Factors in Focus: Where’s the Value in Defensive Positioning?

- Global equities were down in Q3 2021, ending a run of five consecutive quarters of positive returns. The MSCI Momentum and MSCI Minimum Volatility Indexes led the performance among the MSCI ACWI Factor Indexes.

- While equity markets have delivered strong returns in the last year, rising concerns of stagflation may give rise to defensive positioning. Among defensive factors, minimum volatility has had historically low valuations relative to quality.

- As economies reopened with increasing numbers of COVID-19 vaccinations "in arms," MSCI's adaptive multi-factor model pointed to an overweight to momentum as of Sept. 30, 2021.

Momentum and Low Residual Volatility Were the Big Winners in Q3 2021

We capture the performance of the drivers of the global equity market using MSCI's Global Equity Model. The exhibit below shows the pure-factor performance over the quarter. Momentum was the best-performing factor, followed by low residual volatility, while liquidity performed the worst.

Pure-Factor Performance in Q3

Performance of the MSCI Global Equity Model (GEM+ESG) pure factors from June 30, 2021, to Sept. 30, 2021.

Factor Performance Varied Across Regional Markets in Q3

As investors looked to position their portfolios defensively, the MSCI Minimum Volatility Indexes outperformed in the MSCI ACWI and MSCI Emerging Markets Indexes, while the MSCI High Dividend Yield and MSCI Enhanced Value Indexes delivered mixed performance across regions. The MSCI Momentum Indexes were positive in developed world markets and negative in emerging markets and all-country (AC) Asia ex Japan.

On a regional basis, the MSCI Emerging Markets and MSCI AC Asia ex Japan Indexes were negatively impacted by China's retracing ~18% during the quarter. However, factor indexes in these regions delivered positive active returns, due to their underweight to China. In particular, low volatility outperformed by 6.2% and 5.1% in EM and AC Asia ex Japan, respectively.

Dispersion in Factor Performance Between Developed and Emerging Markets

Loading chart...

Please wait.

The table shows regional variations of the MSCI Minimum Volatility Index (USD), MSCI High Dividend Yield Index, MSCI Quality Index, MSCI Momentum Index, MSCI Enhanced Value Index, MSCI Equal Weighted Index and MSCI Growth Target Index, from June 30, 2021, to Sept. 30, 2021. The bar chart shows the active returns of the same indexes, by region, for each month in the quarter, as well as for the full quarter.

Yield- and Quality-Factor ETP Flows Were Strongest

The exhibit below shows the USD flows of globally listed exchange-traded products (ETPs) from August 2020 to August 2021. Later in the period, yield-factor ETPs rose to the largest year-to-date inflows, with ~USD 30 billion. Quality also saw some pickup in flows over the last two months.

Global Flows into Factor ETPs (in USD Billions)

All data as of August 2021; defined as each share class of an ETF, as identified by a separate Thomson Reuters Lipper ID. Only primary listings, not cross-listings, are counted. MSCI does not guarantee the accuracy of third-party data.

Defensive Positioning: Quality vs. Minimum Volatility

The macroeconomic uncertainty around inflation and interest rates gave rise to a defensive theme, with minimum volatility doing well over the quarter. As investors looked to position portfolios defensively, we compared the valuation of minimum volatility and quality on a historical basis. The exhibit below shows the ratio of the MSCI Minimum Volatility Index's forward price-to-earnings and price-to-book measures to those of the MSCI Quality Index, for developed and emerging markets. In both cases, minimum volatility had much lower valuations than quality, at levels not seen in nearly 20 years.

Minimum-Volatility Indexes Had Much Lower Valuations than Quality in Developed Markets

Forward price-to-earnings and price-to-book ratios of the MSCI World Minimum Volatility (USD) Index with respect to the MSCI World Quality Index from June 1994 to September 2021.

Emerging Markets' Minimum-Volatility Valuations Were Low Relative to Quality Despite Recent Outperformance

Forward price-to-earnings and price-to-book ratios of the MSCI EM Minimum Volatility (USD) Index with respect to the MSCI EM Quality Index from June 1994 to September 2021.

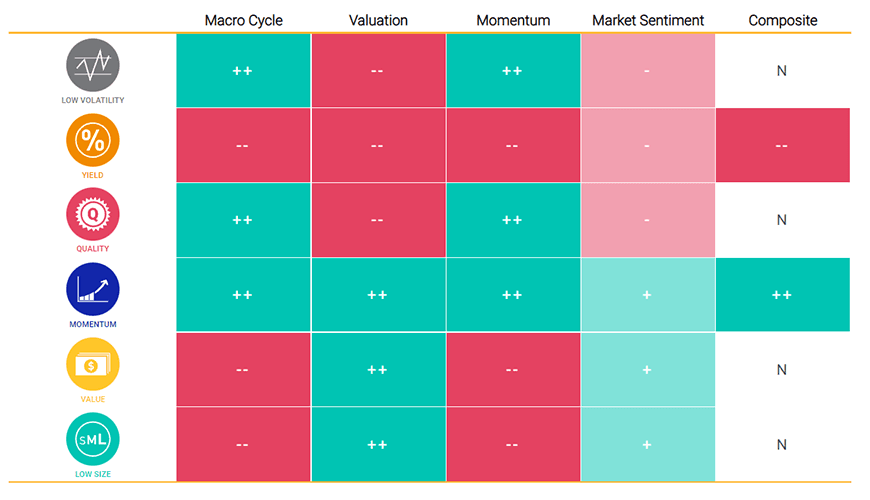

MSCI's Adaptive Multi-Factor Allocation Model

As of Sept. 30, 2021, our adaptive multi-factor model showed the following exposures across the four pillars:

- The macro-cycle pillar indicated an overweight to quality, low volatility and momentum, based on "slowdown" signals from the Chicago Fed National Activity Index, Federal Reserve Bank of Philadelphia's ADS Index and PMI.

- The valuation pillar overweighted low size, value and momentum based on the valuation gap compared to an equal-weighted factor mix in the context of nearly 30 years of a factor's history.

- The momentum pillar selected quality, momentum and low volatility, based on the last three months' relative performance.

- The market-sentiment pillar showed a risk-on environment, based on the Cboe Volatility Index® (VIX) term structure, as well as the neutral environment, based on credit spreads — resulting in an underweight to low volatility, yield and quality and an overweight to momentum, value and low size.

Exposures from MSCI's Adaptive Multi-Factor Allocation Model

As of Sept. 30, 2021. Positive exposures are denoted as + or ++, negative as - or --, neutral as N.

Overall, our adaptive multi-factor model showed an overweight to momentum and an underweight to yield, relative to an equally weighted factor mix.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.