Factors in Focus: Dynamic short term, strategic long term

Blog post

July 2, 2019

- In Q2 2019, momentum and low volatility outperformed in developed markets. In emerging markets, momentum, yield and value outperformed.

- Heading into Q3, our adaptive multi-factor model showed a mild overweight to low volatility and value, neutral for quality, momentum and size, and a mild underweight to yield, relative to a six-factor equally weighted mix.

- Over the last 10 years, a diversified mix of factor indexes in developed and emerging markets outperformed their respective benchmarks.

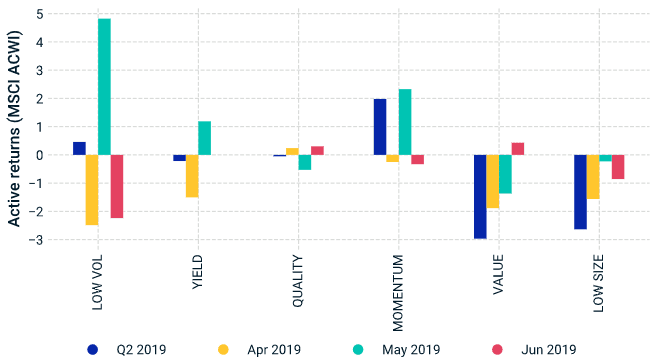

Rotation into momentum and low volatility over Q2

Shows active return (%) performance of the MSCI ACWI Minimum Volatility (USD) Index, MSCI ACWI High Dividend Yield Index, MSCI ACWI Quality Index, MSCI ACWI Momentum Index, MSCI ACWI Enhanced Value Index and MSCI ACWI Equal Weighted Index for second quarter of 2019 and each month, from Mar. 29, 2019 to June 28, 2019.

Equity markets ended the second quarter in positive territory (the MSCI ACWI Index returned +3.8% and the MSCI Emerging Markets Index +0.7%), although investors remained concerned over U.S. trade relations with China and Mexico and over global economic growth. Correction to the China equity market (c. -3.9%) dragged down the performance of the MSCI Emerging Markets Index and the MSCI AC Asia ex Japan Index.

While headline indexes experienced moderate returns, the relative moves in some factors were far from muted. The perfect storm of lower U.S. interest rates, lower inflation and growth may have had a negative impact on the value factor, despite a significant valuation gap relative to the rest of the market. The MSCI ACWI Enhanced Value Index and the MSCI USA Enhanced Value Index underperformed their parent indexes by 7.4% and 5.1%, respectively, in the first half of the year, including four consecutive declining months. Heightened market volatility in May favored defensive factors — notably, low volatility and yield. Momentum, which recently showed defensive characteristics, also outperformed its parent, the MSCI ACWI Index. In June, patterns in low volatility, momentum, quality and value reversed moderately (see exhibit above).

Value factor fell along with US rates and inflation

Shows the 10-year constant-maturity Treasury rate, 10-year breakeven inflation rate and active return (%) performance of the MSCI USA Enhanced Value Index from June 29, 2018 to June 20, 2019.

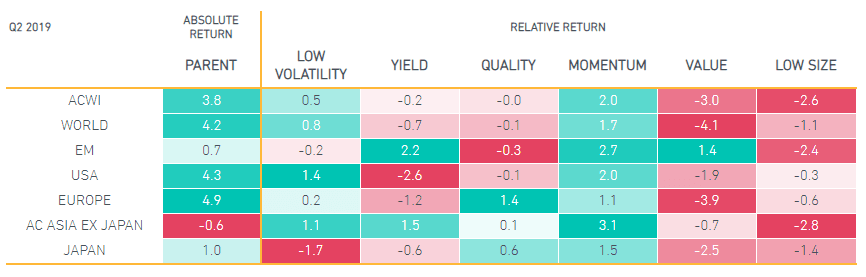

On a regional basis, low volatility and momentum outperformed their respective parents, the MSCI USA, MSCI Europe and MSCI AC Asia ex Japan standard indexes. In contrast to developed markets, factor performance in emerging markets was mixed, with yield, momentum and value outperforming.

