How Could China’s Reopening Impact Global Stocks?

- Chinese stocks sold off sharply last year but have since rebounded off their October 2022 lows. Performance has been driven in large part by China's COVID-19 lockdowns and subsequent reopening.

- Global stocks with significant revenue exposure to China, on average, underperformed the global equity market during last year's sell-off in Chinese stocks, but outperformed during the country's reopening.

- We build a simple scenario-analysis framework, allowing investors to weigh broad-market risk versus specific risk driven by China exposure based on perceived economic scenarios.

Chinese lockdowns also affected non-Chinese firms

Since the Russian invasion of Ukraine at the end of February 2022, Chinese equities sold off for a variety of reasons — pandemic lockdowns and geopolitical tensions among them. Between November 2022 and January 2023, however, Chinese equities rebounded on the prospects of a stronger post-lockdown economy. The question is how these themes affected global ex-China stocks with significant revenue exposure to China.

The exhibit below shows that global stocks with higher economic exposure to China1 tended to underperform the risk-adjusted market return2 between March 2022 and October 2022, when Chinese equities underperformed (left panel). Subsequently, from November 2022 to January 2023, during the rebound of Chinese stocks, high-economic-exposure stocks tended to outperform the market on a risk-adjusted basis (right panel).3

The impact of China's lockdowns and reopening on global stocks

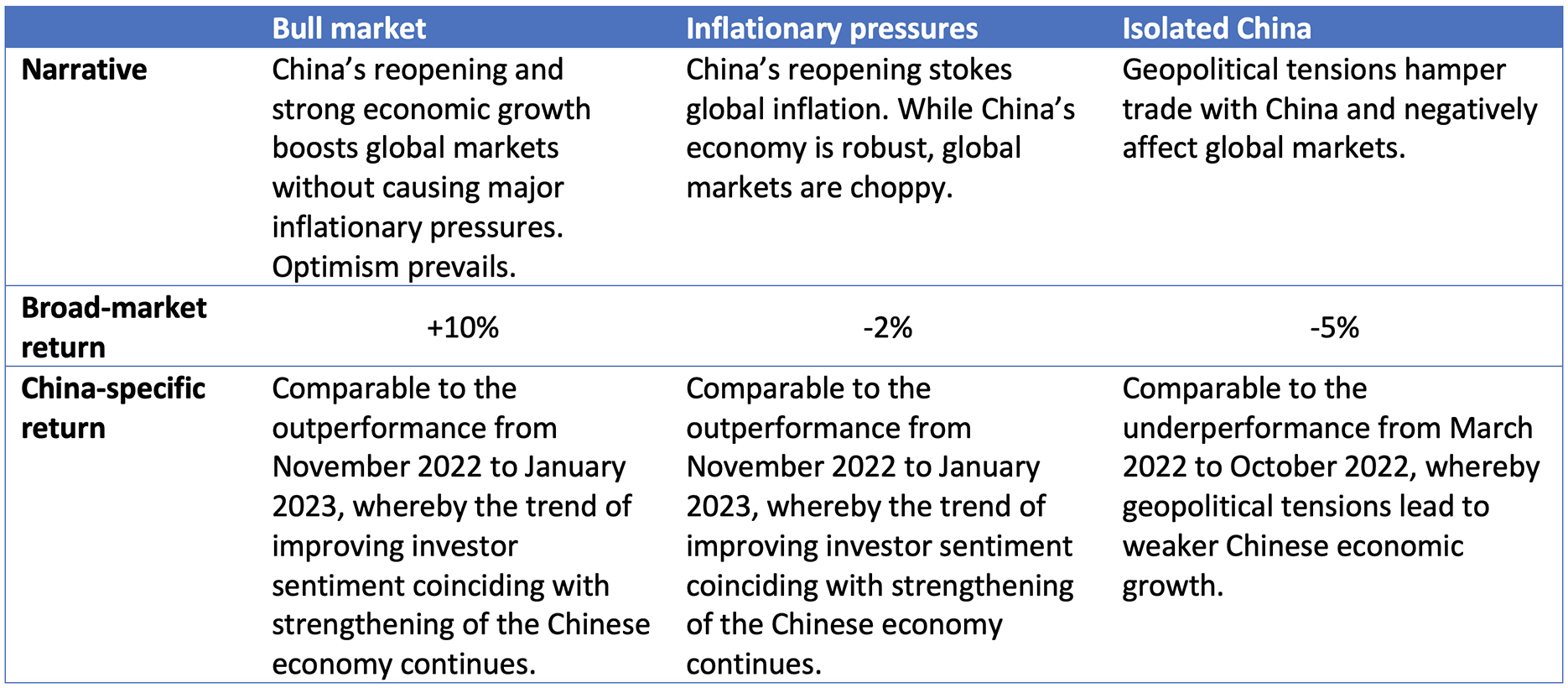

Scenarios for global markets and China

Although the exhibit above shows the average trend and there is significant dispersion around this average across stocks, this relationship suggests that the economic exposure to China could have been a driver of returns beyond broad-market risk. We have set up a simple scenario-analysis framework, whereby a stock's return is driven by two components: systematic broad-market impact and stock-specific impact of China's closing/reopening.

This framework assumes there is no additional impact on a stock's return beyond the broad market and exposure to China. Hence, it does not aim to predict stock returns accurately, but could serve as a data point for investors to weigh the trade-off between broad-market risk and exposure to a specific theme under various scenarios. For an illustration, we assess three hypothetical scenarios for the broad global market and China.

What we assume in our scenarios

These hypothetical scenarios are meant to capture the combination (and potential trade-off) of broad-market impact and China-specific return over a horizon of three to six months. It is assumed there are no other drivers affecting a stock's return; hence the returns under the scenarios are not meant to be accurate predictions of stocks' return.

The exhibit below shows the results under our scenarios across three hypothetical portfolios, represented by MSCI indexes. For broadly diversified indexes such as the MSCI World and MSCI EM ex China Indexes, the impact from the China theme is smaller, while the MSCI World with China Exposure Index shows a significantly larger China-specific return.

Portfolio impact under our scenarios

This framework could be used to assess a universe of stocks in terms of systematic and China-specific impact under certain scenarios. For example, the exhibit below shows the systematic vs. China-specific impact of the "bull market" scenario for two universes of stocks: the MSCI World and MSCI World with China Exposure Indexes. The horizontal axis allows us to assess where each stock is positioned in terms of systematic market risk (above or below average), whereas the vertical axis shows the potential impact of China's reopening under the scenario assumptions.

Systematic versus China-specific impact

The economic exposure to China had, on average, an impact on stock returns during the closing and reopening of the Chinese economy and could be an additional data point for portfolio construction. With different forces affecting equity markets — ranging from potential U.S.-China tensions to economic optimism related to China's reopening — investors could draw on this information to assess potential outcomes and trade-offs.

The author thanks Dora Pribeli for her contributions to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The economic exposure to China expresses how much of a company’s revenue originates from China and is measured as a percentage between 0% and 100%.2A stock’s excess return is measured as the stock’s return minus the risk-adjusted market return, the latter being the stock’s beta multiplied by the market return. In our analysis, the MSCI ACWI Investable Market Index ex China was the universe. A stock’s beta to this universe was estimated by the MSCI Global Equity Model.3In the exhibit, we used a bin width of 20% in incremental steps of 10%, to smooth the chart. The shaded area indicates the standard error for each bin’s estimated average excess return. As there are fewer global ex-China stocks with high economic exposure, the confidence interval widens toward the right-hand side of the chart.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.