Exploring the ‘what ifs?’ in real estate

Blog post

October 29, 2019

- The opacity of real estate markets and the wide spectrum of potential outcomes makes it hard to understand performance. Unlike equity markets, it is typically not possible to passively track the private real estate market.

- Running historical "what-if" analysis may help institutional investors understand how different choices could have impacted outcomes.

- Investors may also consider using benchmarks and weighted contributions to form a better understanding of how much of their relative performance is attributable to certain assets or groups of assets.

A wide range of possible outcomes

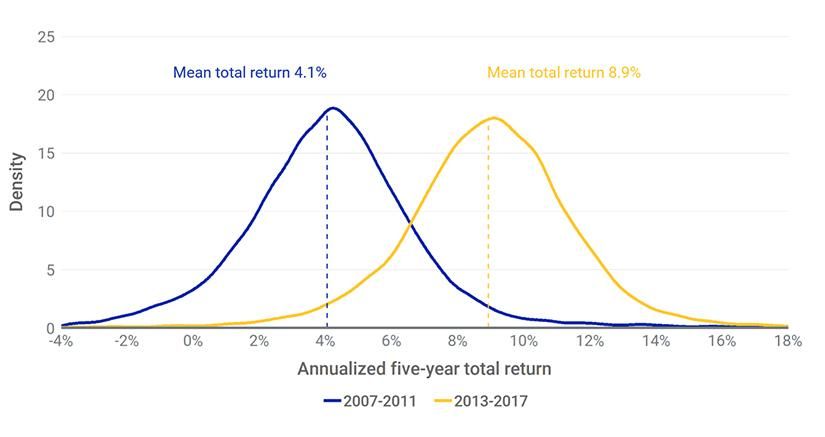

To illustrate the importance of cycles, and the broad range of possible outcomes, we have calculated the annualized performance of 20,000 simulated multinational office portfolios in local-currency terms over two separate five-year periods.2 The exhibit below illustrates the impact of cycles, with the expected total return during the 2007-2011 period (encompassing the global financial crisis) of 4.1% per year, which was 480 basis points (bps) lower than the 8.9% annual average total return during the 2013-2017 period. The chart also shows the wide range of possible outcomes within each period — demonstrating how context may play a role in analysis. For instance, a portfolio that achieved a 7% annual total return in the 2007-2011 period would have considerably outperformed the average portfolio, falling into the 89th percentile. A 7% annual total return in the 2013-2017 period would have ranked in only the 19th percentile, thus considerably underperforming the average

The impact of cycles: Outcomes varied widely for simulated multinational office portfolios

Source: MSCI Global Annual Property Index. Based on the performance of 20,000 simulated multinational office portfolios in local-currency terms.

Unlike equity markets, it is typically not possible to passively track the private real estate market. While investors may choose to use diversification to lower their expected tracking error from the benchmark, the potential for deviation remains high. This cyclical variability and the wide range of performance outcomes can be challenging for real estate investors seeking to evaluate portfolio performance.

What-if analysis provides context

Using the same data, we can use a simplified example to demonstrate how investors can use what-if analysis to gain a sense for how the exclusion of certain assets may have affected hypothetical historical performance. For example, removing U.K. office assets from the simulations increased the expected total return for 2007-2011 by 160 bps to 5.7% annually, as the financial crisis hurt U.K. offices more than it did those in the other 15 countries included in this analysis. By contrast, excluding U.K. assets in the 2013-2017 period — when U.K. office market performance was much stronger — lowered the expected total return by 90 bps to 8.0% a year.

Investors can use a similar what-if analysis approach to a real-life portfolio. For instance, investors could follow a rules-based approach to filter out assets based on attributes like asset age, property type, yield or other characteristics and gain insight into how these variables contributed to portfolio performance.

All assets are not created equal

Investors may also use a benchmark to measure their portfolios' performance relative to the broader market and gain perspective on whether the portfolios out- or underperformed — and by how much. Breaking the relative return down to segment — or even asset levels — can then be used to identify those parts of the portfolio that helped or hurt relative performance.

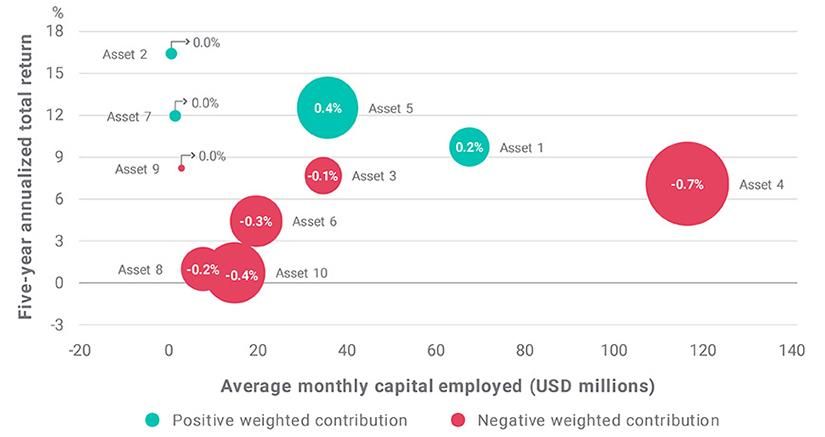

This can be illustrated using one of the simulated office portfolios. This particular portfolio, which comprised 10 assets in the 2013-2017 period, underperformed its benchmark by 120 bps, achieving an annualized total return of 7.8%. The assets' individual performance ranged between 16.5% and 0.8% a year.

We might assume that the best- and worst-performing assets had the biggest impact on the portfolio's performance, but was that the case? When we examine the weighted contributions to relative return, top-performing Asset 2 actually had a minimal impact on the portfolio's relative return because of its relatively small value and therefore small weight. Asset 5 had the most positive impact on the overall portfolio's relative performance, due to its larger weight. At the other end of the spectrum, worst-performing Asset 10 did not have as big an impact as Asset 4 — which underperformed less, but by virtue of its larger weight, was the biggest drag on overall relative performance.

Assets' impact on relative performance

This simple hypothetical example demonstrates how investors may have used weighted contributions to identify sources of strength and weakness in the portfolio.

Looking backwards before going forwards

While real estate is an opaque asset class, what-if analysis and analyzing portfolio returns based on the weighted contributions of segments or individual assets may help investors get a better sense of how their performance measured up against the range of possible outcomes and how it was driven by different variables.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1From an exchange on the now-defunct anonymous messaging app Yik Yak.2The data used in this analysis comes from the MSCI Global Annual Property Index. A sample of 9,721 office assets from 16 national markets was used with random selection to create portfolios of between one and 30 assets. More details on the sample and simulation methodology can be found in Reid, B. ”Risk Reduction and Tracking Error in Small Commercial Real Estate Portfolios.” , October 2019. This report may contain analysis of historical data, which may include hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. The analysis and observations in this report are limited solely to the period of the relevant historical data, backtest or simulation. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.