Liquidity and correlation in the Chinese credit market

Blog post

July 9, 2019

- The Chinese credit market is now the second-largest in the world, with 38 trillion Chinese yuan (USD 5.5 trillion).

- However, foreign ownership of Chinese credit has remained extremely modest, with overseas bondholders owning less than 1% of the market.

- An anomaly exists in how credit from the same issuer trades in the China onshore and U.S. markets.

"Large" does not mean "liquid"

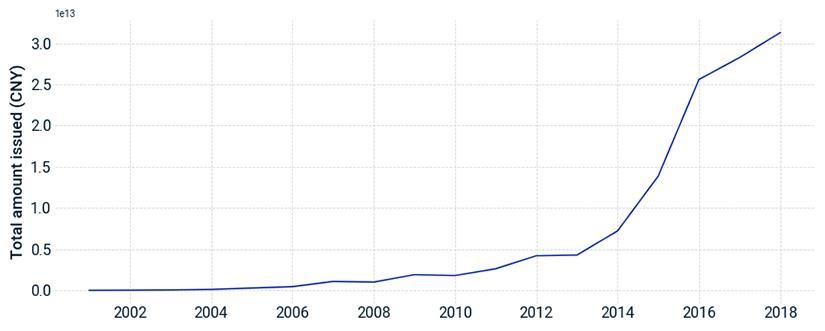

Following the Global Financial Crisis, Beijing launched an economic stimulus program that encouraged many state-owned enterprises to borrow money to finance growth.4 At the same time, China loosened credit requirements as part of an effort to promote direct financing, providing additional stimulus to the market.5 When the People's Bank of China cut rates and reserve requirements in 2015,6 debt growth accelerated further, as can be seen in the exhibit below.

As noted, non-domestic investors hold a tiny proportion of Chinese credit (compared to 30% in the U.S.).2 Moreover, these investors have raised concerns about the relatively poor liquidity of this market, as most bonds are owned by a small group of local institutions and are held until maturity.7

Chinese yuan (CNY) denominated corporate debt issuance

Source: Refinitiv

An idiosyncratic market

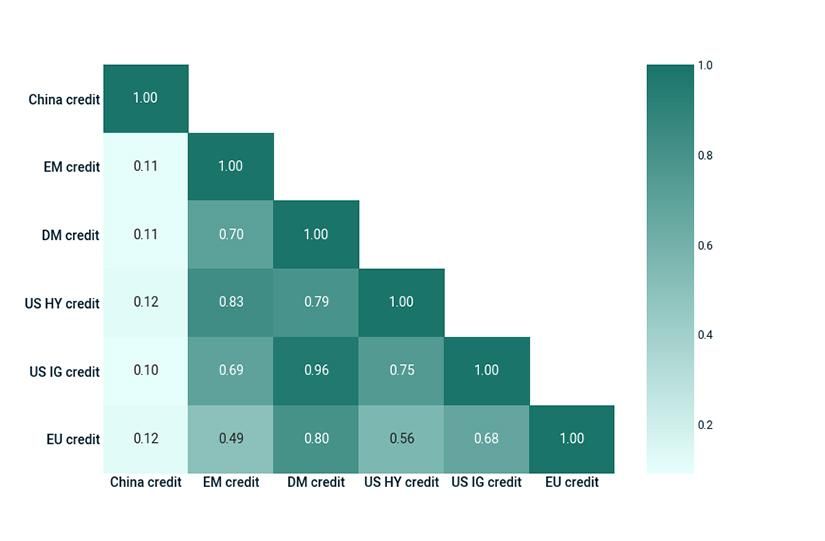

Chinese corporate bonds have shown low correlation with both emerging- and developed-market credit, given the idiosyncratic nature of China's state-driven macroeconomic policies and the low participation of foreign investors in the market. We can see Chinese credit's low correlation with other global credits in the matrix below.

