Reported Emission Footprints: The Challenge is Real

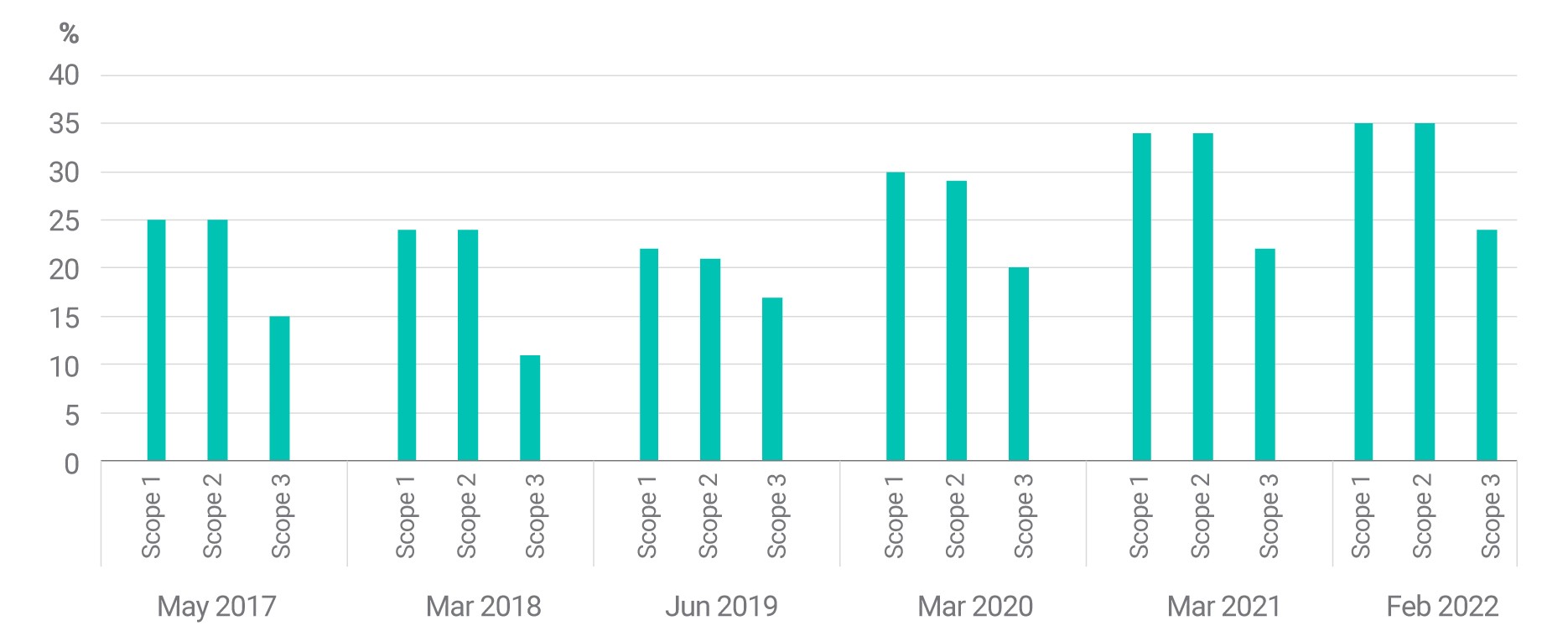

- Greenhouse-gas (GHG) emissions are a key input in climate-related metrics. Fewer than 40% of MSCI ACWI Investable Market Index constituents reported Scope 1 and 2 emissions, however.

- Fewer than 25% of MSCI ACWI IMI constituents reported Scope 3 GHG emissions.

- The sum of reported emission breakdowns did not add up to total reported footprints for 30% of companies.

