Getting the Full Picture on Tenant-Default Risk in Real Estate

- Tenant-default risk analysis in real estate portfolios is often focused on the largest tenants by rental income due to resource or data constraints, but the underlying data suggests this practice may be inadequate.

- For most funds in the MSCI Pan-European Quarterly Property Fund Index, rental income is concentrated outside of the largest 10 tenants. As a fund's tenant count increases, the proportion of rent in the top 10 drops.

- Assigning INCANS Global Scores shows that for most of the funds in the analysis, a substantial portion of income comes from tenants with scores below the bond-equivalent rating of below investment grade.

Top-10 analysis is only part of the picture

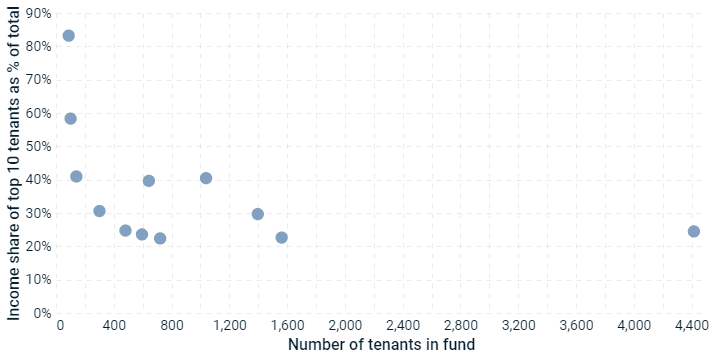

Fund size is an important factor in understanding exposure to tenant-default risk. The exhibit below shows the relationship between the number of tenants and the percentage of total income constituted by the largest 10 tenants. Larger funds tend to have a greater number of assets and more tenants. With a greater number of tenants, the concentration of total fund income within the top 10 drops as the fund's income stream becomes more diversified.

Income share of top 10 tenants as share of fund total

Source: MSCI Pan-European Property Fund Index

A fuller picture tells a different story

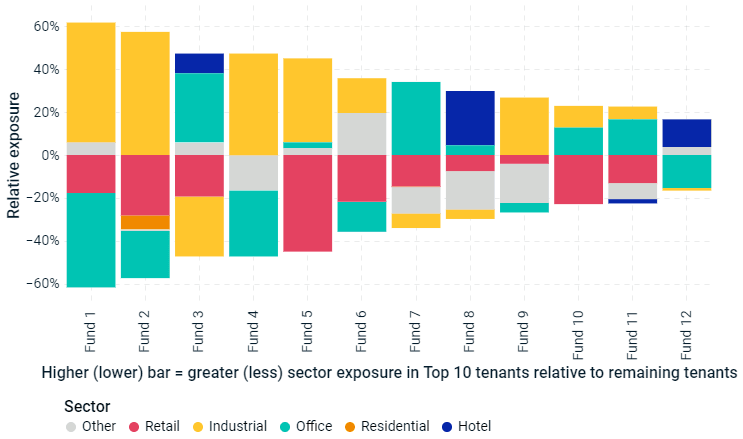

Not only does a focus on the tenant risk of the top 10 risk missing a large proportion of income from the analysis, but the spread of income across property types can be substantially different between the top segment and remainder of tenants. This could be particularly relevant in today's market conditions where occupier strength, as well as the likelihood and potential speed of reletting, may be expected to vary across property types. The exhibit below illustrates the extent to which property-type income exposure among the top 10 tenants is similar or different from that of the remaining tenants. The blocks of color above the x-axis show property types to which a fund has more exposure within the top 10 tenants than among the remainder. The blocks of color below the x-axis show the opposite. Most funds have a greater share of rental income within the 10 top tenants coming from industrial properties and significantly less from retail properties.

Relative sector exposure of top 10 tenants vs. remaining tenants

Source: MSCI Pan-European Property Fund Index

Examining income by tenant-risk profiles

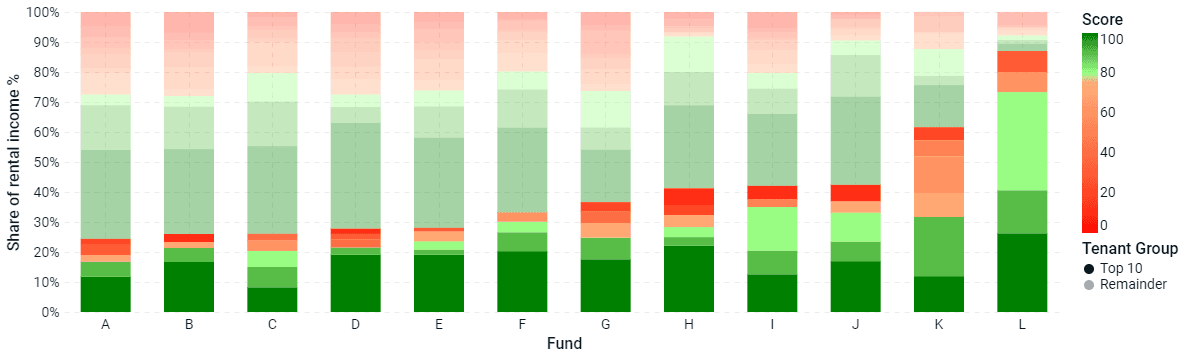

A similar phenomenon is observed when looking at the concentration of income risk across funds. The exhibit below shows rental income for each fund split again across the largest 10 tenants, compared with the remaining tenants. In this chart, income from tenants is broken into 10 risk buckets based on the income's INCANS Global Score, a tenant-risk scoring system. The risk color scale shows tenants with lower (worse) scores as redder and higher (better) scores as greener, and turning at an INCANS Global Score of 76. (This score is the threshold below which the bond-equivalent rating is below BB+, which is considered non-investment grade in fixed-income markets.1)

This breakdown shows that the distribution of income risk across rental income from top 10 tenants is very different from that of the remaining tenants. In only three of the funds (H, K and L) is there a greater share of sub-investment-grade income concentrated in the top 10 tenants than in the remaining tenants (the bold red area is larger than the transparent red area); and for two of those, the majority of total income comes from the top 10 tenants anyway. For the remainder, the majority of sub-investment-grade income risk stems from tenants that comprise the remainder of income. If an investor had examined only the top 10 tenants and assumed the risk characteristics of the remaining tenants' income were similar, income risks may have been underestimated.

Rental income share of the top 10 tenants vs. the remaining tenants, by risk score

Source: MSCI Pan-European Property Fund Index, Income Analytics

Greater importance during economic stress

Collecting tenant-level data and consistently measuring tenant-default risk — especially across countries — are difficult, laborious tasks. It's understandable that managers and investors tend to focus on a more manageable segment of tenants — that is, those contributing the largest rental income. Doing so could lead to partial and biased analysis, potentially missing significant risk exposures in the portfolio. As macroeconomic conditions worsen and tenants come under more stress, making sure one has a full picture of tenant-default risk may become increasingly important for investors and managers of real estate portfolios.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The investment risk for real estate with the equivalent bond ratings as fixed income can be considered lower than that for bonds. Here we are only measuring the risk of default of current lease income. In the case of default, the property still has value. Also, the unit may be released to another tenant.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.