Factors in Focus: Impact of Inflation on Style Factors

- Global equities continued to rally, and many regions reached all-time highs in the third quarter. Within equities, high beta, growth, quality and momentum outperformed. For USD and EUR investment-grade corporate bonds, it was carry and value.

- As investors think about inflation scenarios, we revisit factor performance over various inflationary periods. Quality and momentum were less sensitive to inflation. Growth and low volatility had negative and positive sensitivity, respectively.

- As we enter the final quarter of 2020, MSCI's adaptive multi-factor model pointed to an overweight of low size, value and momentum and an underweight of quality, low volatility and yield.

Pure Factor Performance in Q3 2020

Factor performance of MSCI Global Equity Model (GEM+ESG) pure factors from June 30, 2020, to Sept. 30, 2020.

In last quarter's Factors in Focus, we highlighted the persistence in "style-factor momentum" among factor indexes, and this trend continued into Q3. From an MSCI ACWI perspective, factor-index performance showed a similar pattern to the previous quarter with high beta, growth, momentum and quality all delivering positive active returns, while low vol, yield and value continued to lag behind. Within regions, we continued to see variations, with positive active returns in value in emerging markets (EM), Asia ex Japan, and low size in Europe.

Over September, we saw some signs of a reversal in global factors as market volatility rebased a notch higher. The monotonic shift in monthly returns for momentum and value in the chart above seems to suggest the gradual shift from momentum into value.

High Volatility Led Across All Regions

Loading chart...

Please wait.

The table shows regional variations of the MSCI Minimum Volatility Index (USD), MSCI High Dividend Yield Index, MSCI Quality Index, MSCI Momentum Index, MSCI Enhanced Value Index, MSCI Equal Weighted Index, MSCI Growth Target Index, MSCI USD IG Low Risk Corporate Bond Index, MSCI USD IG Carry Corporate Bond, MSCI USD IG Quality Corporate Bond, MSCI USD IG Value Corporate Bond Index and MSCI EUR IG Low Size Corporate Bond Index, from June 30, 2020, to Sept. 30, 2020. All the EUR IG Corp Bond returns are in EUR and not USD. The bar chart shows the active returns of the same indexes, by region, for each of the months in the quarter as well as the full quarter. Excess returns for bond indexes were computed by subtracting the duration-matched U.S. Treasury/German Bund returns from the total returns, before including any transaction-related costs of the index over the corresponding period.

Credit Factors' Performance in Q3

The MSCI USD and EUR Investment Grade (IG) Corporate Bond Indexes continued their rally from last quarter, supported by a 1.1% and 1.9% respective spread return (in excess of their duration-matched U.S. Treasury/German Bund returns). Among corporate-bond factor indexes, procyclical factors outperformed, while defensive factors lagged.

Within USD and EUR investment-grade bonds, carry continued its upward trend and outperformed the parent index by 1.8% and 0.3%, respectively, on an excess-return basis. Within USD (EUR) the value and low-size factors also outperformed by 0.6% (0.1%) and 0.6% (0.1%), respectively. Defensive factors, characterized by issuers with shorter durations and stronger credit ratings, fared less well in the recovery — within USD (EUR) the low-risk factor underperformed by 0.6% (0.4%) and quality by 0.4% (0.3%). Low-quality credit may have outperformed higher quality due to pledges from central banks to purchase corporate bonds and dissipating market risk. In contrast to equities, where the quality factor could be reflecting higher upside risks, the outperformance of weaker credit quality might be reflecting lower downside risks.

A Look Across Sectors

Consumer discretionary outperformed in Q3 as easing of lockdowns and restrictions throughout the world meant things appeared to slowly get back to normal. Technology continued its rally led by the so-called FAAMG stocks in the first two months of Q3, going up 5.2% against the benchmark.1 However, September ended flat for tech with a lot of volatility. Energy saw a drawdown as oil prices leveled off after a very volatile Q2.

Consumer Discretionary Outperformed as Economy Seemed to Get Back to Business

Active returns of MSCI sector indexes vs. the MSCI ACWI Index for Q3 2020.

Q3 Special Focus: Factors in an Inflationary Environment

Since inflation has been below the Fed's newly stated "2% average" for many years, some expected higher inflation (>2%) going forward. On the other hand, actual inflation in the eurozone turned negative in August and the European Central Bank seems to be coming under pressure to manage that. With this backdrop, we revisit how factors have performed in developed markets during various inflationary environments.

The exhibit below shows that growth delivered positive active returns in low-inflation (<2%) environments, and negative active returns in moderate- to high-inflation (<2%) environments. Since investors have expected growth stocks to have higher longer-dated cash flows, and inflationary periods have often been coupled with higher interest rates, this may have led to an inverse relationship. Value stocks, on the other hand, which have often been characterized by stronger prevailing cash flows, have outperformed in high-inflation environments.

