- While the entire equity market suffered during the sell-off in March, the magnitude of the impact varied for different stocks.

- Style factors, sectors and countries all contributed to the differentiation between best- and worst-performing stocks during this period.

- Large-cap, low-beta and high-quality stocks within defensive sectors fared better in the downturn. Additionally, the worst performers exhibited larger absolute exposures across these factors compared to the winners.

Global equities regained some of their losses after hitting lows in mid-March as the COVID-19 pandemic and related oil-market shocks rippled through the markets. Although the vast majority of equities were in the red, some were "redder" than others. In this blog post, we look at the behavior of the global equity market during the heat of the sell-off to better understand the characteristics of the more resilient stocks during this period.

We used the MSCI ACWI Investable Market Index (IMI), an index of large-, mid- and small-cap stocks across developed and emerging markets, as our universe of equities. Stock returns for the period from Feb. 17, 2020, to March 23, 2020, are used to divide the universe into five equal buckets. The first quintile includes the 1/5 of stocks that performed the worst, and the fifth quintile the stocks that performed the best (or least badly).Global returns by quintile

Data from Feb. 17 to March 23, 2020.

Using the MSCI Barra Global Equity Model for Long-Term Investing (GEMLT), a fundamental-factor model, we investigate the characteristics that separate the quintiles. We calculate the style-factor, sector and country exposure of each quintile by averaging the exposures of individual stocks within them.

Looking at the exhibit below, all but two of the 16 style-factor exposures for the fifth quintile (best performers) and first quintile (worst performers) display as opposites of each other, suggesting that most of the style factors played a role in differentiating winners from losers (relatively speaking). Also, the asymmetry between the two quintile exposures was mainly from the first quintile (worst performers), which showed larger absolute exposures than the fifth.

Differences in style-factor exposure for best and worst performers over the analysis period

Factors found in first- and fifth-quintile stocks

Beta and size were two factors which clearly differentiated stocks between the two quintiles. Two other factors that also represent some differentiation between the two quintiles were value (measured by book-to-price) and quality.

Looking at sectors, more than 50% of stocks in the energy sector appeared in the worst-performing quintile. This was not too surprising as the demand for energy was hampered due to COVID-191 and exacerbated by the feud between Russia and Saudi Arabia, which further pushed down the price of oil in March.

The best performers during this period were more defensive, including consumer staples, utilities and health care (for obvious reasons). There was also differentiation at the industry level. For instance, airlines (an industry within industrials) was one of the worst-performing industries. See our previous research for details of industry factor performance during the current crisis. Sector exposures for best and worst performers over the analysis period

Country exposures also mattered

The exhibit below shows similar analysis at the country level. The color for each country is an indication of its representation in the best- versus worst-performing quintile. China — although the original epicenter — fared the best with 70% more presence in the best- versus worst-performing quintile during the period.

Percentage of best- to worst-performing quintiles by total stocks in different countries

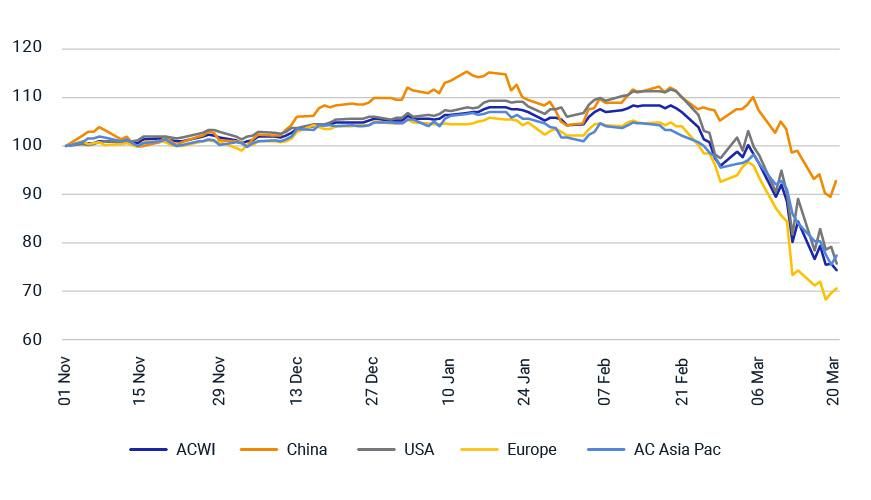

To see whether China's unexpected performance was due to the time frame of the analysis, the exhibit below shows the performance of different regions from Nov. 1, 2019, to March 23, 2020. The chart shows China outperformed and Europe underperformed, perhaps reflecting their approach and capabilities in dealing with a pandemic (i.e., in China the impact was contained in a very specific region) and the potential short- and long-term impact on their economies.

Regional reactions over the course of the pandemic

Market turmoil we saw during the period of analysis had a negative impact on the global equity markets as a whole. The magnitude of the impact, however, varied for different stocks and the difference was largely attributed to common characteristics of the stocks. Using GEMLT, we contrasted winners with losers from the perspective of their factor exposures. The results were quite intuitive: Large-cap, low-beta and high-quality stocks within defensive sectors fared better in the downturn. Additionally, the worst performers exhibited larger absolute exposures across these factors compared to the winners.

The period used for the analysis covers exceptional volatility in global markets, characterized by many large negative-return days but also occasional large positive-return days. Using different end dates could result in different numbers, but what is clear is that style factors, sectors and countries all contributed to the differentiation between the best- and worst-performing stocks during this period.

The author thanks Waman Virgaonkar for his contribution to this blog post.