Factors in Focus: Risky start. Quality finish.

Blog post

April 2, 2019

In this edition of Factors in Focus, we highlight the fast-moving rotation among factors that continued during Q1 2019, and we present our latest indicators for factor performance from our adaptive multi-factor framework. As we move into Q2 2019, this framework showed a mild overweight allocation to low volatility and low size, a neutral allocation to momentum and value and a mild underweight to yield and quality, relative to a six-factor equally weighted mix.

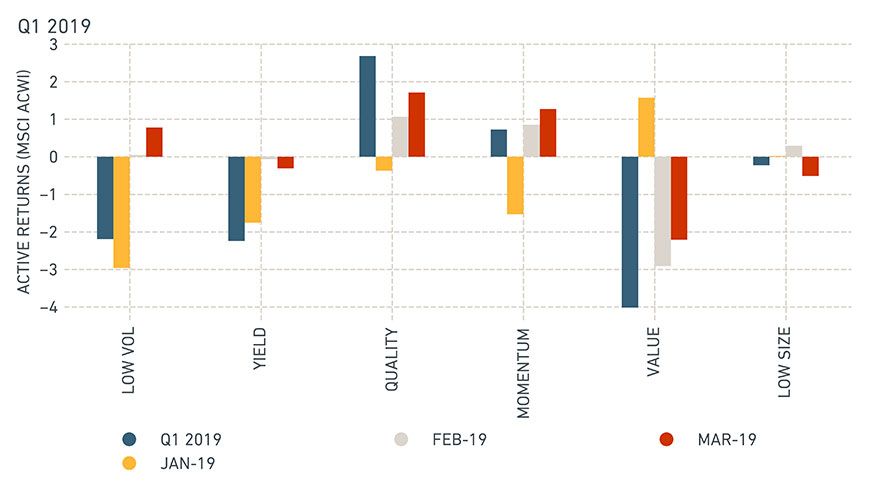

Quality and momentum indexes outperformed in the first quarter

Shows active return (%) performance of the MSCI ACWI Minimum Volatility Index (USD), MSCI ACWI High Dividend Yield Index, MSCI ACWI Quality Index, MSCI ACWI Momentum Index, MSCI ACWI Enhanced Value Index and the MSCI ACWI Equal Weighted Index for each month and full quarter from Dec. 31, 2018, to March 29, 2019.

Equity markets performed well during the first quarter (the MSCI ACWI Index returned 12.3% and the MSCI Emerging Markets Index 10.0%) fueled by optimism that trade agreements between the U.S. and China may be imminent, as well as news that the U.S. Federal Reserve Board paused in relation to any further interest-rate hikes.

Looking at factor performance in the MSCI ACWI Index, investors started the year in risky territory by rotating away from low- to high-volatility stocks and value stocks. However, following the strong equity market gains in January, the value factor reversed sharply, and quality along with momentum outperformed over February and March, in part due to an overweight allocation to technology.

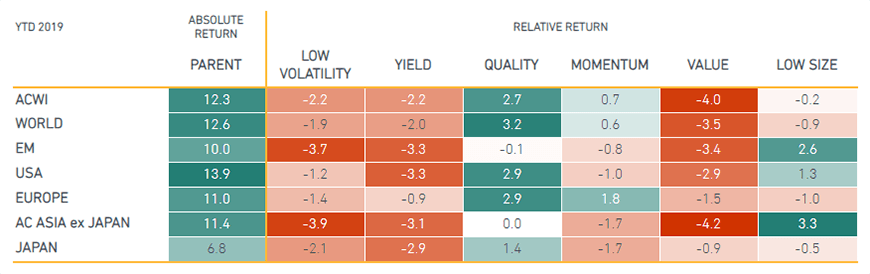

On a regional basis, the size factor's outperformance was more pronounced in emerging markets (EM), and AC Asia ex Japan, whereas quality's outperformance was more evident in developed markets (DM), except Europe.

Quality outperformed in most developed markets; size in emerging markets

Shows regional variations of the MSCI ACWI Minimum Volatility Index (USD), MSCI ACWI High Dividend Yield Index, MSCI ACWI Quality Index, MSCI ACWI Momentum Index, MSCI ACWI Enhanced Value Index and the MSCI ACWI Equal Weighted Index from Dec. 31, 2018, to March 29, 2019.

