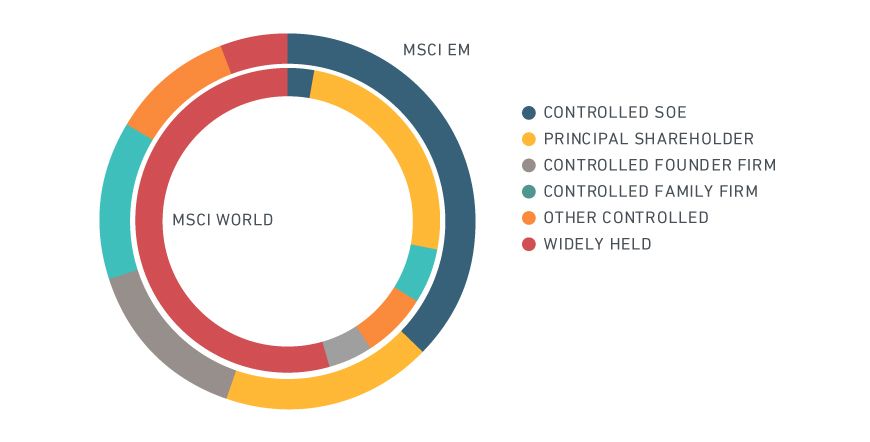

A second characteristic that distinguished emerging- from developed-market firms was ownership structure.1 The majority of emerging-market firms by weight were either SOEs or had a single principal shareholder. In contrast, the majority of developed-market firms by weight were considered widely held, with a dispersed ownership base. These differences are shown in the outer and inner rings, respectively, in the exhibit below.

Emerging-market firms (by weight) were majority state-owned or had a single principal shareholder

Ownership structure and market weights as of December 2018

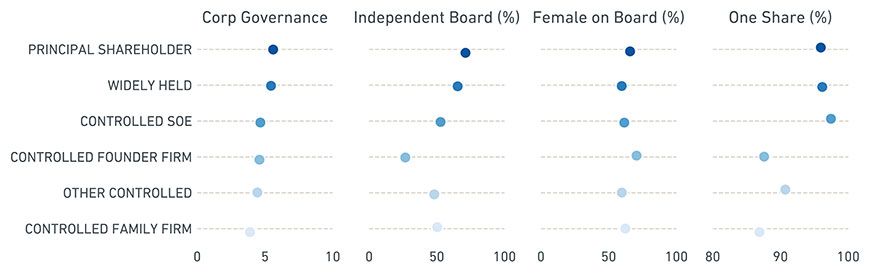

Ownership structure matters in the context of the governance scores because of its relationship to a firm's governance characteristics. In the exhibit below, we group firms in the MSCI Emerging Markets Index based on their ownership structure. The first column is the overall corporate governance rating, while the remaining are selected measures drawn from a firm's board and ownership practices.

Ownership structure for firms within the MSCI Emerging Markets Index

All ratings as of December 2018. Percentages are the proportion of firms in each ownership category that meet the criteria.

Firms controlled by founders, a family or another large shareholder ("other") tended to have a lower overall corporate governance score, with lower levels of board independence and more deviations from a one-share, one-vote shareholder policy. As we noted in "Ownership Forms & Governance Control," the primary risk to minority investors in these types of firms were related party transactions and cross-shareholding structures.

How have SOEs fared?

The answer is mixed. The possibility of misalignment between the strategic interests of the state and those of minority shareholders remained a key governance risk in SOEs. Yet equity investments in SOEs generally carried lower risk than the wider market as they enjoyed the explicit backing of the government. They also have tended to offer relatively higher dividend yields — particularly in China, following recent reform initiatives that increased dividend payouts by SOEs.

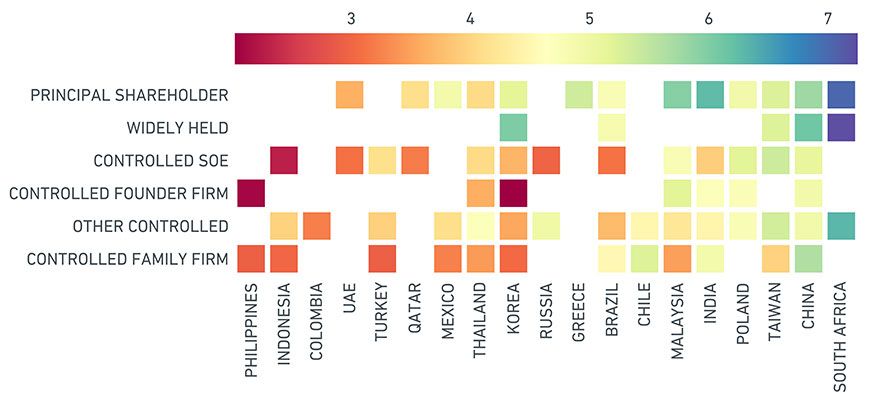

Let's bring it together by examining the relationship between governance, ownership structure and country. Specifically, within an ownership structure, are there certain countries whose firms have displayed higher governance ratings? The exhibit below shows firms' MSCI ESG Research governance scores based on their country of domicile and ownership structure.

