For Real Estate, All Rate Rises are Not Created Equal

Blog post

April 25, 2018

A decade after the global financial crisis, the era of ultra-low interest rates may be drawing to a close. Many real estate investors worry that rising rates could hurt their portfolios. However, our analysis suggests it's the macroeconomic fundamentals driving interest rates, not the rise itself, that are most important.

Why are rates rising? That is the question.

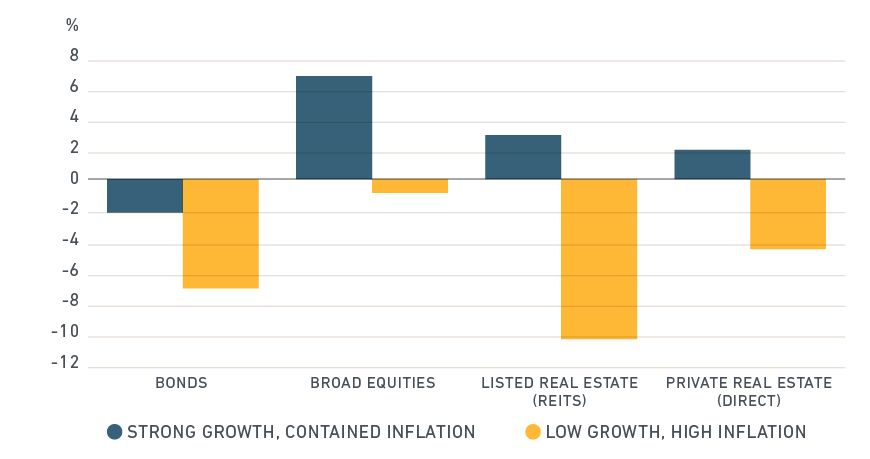

To illustrate the importance of asking "Why?," we used the Barra Integrated Model to explore two forward-looking rate-rise scenarios. In the first, economic growth improves and the central bank makes well-timed rate hikes, which keep inflation within target bands. The second scenario models stagflation, where growth is muted but inflation rises. The central bank raises interest rates to control prices, which causes already weak economic growth to falter, prompting a recession.1

As shown in the exhibit below, in the strong-growth scenario, the impact on bonds is negative, whereas the predicted impact on listed real estate, such as REITS, and private real estate, as well as equities is positive. By contrast, in the low-growth scenario, the predicted performance of real estate mirrors the negative performance of equities and bonds.2

Predicted impact of two rate-rise scenarios

Source: MSCI, Barra Integrated Model

While listed and private real estate move together over longer time periods, their immediate responses to different macro environments and economic shocks can differ substantially.3 As the exhibit above shows, for example, both lose value in the low-growth scenario, but listed real estate investments lose more than twice as much. This is due, in part, to the leveraged nature of REITs4 and the fact that they are more liquid, and therefore easier to rebalance than direct real estate investment.

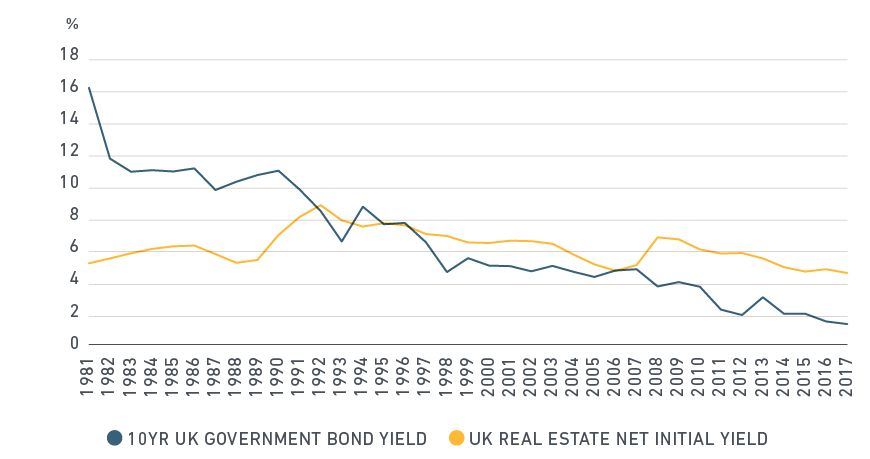

Higher bond yields don't automatically mean higher real estate yields

The stable income stream of real estate can give the impression of a fixed-income investment, but the exhibit below shows that real estate yields movements in the U.K. have actually been relatively independent of bond yields over the past 36 years.5 Further, the real estate yield premium has not been stable — nor has it always been positive.

Real estate yields have had little in common with long-term interest rates

Source: MSCI Global Intel, OECD

That said, there can be commonality between real estate and bonds, in that both are impacted by a discount rate effect when interest rates rise. That is, as long-term rates rise, the present value of a given future cash flow diminishes, putting negative pressure on both asset classes. However, unlike bonds, the future cash flows of real estate are not fixed. When rising rates coincide with rising growth expectations, the growth can dominate the discount rate,6 resulting in low correlations of real estate to interest-rate factors, and pro-cyclical real estate behavior. When considering the potential impact of rising interest rates, it's imperative for investors to remember two things: Real estate does not respond exactly the same as fixed income. And, it may not be enough to factor in what's happening. They might want to figure out why.

The author thanks Thomas Verbraken and Oleg Ruban for their contributions to this post. 2 The contrast in predicted performance for real estate in these two scenarios illustrates the importance of completeness as an attribute of stress test scenarios. For a full discussion of completeness see Acerbo, C. and T. Verbraken. (2016). "Modelling Future Shocks: MSCI Best Practices for Predictive Stress Tests." MSCI Research Insight. 3 Teuben, B. and I. Cullen. (2017). "Listed and Private Real Estate - Putting the Pieces Back Together." MSCI Research Insight. 4 Private real estate is modelled on an unleveraged basis within these scenarios. 5 A similar result can be seen in other countries but we use the U.K. here to show a comparison over the longest possible time period. 6 Shepard, P. et al. (2015). "Is Real Estate Bond-Like?" MSCI Research Insight.

Further reading:

Subscribe todayto have insights delivered to your inbox.

1 Additional background and context on the modelling of interest rate rises can be found in Suryanarayanan, R. et al. (2015). “The Fed Rate Hike: Implications for U.S. and Global Multi-Asset Class Portfolios.” MSCI Research Insight.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.