Momentum showed defensive characteristics YTD

To provide insights on recent market dynamics, we present a clustered correlation analysis of our Global Equity Factor Model – Long Term Horizon (GEMLT) factor returns. Year-to-date, the factor correlations were generally weak, suggesting multi-factor combinations offered strong diversification properties. There were a couple of exceptions. We found momentum displayed defensive characteristics, particularly attaching itself to low beta and low residual-volatility factors, resulting in underperformance over January and outperformance over March. Size had a positive correlation with long-term reversal, suggesting that mid- and small-cap stocks may have bottomed out in global equities and perhaps started to reverse (more evident in EM). We also found some quality factors, such as earnings quality and investment quality, correlated with the growth factor.

Factor correlations were generally weak – with notable exceptions

Loading chart...

Please wait.

Data from Jan. 1, 2019, to March 29, 2019. Correlation calculated on three-day non-overlapping returns.

What about the second quarter?

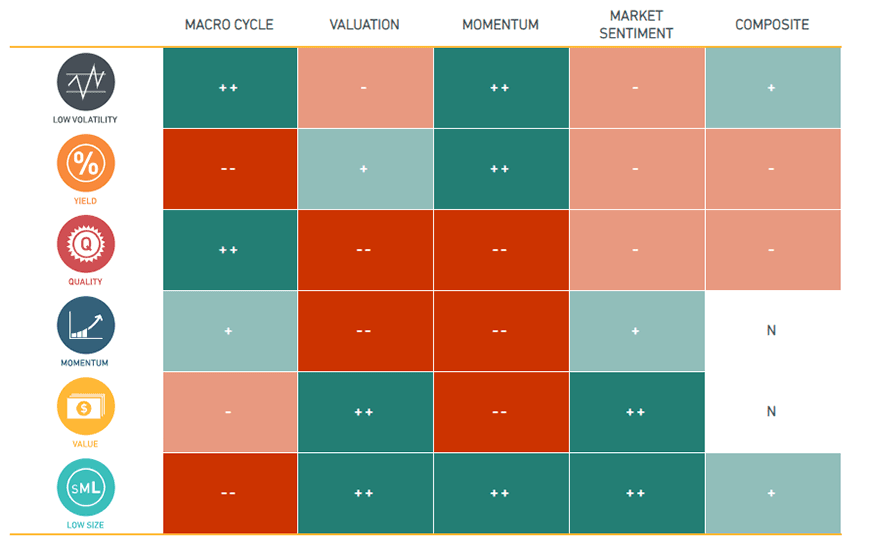

Following the sharp rotation in factor returns in Q1 2019, we revisited our framework for adaptive multi-factor allocation, which is centered around adapting factor allocations based on four pillars: Macro Cycle, Valuations, Momentum and Market Sentiment.

As of March 31, 2019, our adaptive multi-factor framework showed the following exposures across the four pillars, with changes from the exposures at the end of 2018 found most notably in the Market Sentiment pillar:

- Macro Cycle indicated a bias toward a "slowdown" and overweighted low volatility, quality and momentum, based on the Chicago National Activity Index, the Federal Reserve Bank of Philadelphia's ADS Index and the Global Purchasing Managers Index.

- Valuation overweighted value, low size and yield, based on the valuation gap compared to an equal-weighted factor mix in the context of 40 years of a factor's history.

- Momentum selected low volatility, high dividend yield and low size, based on the last six months' relative performance.

- Market Sentiment overweighted momentum, value and size, based on contained credit spreads and an upward sloping CBOE Volatility Index (VIX) term structure at the time of reference.

Exposures from MSCI's adaptive multi-factor allocation framework

As of March 29, 2019. Positive exposures are denoted as + or ++, negative as - or --, neutral as N.

While DM quality and EM size turned out to be the leading factor performers for Q1 2019, at quarter end, our adaptive multi-factor framework had a different stance, as indicated by the exhibit above. Factors in Focus will continue to report on the markets throughout 2019.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.