Is Momentum Crashing?

Blog post

April 8, 2016

Momentum, the tendency of past winners to continue to do well in the near future, is a pervasive return regularity in equities and across asset classes. It is used both as a signal in alpha models and as a factor in risk models. But after a sharp drop and subsequent rebound in equity markets in the first three months of the year, the momentum factor reportedly has crashed.

MSCI's models confirm as much but also shed light on some factors that share characteristics with momentum and that have performed well over the same period. The models offer a way for investors to monitor risk exposures that tie to their investment horizons.

Momentum is a complex factor. In the literature, reversal effects have been reported over five year periods, momentum effects over one year, and reversal effects over periods from one month to one day. Momentum has been included in Barra factor models for many decades. One of the innovations in the latest Barra factor models is the rich, granular factor structure that allows deeper insights into complex factors like momentum and enables investors to match their horizon with an appropriate set of factors.

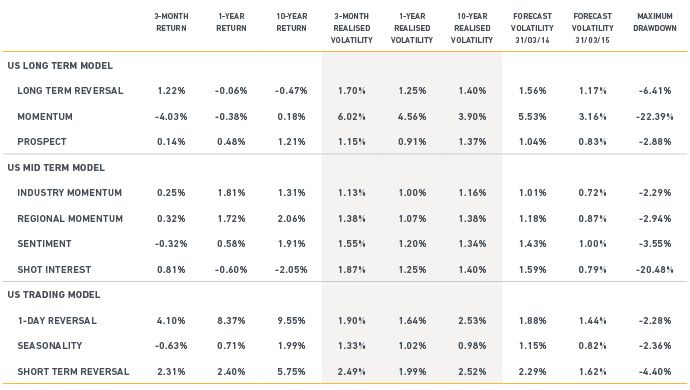

The table below shows momentum factor returns, volatilities and drawdowns based on daily factor returns from the Barra U.S. Total Market Equity Model.1 The model comes in three variants – long-term, medium-term and trading – and covers a different set of momentum factors depending on the investment horizon.

Momentum factor returns over the most recent 10 years

The analysis reveals that the momentum factor suffered a sharp drop of 4% during the first quarter, equivalent to 2.7 standard deviations on an annualized basis. However, this decline is not as steep as the drawdown of 22.4% that momentum experienced during the 2008-2009 financial crisis.

Negative returns for momentum in the first quarter contrasted sharply with positive returns in reversal factors. Long-term reversal – the tendency of stocks that have declined in the past five years to recover in the subsequent period – rallied by 1.22%, equivalent to 2.9 annual standard deviations, while one-month and one-day reversal factors also experienced comparatively large positive returns in the period.

Factor returns analyzed in the table above correspond to the returns of "pure" factor portfolios. These are theoretical long-short market-neutral portfolios that have unit exposure to their underlying factors, zero exposure to all other factors and minimum risk. Though these portfolios are the purest expression of a factor, they would be practically impossible to implement as an investment strategy because they require thousands of long and short positions, daily rebalancing, and high turnover.

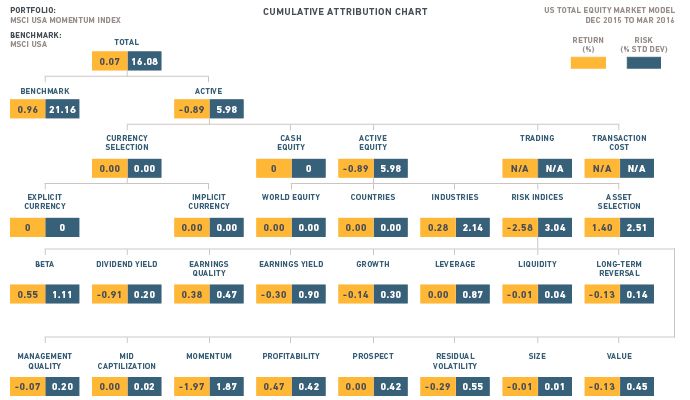

To understand how actual momentum strategies may have been affected by the recent decline in momentum factor returns, we use the Barra U.S. Total Market Equity Model for Long-Term Investors to analyze the performance of the MSCI USA Momentum Index.

The chart below shows that the MSCI USA Momentum Index underperformed the MSCI USA Index by 89 basis points (bps) in the first three months of 2016. Negative contribution of 197 bps from momentum was partly offset by positive contributions of 55 bps, 38 bps, and 47 bps from beta, earnings quality and profitability, respectively. The MSCI USA Momentum Index also has exposure to these factors because it uses risk-adjusted returns to select constituents so as to mitigate the vulnerability to volatility of high-momentum stocks.

Decomposing performance of the MSCI USA Momentum Index (First quarter, 2016)

To be sure, momentum strategies that focused on stocks that rallied in the past six to 12 months suffered losses in the first three months of this year. But momentum has many facets.

1 Clients of MSCI can find complete details of the model and precise factor definitions at the Barra model client support site.

Further reading

Riding on Momentum

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.