Index Rebalancing During High Volatility: A Balancing Act

Blog post

May 13, 2020

- During the COVID-19 crisis, equity markets in most countries and regions saw significant declines. Even though markets have partially recovered from those lows, volatility remains higher than the historical average.

- Against this backdrop, rebalancing of indexes is top-of-mind for many investors, as they seek a balance between two competing objectives: market representation and index turnover.

- The MSCI Global Investable Market Index (GIMI) methodology aims to strike that balance between a timely representation of the investment opportunity set and turnover while also maintaining investability1 and replicability.

Seeking Balance

The MSCI GIMI methodology aims to find a balance within necessary trade-offs across our market-capitalization-weighted equity indexes to meet multiple objectives. Apart from aiming to provide indexes that are precise, investable and replicable, it strives to meet two other key aims:

- Timely reconstitution of securities to reflect the evolution of equity markets

- Limit index turnover to better support index stability and trading cost efficiency

May 2020 GIMI Index Review

In accordance with the methodology, the MSCI GIMI Indexes will be rebalanced on the last business day of May 2020, with changes effective June 1, 2020. The proforma results of the rebalancing were announced on May 12, 2020. As with previous May semi-annual index reviews (SAIRs), the May 2020 review involved reassessing companies against liquidity criteria, assigning companies to large-, mid- and small-cap size segments and applying buffer zones to reduce index turnover. Though this SAIR was scheduled, with large shifts in equity markets, the need to refresh the index in this way becomes more pressing.

Assessing the Investable Universe

The May 2020 index review will result in the timely removal of securities that do not meet the minimum liquidity threshold and help ensure the rebalanced index meets minimum liquidity requirements. Additionally, rebalancing will allow the addition of newly eligible securities, including IPOs since the November SAIR.

Assigning Companies to Large-, Mid- and Small-Cap Size Segments

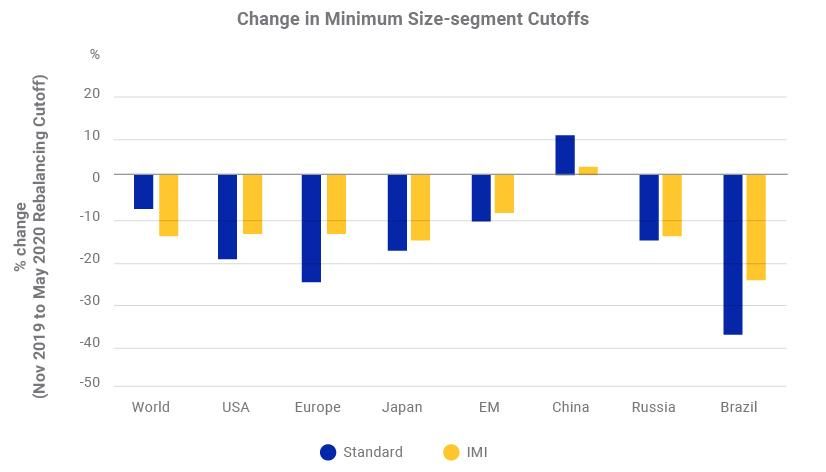

The MSCI GIMI methodology assigns companies to large-, mid- and small-cap segments by determining minimum size-segment cutoffs that target market-cap coverage of 70% for large-caps indexes, 85% for standard indexes (large- and mid-cap) and 99% for IMI (large-, mid- and small-cap) in each market. Typically, when based on stock price performance alone, companies can migrate from one size segment to another, leading to index turnover. However, when equity markets move, the minimum size-segment cutoffs in the MSCI GIMI are designed to adjust as they continue to target the same market cap coverage. This provides a natural buffer for the retention of companies within the same size-segment, which can reduce turnover.

In the exhibit below we show the performance of select key developed- and emerging-market countries as well as the change in the minimum size-segment cutoffs across these countries. The size-segment cutoffs adjusted with the performance of the underlying markets. Interestingly, for Chinese equity markets, which fully recovered over the period of analysis, the minimum size-segment cutoff adjusted upward, and in Brazil, where markets were severely impacted, the downward adjustment of the minimum size segment was significantly higher than other markets.

Equity Market Performance and Changes in Minimum Size-Segment Cutoffs

Data as of the close of trading Oct. 18, 2019, and April 21, 2020, for the November 2019 SAIR and May 2020 SAIR, respectively. Standard refers to large- and mid-caps and IMI refers to large-, mid- and small-caps.