"Momentum everywhere" in Q2

Shows regional variations of the MSCI ACWI Minimum Volatility (USD) Index, MSCI ACWI High Dividend Yield Index, MSCI ACWI Quality Index, MSCI ACWI Momentum Index, MSCI ACWI Enhanced Value Index and MSCI ACWI Equal Weighted Index from March 29, 2019 to June 28, 2019.

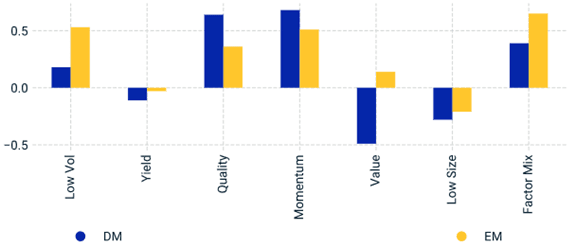

10-year factor performance — diversification paid off

The recent relative drawdowns of the value and low-size factors have led some investors to question the sustainability of factors providing outperformance. Over the last 10 years, developed markets were characterized by a long cycle of growth, prolonged low rates and low inflation and low levels of market volatility punctuated by short-lived volatility spikes. Momentum and defensive factors, particularly low volatility and quality, outperformed; and cyclical factors, such as value and low size, underperformed (while value outperformed in emerging markets).

While historical patterns showed certain individual factors underperformed for several years, a diversified mix of all six factors, based on simple equal-weighting, outperformed for the full period in both developed and emerging markets.

A diversified mix of factor indexes outperformed over the long term

Data from May 31, 2009, to May 31, 2019

What about the third quarter?

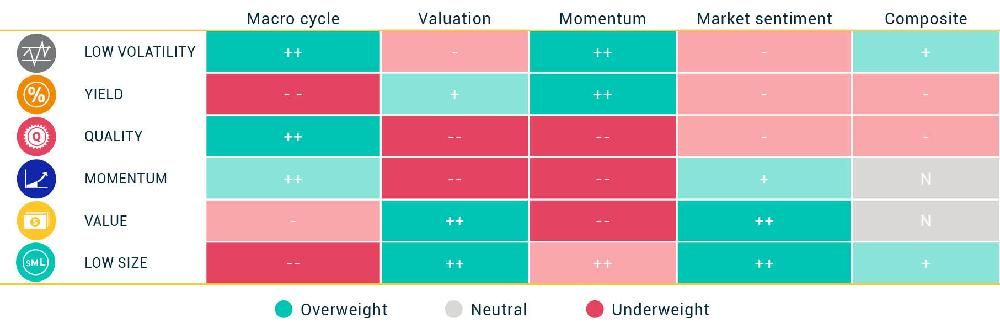

Following the continued rotation in factor returns in Q2 2019, we revisited our model for adaptive multi-factor allocation, which is centered around adapting factor allocations based on four pillars: macro cycle, valuations, momentum and market sentiment.

As of June 28, 2019, our adaptive multi-factor model showed the following exposures across the four pillars, with all but valuation changing from March 31, 2019:

- Macro cycle indicated a bias toward a "slowdown/contraction" and overweighted low volatility, quality and value, based on the Chicago National Activity Index, the Federal Reserve Bank of Philadelphia ADS Index and the Purchasing Managers' Index.

- Valuation overweighted value, low size and yield, based on the valuation gap compared to an equal-weighted factor mix in the context of 40 years of a factor's history.

- Momentum selected momentum, quality and low volatility, based on the last six months' relative performance.

- Market sentiment showed a mild overweight to size, momentum and value, based on contained credit spreads and an upward sloping Cboe Volatility Index (VIX) term structure at the time of reference.

Exposures from MSCI's adaptive multi-factor allocation model

Data as of June 28, 2019. Note: Indicators highlight overweight and underweight index positions relative to an equal-weight six-factor index mix. "++" denotes a strong overweight, "+" a mild overweight, "N" neutral, "-" mild underweight, "--" strong underweight.

While momentum turned out to be the leading factor performer across developed and emerging markets for Q2 2019, our adaptive multi-factor model had a different stance heading into the third quarter, as indicated by the exhibit above.

Factors in Focus will continue to report on the markets throughout 2019.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.