Global Gateway Cities: The Performance Behind the Hype

Blog post

February 21, 2018

Since the Global Financial Crisis, real estate investors have turned to Global Gateway Cities as a key way to diversify portfolios and to generate capital growth. The conventional wisdom asserts these large, well connected and economically dynamic cities should provide more liquidity and more stable cash flows than those available from secondary markets. But have these cities, which include London, New York and Tokyo, offered the superior and safer investments to justify their premium pricing?

In this blog, we show the office sector in Global Gateway Cities did not provide better unadjusted total returns over the decade ending 2016. Dissecting returns between capital growth and income, we found Global Gateway Cities in general provided higher capital growth, but lower income returns than other major cities.

However, we saw a different picture when we adjusted returns for country effects. Relative to country market averages, Global Gateway Cities were concentrated in the top half of performers, although they also displayed higher volatility than their national averages. In contrast, smaller cities generally provided more stable returns with lower capital growth.

Performance Characteristics

We compared the performance of offices in Global Gateway Cities versus groupings of other international cities: Regional Gateway Cities, Nationally Significant Cities and "Other" Cities, from 2007 to 2016, providing a large sample of cities over a major part of the latest real estate cycle.

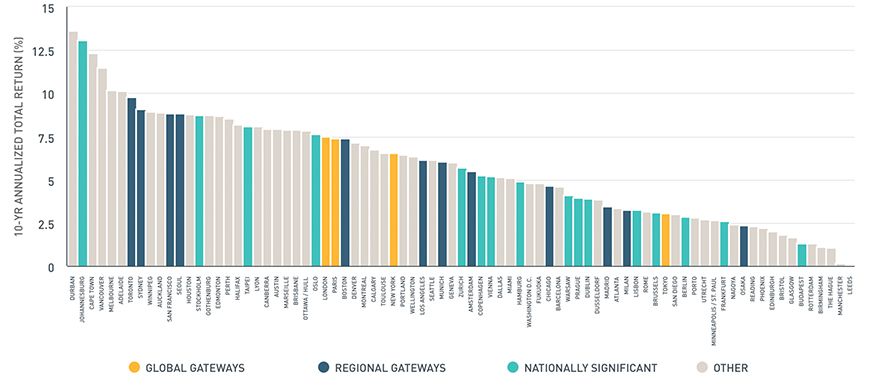

No clear pattern emerged. Cities from each segment were spread across the distribution, as shown below. Global Gateway Cities clearly were not stand-out performers in terms of total return during our sample period, contradicting initial expectations.

Global Gateway Cities were not stand-out performers

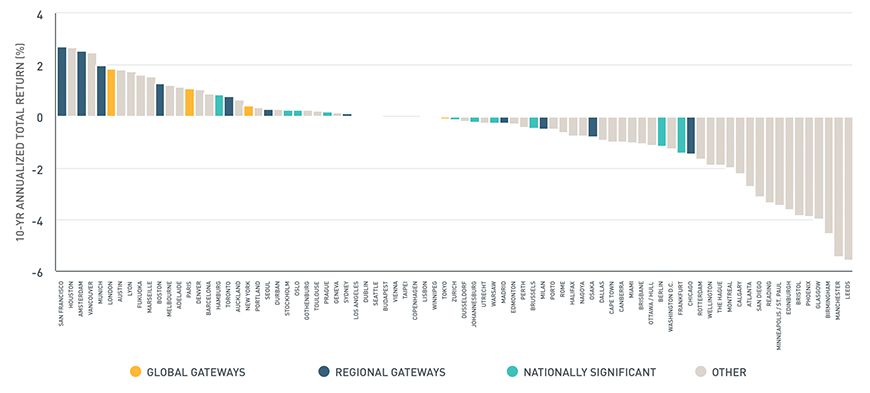

However, adjusting annualized total returns for country effects, Global Gateway City markets tended to outperform, clustering in the top half of the distribution in the exhibit below (left side).

Gateways stand out more on a relative basis

Risk characteristics

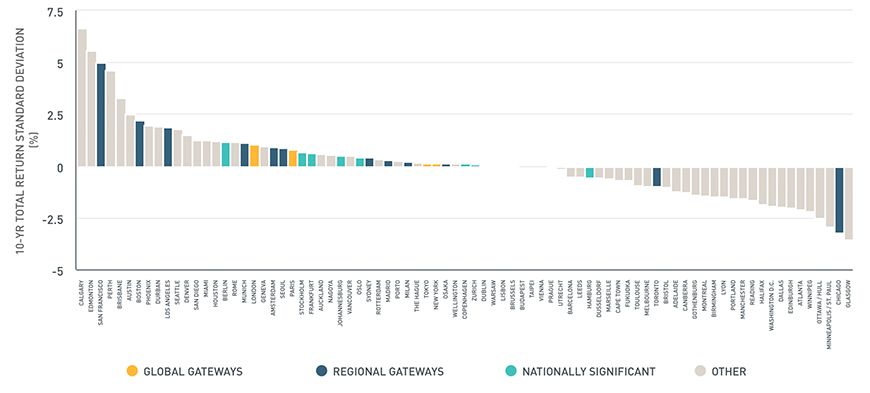

The exhibit below shows Global Gateway City markets recorded higher volatility (standard deviation) of yearly total return than their national market average, ranking them in the top half of the distribution.

Global Gateway Cities tended to be more volatile than their domestic peers

The higher volatility seen in Gateway Cities was not surprising, as they provided lower income returns and were more heavily dependent on capital growth than other markets. Capital growth tends to be the more volatile component of total returns.

According to MSCI data, Global Gateway Cities did not consistently represent "superior" or "safer" investment locations over the analysis period, but they did tend to outperform their national markets, albeit with greater volatility. While city level trends are important to consider, it is clear that national level dynamics were also significant drivers of performance variations.

In general, the ability to define custom market segmentations and apply these in a flexible way to a consistent global database can allow investors to refine and detect key strategic insights. This analysis requires a more granular and more flexible approach, such as that offered by Global Intel PLUS, to segment areas so that nuances in market trends can be revealed. This way, we can offer new insights into the performance characteristics of larger metro areas.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.