For dividend yield, the sensitivity to inflation was mixed; higher inflation, often associated with higher rates, could have muted performance of yield strategies. However, if dividend payouts were linked to inflationary periods, this could have counteracted these effects. Low volatility delivered stronger performance in both moderate- and high-inflation environments, as corporate cash flows might have been positively exposed to inflation. Quality and momentum were less sensitive to inflation and outperformed in all scenarios. An equal-weighted mixture of all the factors diversified away sensitivity to inflation and delivered a positive active return, on average, across the three cases.

Inflation vs. Mean Annual Active returns

All factor indexes are for the MSCI World Index universe. Data for inflation consists of the annual inflation rates for advanced economies published by the International Monetary Fund. The three inflation bins have almost the same number of data points. Analysis is from Dec. 31, 1979, to Dec. 31, 2019.

When considering real rates, both quality and momentum delivered positive active returns in all scenarios. An equal-weighted factor mix also remained unaffected. When real rates have been negative, smaller and growing companies might have found themselves borrowing at a lower rate than their growth in pricing power, leading to outperformance, while low volatility may have tended to be favored by investors with less risk appetite moving from fixed income to equities.

Real Rates vs. Mean Annual Active Returns

All factor indexes are for the MSCI World Index universe. Data for inflation is the annual inflation rates for advanced economies published by the International Monetary Fund. Real rate is defined as the forward-looking 1-year U.S. Treasury rate minus inflation. The three real-rate bins have almost the same number of data points. Time period for analysis is from Dec. 31, 1979, to Dec. 31, 2019.

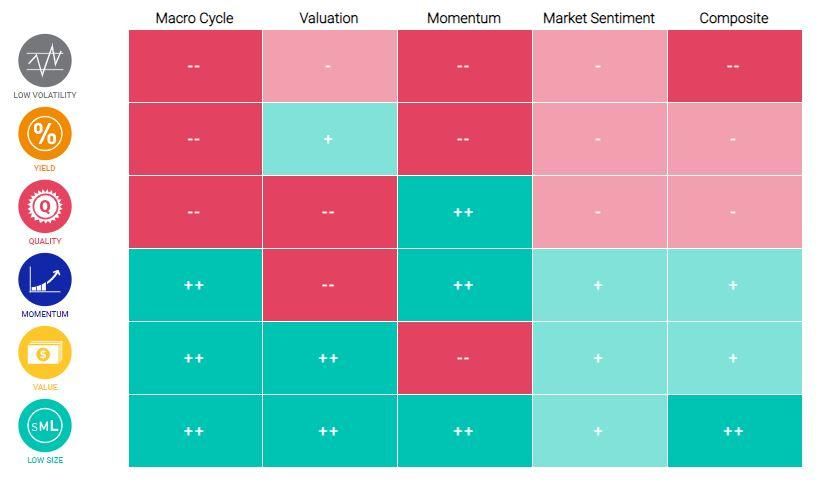

MSCI's Adaptive Multi-Factor Allocation Model Headed into Q3

Our adaptive multi-factor framework is a model designed to analyze decisions about tilting toward factors. Our research has shown that factors were sensitive to changing market conditions and suggests there is value in taking a holistic approach to factor assessment that encompasses the macroeconomic environment, valuations, recent performance trends and risk sentiment.

As of Sept. 30, 2020, our adaptive multi-factor model showed the following exposures across the four pillars:

- The macro-cycle pillar indicated an expansion and thus overweighted value, low size and momentum, based on the Chicago Fed National Activity Index, Federal Reserve Bank of Philadelphia's ADS Index and PMI.

- The valuation pillar overweighted value, low size and yield, based on the valuation gap compared to an equal-weighted factor mix in the context of nearly 30 years of a factor's history.

- The momentum pillar selected momentum, quality and low size, based on the last three months' relative performance.

- The market-sentiment pillar showed a risk-on environment, based on the Cboe Volatility Index® (VIX) term structure and neutral environment based on credit spreads, resulting in an overall mild overweight to momentum, value and low size.

Exposures from MSCI's Adaptive Multi-Factor Allocation Model

As of Sept. 30, 2020. Positive exposures are denoted as + or ++, negative as - or --, neutral as N.

Overall, our adaptive multi-factor model showed a mild overweight to momentum and value and a mild underweight to yield and quality, with low size and low volatility being a large overweight and underweight, respectively.

Further Reading

MSCI Perspectives Podcast: Focusing Factors on Inflation

Factors in Focus: During COVID, inflation and economic uncertainty ahead

Factors — Elements of Performance webpage

Factors in Focus: How Trendy Is Your Style Factor?

Factors in Focus: Risk sentiment and factor dynamics in a crisis

Factors in Focus: Will 2020 vision sharpen exposures?

1FAAMG is an acronym used as shorthand for Facebook Inc., Amazon.com Inc., Apple Inc., Microsoft Corp. and Alphabet Inc.’s Google LLC.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.