Re-Examining the Tax Gap for MSCI World Companies

Blog post

June 3, 2015

Regulatory authorities are now taking a much tougher approach to corporate tax rates. Since we explored the topic in December 2013 (The 'Tax Gap' in the MSCI World), the regulatory outlook has shifted substantially. New country-by-country transfer-pricing reporting requirements from the Organisation for Economic Co-operation and Development (OECD) will come into effect in January 2016. Favorable tax deals will likely be scarcer in the near term, given the European Commission's investigation of whether "sweetheart" tax arrangements offered by Ireland, Luxembourg and Netherlands contravene European competition rules against providing "state aid." Some countries have also proposed specific tax-avoidance legislation explicitly targeting big name multinationals, such as U.K. legislation dubbed a "Google Tax'" and Australia's new "Netflix Tax."

Key findings of that report included:

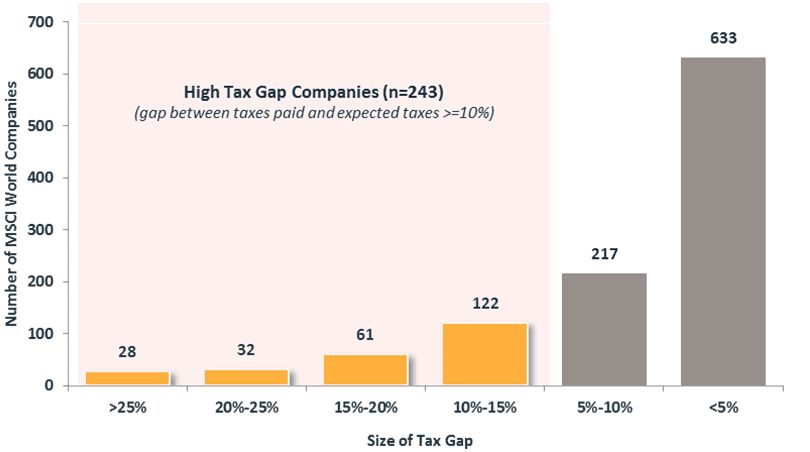

- Taxes paid by the 243 companies in the MSCI World Index with the largest tax gaps (defined as the difference between the reported tax rate paid and the tax rate of where companies generate revenues) would have totaled an estimated USD 82 billion per year in taxes, had these companies been paying taxes at the same rate as their peers in the MSCI World Index. If these taxes had been paid, it could have reduced aggregate profit after taxes across these 243 companies by approximately 20% over this period (Exhibit 1).

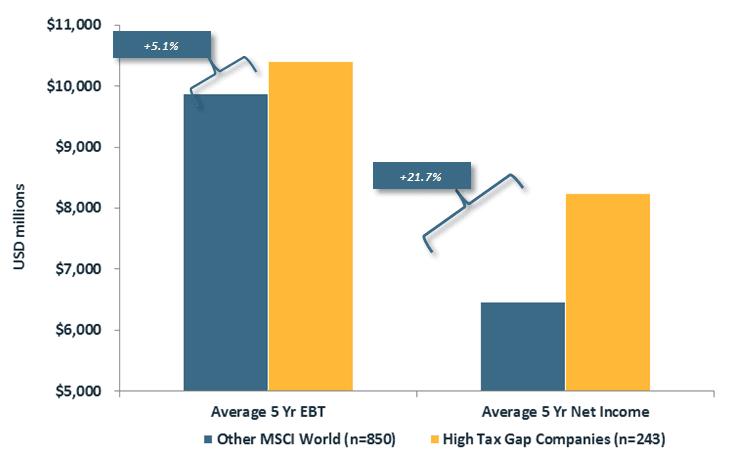

- High "tax gap" companies enjoyed a sizable profit advantage over their peers despite having a far smaller pre-tax earnings advantage, suggesting tax strategy played a role in the difference (Exhibit 2).

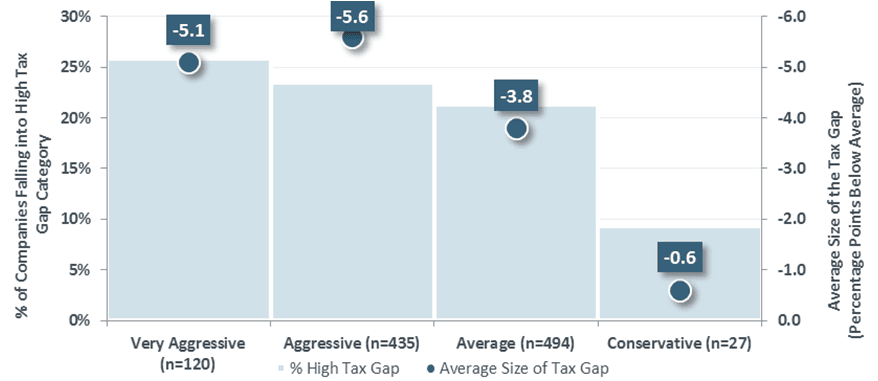

- Using MSCI ESG Research's forensic accounting (AGR) scores, we found that companies with very aggressive accounting ended up paying lower taxes, with a significantly higher proportion of high "tax gap" companies represented in the very aggressive accounting categories than the conservative accounting category (Exhibit 3).

Exhibit 1: Gap Between Tax Rate Paid and Weighted Average Tax Rate of Countries Where Revenues are Generated

MSCI World Index Companies excluding REITs, Mining Companies, and Companies with Negative Profits (n=1,093). Period from 2009-2013.

Exhibit 2: Comparison of Earnings Before Tax and Net Income between High Tax Gap Companies and Rest of MSCI World Index

Excluding REITs, Mining Companies, and Companies with Negative Profits (n=850). Period from 2009-2013.

Exhibit 3: Tax Gap Characteristics

MSCI World Index Companies excluding REITs, Mining Companies, and Companies with Negative Profits (n=1076 companies of 1093 MSCI World companies for which MSCI ESG Research's Accounting and Governance Risk (AGR) data was available. Period from 2009-2013.

The results suggest that employing different tax strategies than their peers could have been a main driver of the large net income advantage enjoyed by these high "tax gap" companies over this period. On the one hand, whatever tax strategies these companies employed clearly worked over this period in that these companies reported much higher net income than they might have otherwise. On the other hand, the higher net income may have resulted from maneuvers unrelated to the quality of the core business operations, where the advantages enjoyed by these companies over their peers seem to be more modest.

While our "tax gap" analysis cannot identify instances of aggressive profit-shifting per se given limited disclosure by companies, it can suggest a more targeted set of companies for investor engagement by understanding the large gap between the reported tax rate paid and the tax rate of where companies generate revenues.

Read the report, "Re-Examining the Tax Gap."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.