GHG-disclosure rates for MSCI ACWI IMI constituents

MSCI ACWI IMI constituents' disclosure rates, as of respective dates. Source: MSCI ESG Research LLC

Current state of data quality

The percentage of companies reporting their emission footprints isn't the only problem, however: Data quality has proven to be problematic as well. A recently published report identified inconsistencies in emissions data reported to environmental organization CDP (formerly the Carbon Disclosure Project).2 The sum of reported emissions broken down in categories such as business lines, region and type of greenhouse gas did not add up to the total reported footprint for 30% of companies, according to the analysis.

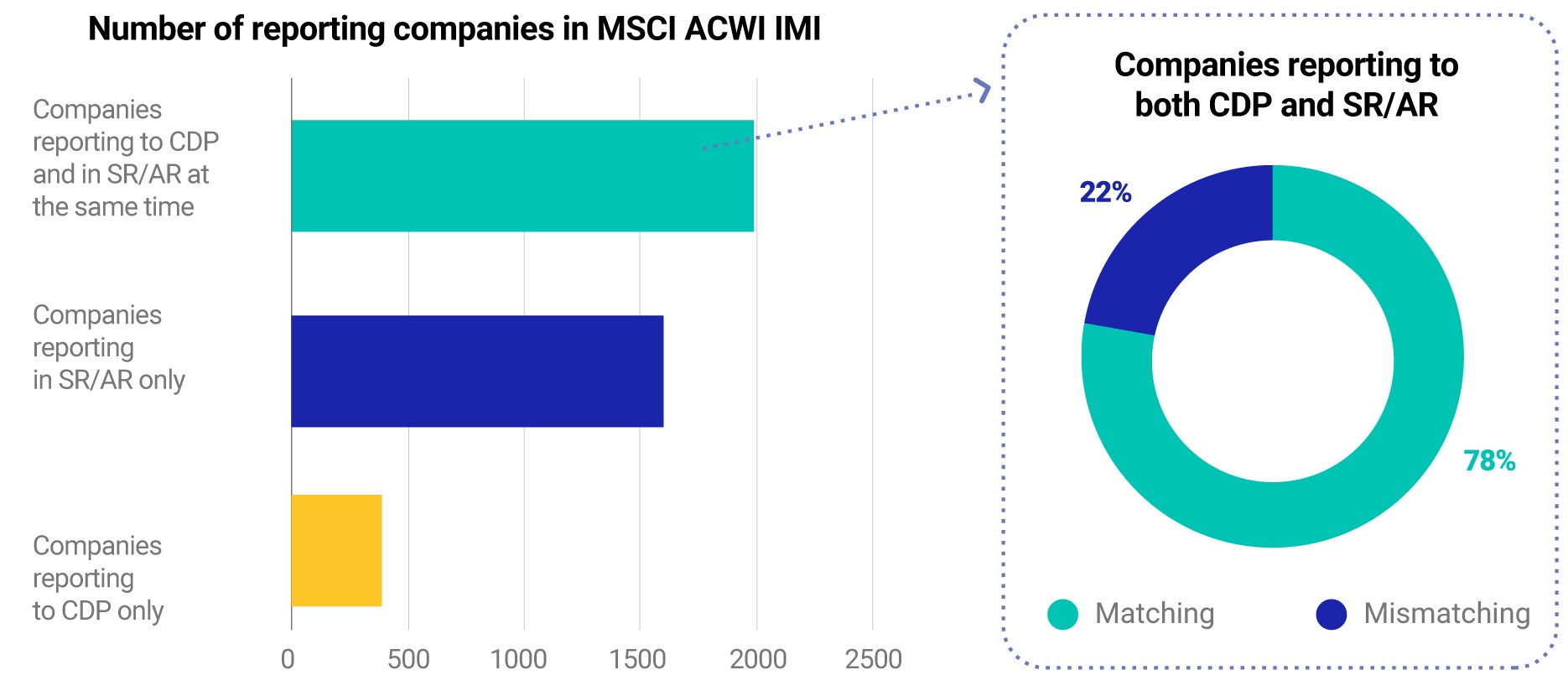

For the MSCI ACWI IMI, 44% of the companies reported a GHG footprint in at least one of the three scopes.3 Approximately 22% of constituents of the MSCI ACWI IMI that disclosed emissions data both to CDP and in their annual report or sustainability report had a reporting mismatch, meaning that the two datasets were inconsistent, as shown in the exhibit below.

