Hedge Fund Returns: Is Fund Selection Important?

Blog post

October 22, 2018

Many investors view hedge fund investing as a way to generate returns that are uncorrelated with returns from other parts of their portfolio. We found that the average hedge fund had significant exposure to traditional and factor investing strategies. Moreover, exposure to traditional and factor investing strategies typically accounted for the majority of a typical hedge fund's returns. Further analysis also suggested that some hedge fund-specific strategies generated incremental returns. Given this, investors may wish to pay particular attention to fund selection when making an investment.

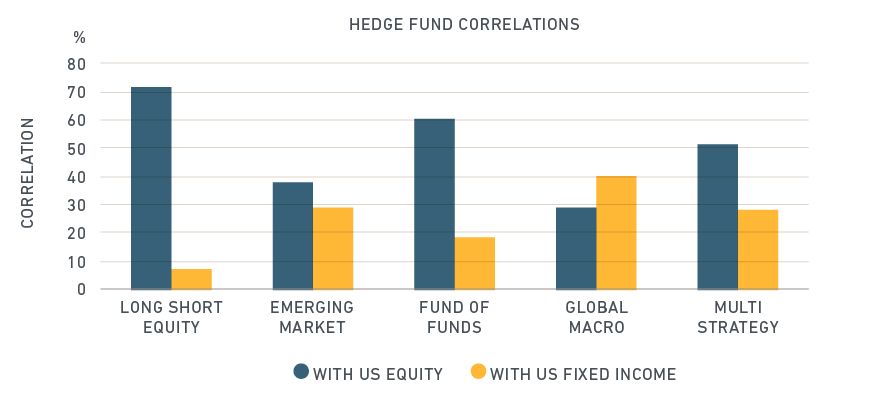

Correlations with equities and bonds

To assess the correlation of hedge funds to other asset classes, we examined the relationship of major hedge fund investment strategies with traditional investments using the MSCI Fund Model.1 Forecasts derived from the model highlighted significant correlations with U.S. equities, ranging from 30% in global macro to 72% in long-short equity. The correlations of the hedge fund strategies with U.S. fixed income were generally lower, ranging from 5% in long-short equity to 40% in global macro. Based on our analysis, hedge funds offered some diversification benefits but the extent of such diversification varied significantly, depending on asset class and strategy.

HEDGE FUNDS HAD SIGNIFICANT CORRELATIONS WITH U.S. EQUITIES AND FIXED INCOME

Each hedge fund strategy is represented by a strategy portfolio, which consists of funds with the same investment strategy from the TASS hedge fund database, weighted by market cap. The U.S. equity strategy is represented by the MSCI USA Index and U.S. fixed income is represented by the ICE BofAML US Corporate and Government Master Index (B0A0) provided by ICE BofAML Global Research, used with permission. The model forecasts are as of December 2017.

Traditional strategies were an important driver of hedge fund performance

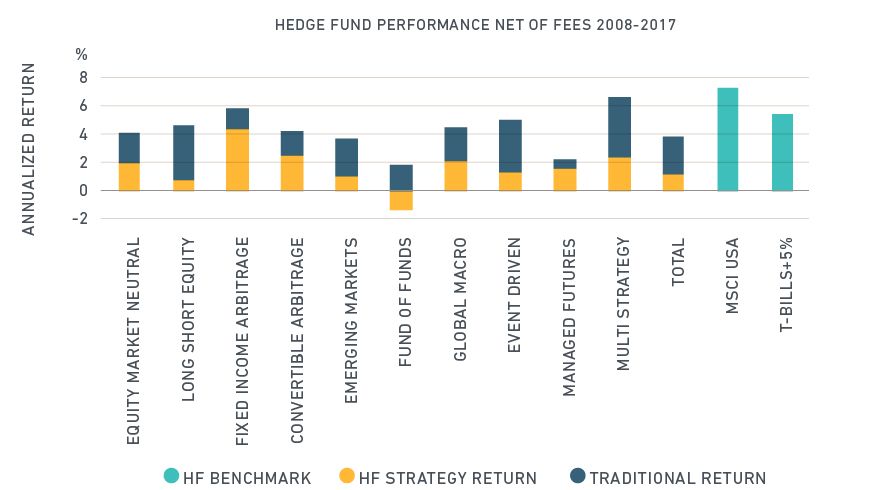

Overall, hedge funds returned an average annual total return of 3.8% after fees from 2008 to 2017, based on TASS data. During the same period, the MSCI USA IMI returned 7.30% and a benchmark of Treasury bills plus 5%2 returned 5.43%. Similar to our correlation findings, our analysis highlighted that hedge fund performance varied significantly by strategy.

Digging deeper, we tried to identify the drivers of hedge fund returns. Using the MSCI Fund Model, we decomposed hedge fund returns into alpha (security selection), traditional beta and factor investing (proxies for index fund returns), and hedge fund strategy beta. We found that hedge fund strategy beta, which may primarily be driven by market timing, offered a source of return and diversification.

The sources of fund returns largely determined the correlations of hedge funds with other asset classes: The greater the returns that were generated from traditional and factor investments, the higher the correlations with equities and bonds. As our analysis found, traditional and factor investing were the main driver of hedge fund performance, with an average annual return of 2.7%3 (versus 1.1% for hedge fund strategy beta).

HEDGE FUNDS HAVE SIGNIFICANT EXPOSURE TO TRADITIONAL DRIVERS OF RETURN

Each hedge fund strategy is represented by a strategy portfolio, which consists of funds with the same investment strategy from the TASS hedge fund database, weighted by market cap. Using the MSCI Fund Model, we decomposed the total portfolio returns to the traditional return (available through index investments) and the hedge fund strategy return. Data as of December 2017.

Buyer beware

Our analysis showed that hedge funds, during the study period, had significant exposure to traditional and factor investing strategies which accounted for the majority of overall hedge fund returns. Investors may have been able to increase diversification benefits from fund selection as we did find disparities among strategies and among funds. However, our analysis indicates careful scrutiny of fund selection may be required.

1 See the footnote to the above exhibit for details on the universe used. MSCI Fund Model is a returns-based model, which extends the traditional style analysis to incorporate other holdings-based information. For example, see Shepard, P., Y. Liu, and L. Yang. (2018). "The MSCI Fund Model." MSCI Research Notes. (Client access only)

Further reading:

Anatomy of hedge fund portfolios

Which factors are more time-sensitive?

The MSCI Fund Model (Client access only)

Subscribe todayto have insights delivered to your inbox.

2 Some investors require a 5% risk premium from hedge fund investments.3 Alpha at the portfolio level is negligible as it gets cancelled out when averaged across funds.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.