Take the example of controlled family firms. We saw earlier that these firms scored lowest in overall governance scores. One surprise is that family firms in China were considered relatively well-governed. Few of China's family firms were a part of extensive family conglomerates, such as in India or Korea. As a result, Chinese family firms were less often flagged for either having an entrenched board (a board with long tenure) or overboarding (a director who sits on multiple boards).

Governance scores based on country and ownership structure

Values shown are the average corporate governance scores within each ownership type and country of domicile. Only ownership/country pairs with at least three firms are shown.

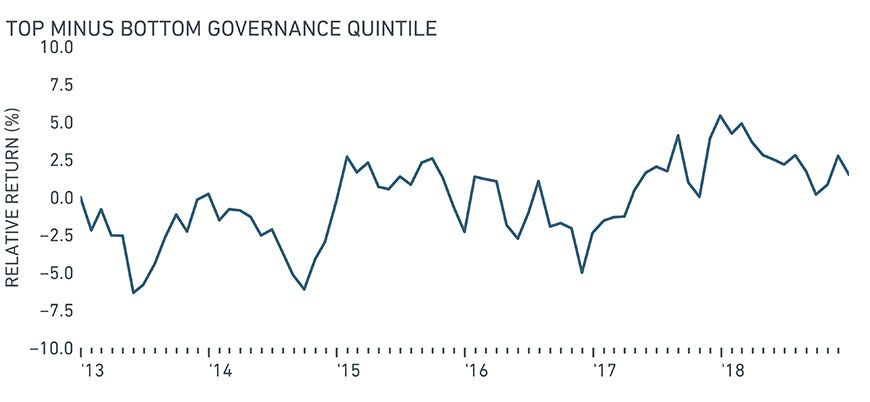

Last, we look at whether governance has affected returns. The final exhibit shows the return difference between the highest- and lowest-rated firms in emerging markets. In our backtest, higher-rated firms outperformed lower-rated firms since 2013.2 While not shown, a return attribution indicates that top-rated firms' higher yields and lower stock-level volatility were two key drivers of the outperformance.

Return differences between highest- and lowest-rated EM companies

Returns are gross in USD and relative to the MSCI EM index from January 2013 to December 2018. We choose 2013 as a start date, as complete ratings coverage of the MSCI EM index began in 2013. Quintiles are formed using the Governance Pillar Score for each stock. The Governance Pillar Score is a composite of a firm's corporate governance and corporate behavior score. Quintiles contain an equal number of stocks that are equally weighted and rebalanced semi-annually.

Active managers looking to incorporate governance into their portfolios may wish to consider using a reweighting approach, which we explained last year. This approach aims to preserve the manager's investment style and holdings, while tilting toward firms with higher governance ratings. However, this came at the expense of tracking error to the original strategy. Indexes can also employ a similar reweighting approach, as we discussed in "Raising Minimum Governance Standards."

Emerging-market investors have a growing menu of options to make informed investment decisions. Although corporate governance is just one component of a firm's overall ESG profile, it addresses both ownership risk and country risk — helpful criteria for active and index-based investors alike.

The authors thank Ric Marshall, Michael Cheng and Alan Brett for their contributions to this post.

Further Reading

1MSCI defines controlled SOEs as companies that have one or more sovereign entity investors controlling 30% or more of the company’s total voting power; principal shareholder companies as those with one or more investors that hold at least 10% but not more than 30% of the company’s total voting power; controlled founder firms as having one or more company founders holding 30% or more of the company’s total voting power and also serving as the company’s chief executive officer or chairman; controlled family firms as those having one or more family groups holding 30% or more of the company’s total voting power; other controlled companies as those with one or more investors, not identified as either company founders or representing family interests, holding a combined voting block of 30% or more; and widely held companies as those lacking any single investor holding 10% or more of the company’s total voting power.2This report contains analysis of historical data, which includes hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.