How Low Interest Rates May Impact your Portfolio

Blog post

October 6, 2016

Slow growth and a shortage of safe assets have led major central banks to maintain monetary policies that include short-term interest rates near or below zero. The policies, which aim to encourage businesses and consumers to borrow and spend, have lowered bond yields, distorted yield curves, shifted the composition of central banks' balance sheets toward riskier assets and sent savers in search of yield. The persistence of low growth and a lack of inflation also have led investors to wonder whether such policies still pack any punch.

MSCI has modeled three scenarios for near-zero rates that investors can use to stress test their multi-asset class portfolios. Note that each scenario below aims to assess the impact of various shocks. Investors can use analytics from MSCI to evaluate potential impacts of these and other scenarios tailored to their portfolios.*

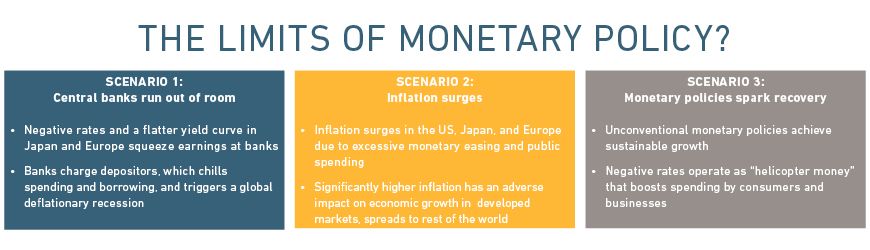

Scenario 1: Central banks run out of room

Negative rates squeeze earnings at banks in Europe and Japan, which in turn charge depositors to keep money in their accounts. That adds to investor uncertainty, which chills spending and borrowing and tips the eurozone and Japan into a deflationary recession that spreads to the rest of the world. The pressure on banks leads to a rise in systemic risk. Credit spreads for financials widen by about 40% relative to current levels, and the VIX jumps by 45%.

Implications:

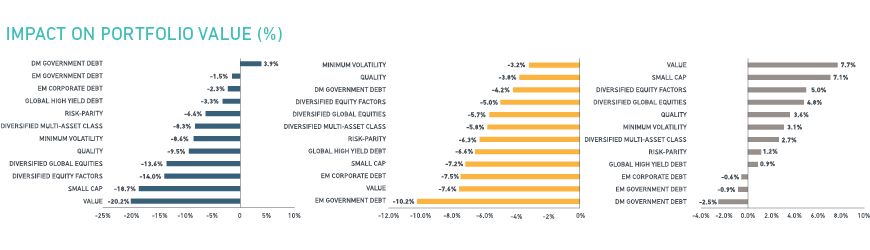

Equity markets are rattled worldwide, falling 13.6%. Equity factors that tend to be cyclical, including value and small cap, could lose 20.2% and 18.7%, respectively, while defensive factors such as minimum volatility and quality likely would outperform.

Yield curves flatten globally, sending yields below zero across maturities in Europe and Japan. Fixed income portfolios with longer durations and a tilt toward Treasurys would likely benefit as well.

A diversified multi-asset class portfolio could lose as much as 8.3% of its value. A risk parity portfolio with enhanced exposure to bonds might mitigate the impact, losing 6.4%.

Scenario 2: Inflation surges

A prolonged period of monetary easing and a buildup of government debt in the U.S., Europe and Japan fuels inflation expectations. Significantly higher inflation has an adverse impact on growth that spreads to the rest of the world.

Implications:

Equities could lose as much as 5.7% globally while emerging market stocks could shed 3.5%. Value and small-cap equity factors could underperform the market, along with defensive factors such as minimum volatility or quality. Yield curves steepen significantly across developed markets. Fixed income portfolios with lower duration could fare better relative to market. With losses spread across all asset classes, a diversified portfolio could lose 5.8% of its value. A risk-parity portfolio stands to lose as much as 6.3%.

Scenario 3: Monetary and fiscal policies spark economic recovery

Unconventional monetary policy achieves sustainable growth. Low rates operate as helicopter money that boosts spending by consumers and businesses. The buildup of risky assets on the balance sheets of central banks together with government-backed investments in infrastructure and alternative energy create incentives for risk-taking by investors. The return of growth combined with benign inflation allows central banks to normalize their policies.

Implications:

Equities around the world could gain about 4.8%. Cyclical factors such as value and small-cap could outperform defensive factors and the overall equity market. Yield curves steepen globally. Fixed income portfolios with lower duration and enhanced exposure to credit also stand to benefit. A diversified multi-asset class portfolio could gain 2.7% while a risk-parity portfolio may gain 1.2%.

*Analytics from MSCI include RiskManager, BarraOne, and MSCI's Macroeconomic Risk Model and Scenario Analysis Service. Clients will find guidance on how to implement the stress tests in RiskManager and BarraOne at our client support site.

The author thanks Raghu Suryanarayanan and Thomas Verbraken for their contribution to this post

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.