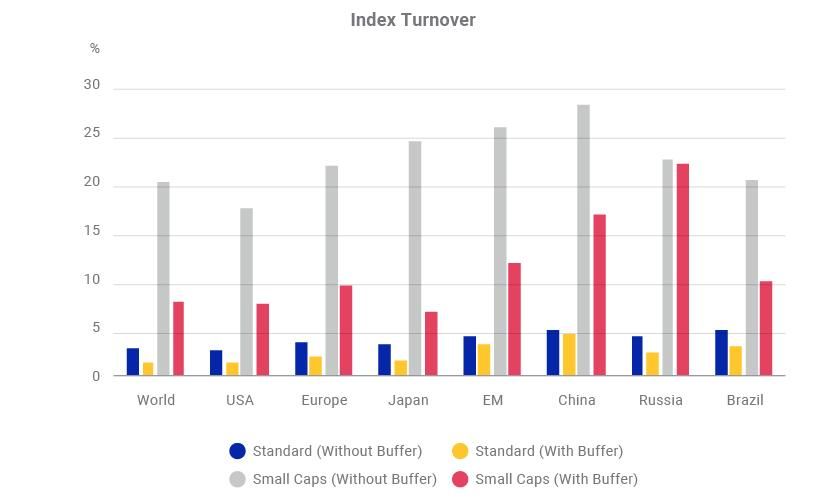

Applying Buffers to Limit Turnover

In an effort to control index turnover, the MSCI GIMI methodology explicitly applies multiple buffers that restrict inclusion, exclusion and migration of securities between size segments. For instance, a security may remain in its current size segment provided its full market capitalization falls within a buffer zone set below the minimum cutoff. To illustrate, the exhibit below reviews the impact this buffer had on turnover for the same select developed- and emerging-market countries.

Impact of Size-Segment Buffer

Index turnover calculated for the May 2020 SAIR with and without application of size-segment buffer. Standard refers to large- and mid-caps.

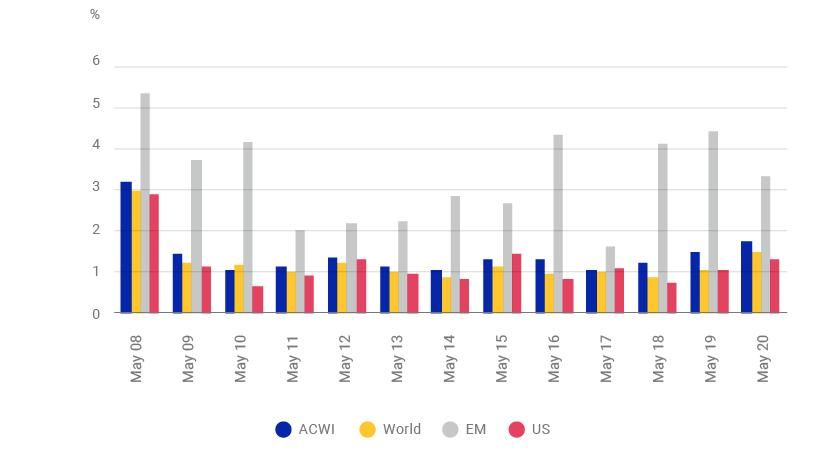

To put May 2020 index turnover in context, the exhibit below shows it was in line with past May SAIRs. The 12-year period includes more benign market environments as well as volatile times such as the 2008 global financial crisis. Relative market volatility had no significant impact on index-rebalancing turnover.

May 2020 Turnover was in Line with Historical Averages

Index turnover reported for May SAIR for standard (large- and mid-cap) size segment.

Alignment Between Parent and Derived Indexes

The market-capitalization-weighted MSCI Global Investable Markets Indexes are also the underlying security universe for derived indexes such as factor or ESG indexes. Rebalancing these indexes allows changes to trickle down to derived indexes and aims to help avoid tracking error arising from benchmark misalignment.

While significant shifts in equity markets may highlight a need for index reconstitution, they may also raise concerns around excess turnover and the likely associated trading cost. MSCI Global Investable Markets Indexes aim to provide sustained and appropriate market representation without significantly higher index turnover. Our analysis showed that, with the help of implicit and explicitly applied buffers, the May 2020 index turnover was similar to that seen in past SAIRs, even in the face of current market volatility.2

Further Reading

Subscribe todayto have insights delivered to your inbox.

1You cannot invest in an index. Investability refers to the ability of an institutional investor to make the investments needed to replicate the index.2Illustrative purposes only. Past performance is not indicative of future results or how a product replicating the indexes may perform.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.