Companies reporting by source for MSCI ACWI IMI

Companies in the MSCI ACWI IMI, as of Jan. 20, 2022. Company disclosures in their sustainability report (SR) or annual report (AR) or to CDP, for fiscal year 2019. Source: MSCI ESG Research LLC

In the case of Scope 3 emissions, we found that data quality and quantity were particularly low. We observed that 69% of the companies reporting to CDP did not disclose Scope 3 emissions, indicating a large reporting gap. The current state of corporate emission disclosures presents a challenge for investors' GHG-footprint analysis, since Scope 3 includes the most important types of emissions for many industries.4

Dealing with data limitations

To help deal with this challenge, data providers have identified measures to enhance the quality and consistency of the GHG data used in climate-related metrics.5

Quality-assurance scheme for reported GHG-emission footprints

Source: MSCI ESG Research LLC

These measures include automated screening for the latest company disclosures, comparing company disclosures to other available sources, defining a hierarchy of sources and reaching out to internal experts or the reporting company for clarification, if necessary. As data coverage is generally low, data gaps may need to be filled with sophisticated estimation approaches to ensure a workable dataset in a large investment universe. For instance, the GHG footprint in a company's annual report may not match the one disclosed on the company's website. To decide which source to use, the quality-management team could reach out to the issuer or decide which information to use based on a pre-defined ranking of sources. For cases where the selection of sources isn't straightforward or to better understand if reporting requirements are fully met, it might still be necessary to consult with internal experts on which footprint is appropriate to use.

Focus on data quality

To help improve climate assessments, data users may need to implement quality-control measures such as regular screening, communication with issuers and prioritizing sources. However, investor demand for improved climate-related data quality is likely to increase in the future. While companies with transparent reporting could be well positioned to respond to growing expectations, companies with weak disclosure might face growing pressure.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The Greenhouse Gas Protocol is a global standard for emission footprints, dividing a company’s GHG footprint into Scope 1 (direct emissions), Scope 2 (emissions from electricity consumption) and Scope 3 (emissions from the value chain). “Technical Guidance for Calculating Scope 3 Emissions.” Greenhouse Gas Protocol, October 2013.

“Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures.” Task Force on Climate-related Financial Disclosures, June 2017.2Kishan, Saijel “Corporate Greenhouse Gas Data Doesn’t Always Add Up.” Bloomberg, Jan. 12, 2022.3Constituents of the MSCI ACWI IMI as of Jan. 20, 2022. GHG footprints for fiscal year 2019.4Measured by the share of the Scope 3 GHG intensity within the total GHG intensity, including all emission scopes. See Bokern, David, Baker, Brendan, and Panagiotopoulos, Antonios. “A Major Step Forward for Scope 3 Carbon Emissions.” MSCI Research Insight, Oct. 20, 2020.5For example, MSCI ESG Research LLC uses GHG emission data in the MSCI Climate Value at Risk and Implied Temperature Rise metrics.

“Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures.” Task Force on Climate-related Financial Disclosures, June 2017.2Kishan, Saijel “Corporate Greenhouse Gas Data Doesn’t Always Add Up.” Bloomberg, Jan. 12, 2022.3Constituents of the MSCI ACWI IMI as of Jan. 20, 2022. GHG footprints for fiscal year 2019.4Measured by the share of the Scope 3 GHG intensity within the total GHG intensity, including all emission scopes. See Bokern, David, Baker, Brendan, and Panagiotopoulos, Antonios. “A Major Step Forward for Scope 3 Carbon Emissions.” MSCI Research Insight, Oct. 20, 2020.5For example, MSCI ESG Research LLC uses GHG emission data in the MSCI Climate Value at Risk and Implied Temperature Rise metrics.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.