Is there another Woodford waiting to happen?

Blog post

July 11, 2019

- After the Woodford Equity Income Fund had to gate redemptions, institutional investors may worry that other European UCITS funds could have a similar liquidity mismatch.

- We used MSCI's LiquidityMetrics to see how the liquidity profiles of these funds would look if U.S. regulations, rather than Europe's less prescriptive ones, applied.

- Most funds we analyzed were highly liquid, but those that weren't may risk a mismatch between the funds' liquidity profiles and potential redemption requests.

Liquidity matters despite less regulation for European funds

The liquidity rules of the U.S. Securities and Exchange Commission (SEC) prevent open-end mutual funds from holding more than 15% of their investments in illiquid assets, with the aim of reducing the likelihood of redemption suspensions.1 While the corresponding European regulation does not set limits on holdings, funds complying with the rules must allow redemptions at least twice a month — and many UCITS funds permit withdrawals on any day, known as daily dealing.2

This may create an incentive for a UCITS fund to hold sufficiently liquid investments to ensure alignment with daily dealing — or whatever has been promised in terms of withdrawal rights. As Andrew Bailey, chief executive officer of the U.K. Financial Conduct Authority, put it: "It is not sensible to provide for daily dealing and redemption in open-ended funds that hold a large exposure to illiquid assets, including those that while listed are not regularly traded."3

How do other funds' liquidity profiles compare to Woodford's?

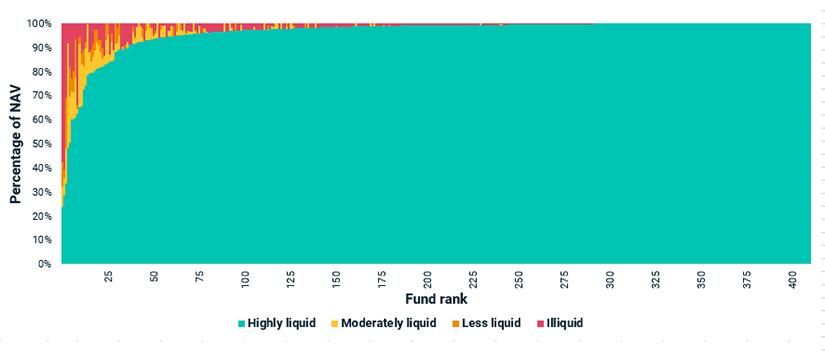

We used MSCI's LiquidityMetrics to assess the liquidity of a sample of European funds with similar characteristics to Woodford's, analyzing UCITS funds with assets under management greater than EUR 1 billion that primarily invest in equities. We applied the SEC bucketing rule to study how each fund's liquidity profile would look if the U.S. regulation applied. In the exhibit below, we ordered about 400 such UCITS funds along their highly liquid bucket proportion under a 5% anticipated trading scenario.4

Most, though not all, UCITS funds were highly liquid

Source: MSCI; Lipper, a Refinitiv company, as of March 31, 2019. Breakdown of equity UCITS funds with AUM greater than EUR 1 billion, according to the SEC's prescribed bucketing rules. We used a 5% anticipated trading size and MSCI's suggested significant market impact thresholds for the analysis.

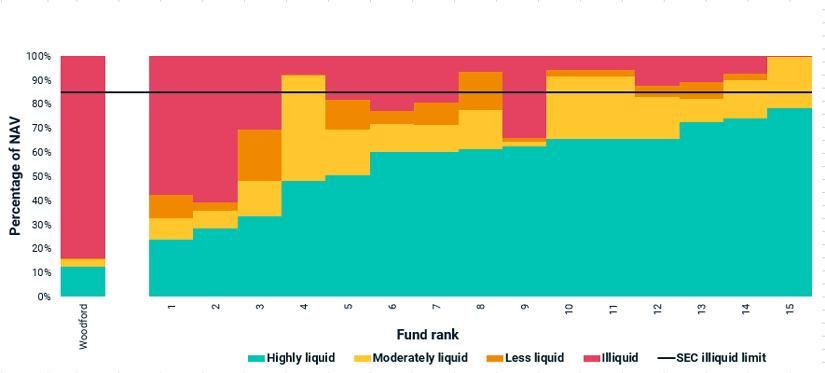

The vast majority of these portfolios were very liquid. However, there were a handful of funds that warranted further examination. In the exhibit below, we compare the liquidity profile of the 15 least liquid UCITS funds, ranked by their highly liquid fraction, to that of the Woodford Equity Income Fund's 85% illiquid holdings, as of Dec. 31, 2018.

Seven of the funds breached the SEC's 15% illiquid-holding limit, and approximately 1% of them had less than half of their holdings in the highly liquid category. In short, the liquidity profile of these funds may be misaligned with anticipated redemption requests.

Least liquid UCITS compared to Woodford Equity Income Fund

Source: MSCI; Lipper, a Refinitiv company. Woodford's fund liquidity shown as of Dec. 31, 2018. The 15 least liquid UCITS funds shown as of March 31, 2019. The 15% limit of illiquid holdings is prescribed by the SEC's regulation for U.S. mutual funds.

The price of misaligned liquidity

Misaligned liquidity can be a risk for both institutional investors and fund managers. For institutional investors, a potential liquidity mismatch may prevent them from withdrawing their capital upon request, while suspension of withdrawals may harm a fund manager's reputation. Even though most of the analyzed UCITS funds seemed sufficiently liquid, there were a handful with relatively large exposure to liquidity risk. The Woodford fund highlighted the importance of keeping an eye on a fund's liquidity profile as a key component of managing risk.

The author thanks Laszlo Arany for his contributions to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The SEC’s liquidity rules assign each portfolio holding into one of four buckets based on how long it takes to sell a portion of the position that the fund reasonably anticipates trading within reasonable transaction costs. A holding is deemed to be highly liquid if it can be traded and settled in three days, moderately liquid if it can be traded and settled in a week and less liquid if it can be traded but cannot be settled in a week. Otherwise, the holding is considered illiquid. “Investment Company Liquidity Disclosure.” Securities and Exchange Commission, June 28, 2018.2“Recommendation of the European Systemic Risk Board of 7 December 2017 on liquidity and leverage risks in investment funds.” , April 30, 2018.3Binham, C. and Riding, S. “FCA head says fund rules may need to change after Woodford meltdown.” , June 9, 20194The anticipated trading scenario is fund-specific. It depends on the fund’s investor composition, redemption history and market conditions. A 5% scenario sits in the middle of the typical range and could capture important liquidity characteristics.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.