Chinese corporate debt exhibited low correlation with other credit markets

Source: MSCI's MAC factor model correlation matrix as of May 23, 2019. Calculated using a two-year half-life and weekly data. China, the U.S. and EU are tier four level factors, while EM and DM are tier two. Factors are calculated in local currency.

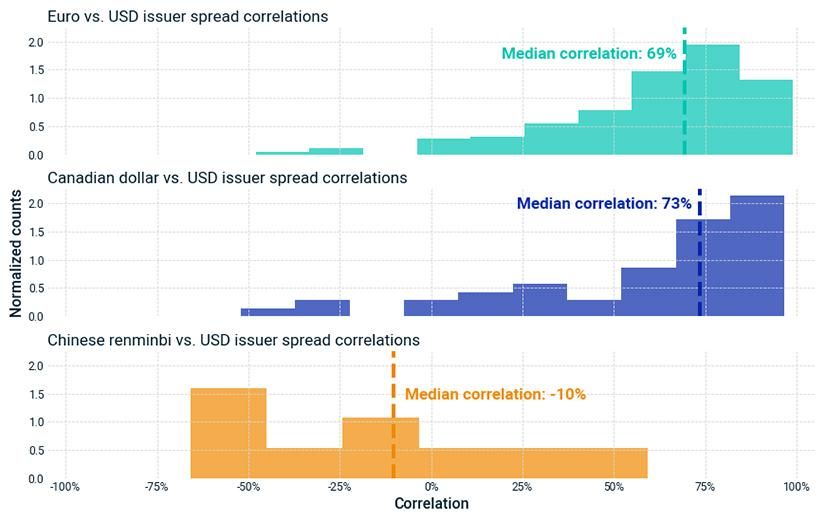

There also is an anomaly in how credit from the same issuer trades in the China onshore and U.S. markets. Theoretically, these bonds should trade with high correlations, as both bonds face equal credit risk. This is true for markets such as Canada, Europe and the U.S., where the average spread correlation of debt of an issuer trading across markets is around 60%-70%. In contrast, bonds of similar maturities from Chinese companies that issue debt denominated in both the Chinese renminbi and the U.S. dollar exhibited much lower correlations – close to zero and sometimes negative – as we can see in the exhibit below.

Bonds from the same issuer trading on CNY and USD exhibited low correlations

Source: MSCI's issuer curves. We looked at the correlation of three-year spreads on bonds from the same issuer trading on distinct currency pairs. Data sampled from Jan. 1, 2016 through April 26, 2019 with weekly frequency for 15 Chinese, 47 Canadian and 175 European Union issuers. We also note that the hypothetical portfolios of renminbi and U.S. bonds for the Chinese issuers exhibited similar average currency-hedged monthly returns.

An evolving bond segment

The characteristics of China credit have been related to China's unique macroeconomic policies and the composition of market participants. As China's regulators continue to make their equity and bond markets more accessible to international investors, these characteristics may continue to evolve.8 Such moves, including the opening of the related futures market,9 may attract participation from more international investors, potentially leading to better liquidity and changes in the market's correlation structure.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Rapoza, K. “Why China’s Stock Market is in Beast Mode.” Forbes, March 19, 2019.2Cook, R. “Ratings key to globalizing China’s bond market.” Asia Times, May 9, 2019. We define credit as policy bank bonds plus corporate credit.3Schipke, A., Rodlauer, M. and Zhang, L., eds. 2019. “The future of China’s bond market.” International Monetary Fund.4“China's stimulus package.” Australia Department of Treasury, March 30, 2012.5Lee, D. "China's stimulus plan sets high bar." LA Times, Nov. 10, 2008.6“China defaults to rise as corporate debt burden climbs: S&P.” Reuters, July 16, 2016.7Weinland, D. “Risk of liquidity shocks haunts China’s fast-growing bond markets.” Financial Times, May 27, 2019. Op. cit., IMF.8Curran, E. and Chen, T. “How China’s $13 trillion bond market may be trade-war winner.” Bloomberg, April 24, 2019.9Weiland, D. “China prepares to open up bond futures market to domestic Banks.” Financial Times, May 22, 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.