Review of returns across asset classes – first quarter 2016

Blog post

April 20, 2016

On a quarterly basis, MSCI reviews the principal asset classes in the preceding three months through the prism of MSCI's factor models, which are used by investors to manage risk and construct portfolios. The models cover global equities, bonds, commodities and currencies.

Overall, the performance of factors in the first quarter of 2016 reflected investors' concerns about future growth and their expectation of low inflation.

EQUITY FACTORS

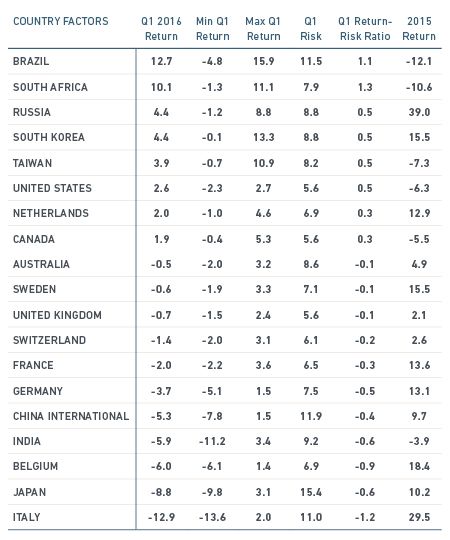

Country factors

The performance of country-factor returns over the first three months of the year underscored investors' concerns with the outlook for economic growth across Europe, Japan and China (Exhibit 1). Within Europe, Italy experienced the steepest decline (-12.9%), compared with a nearly 30% gain in 2015. Germany and France fell 3.7% and 2%, respectively.

The Brazil equity factor rebounded over the quarter and returned 12.7% to erase a 12% loss in 2015. Despite the country's economic woes, investors may be pricing in prospects for a change in the government and reforms that could follow.

EXHIBIT 1: COUNTRY FACTOR RETURNS (%)

All returns are shown in local currency terms

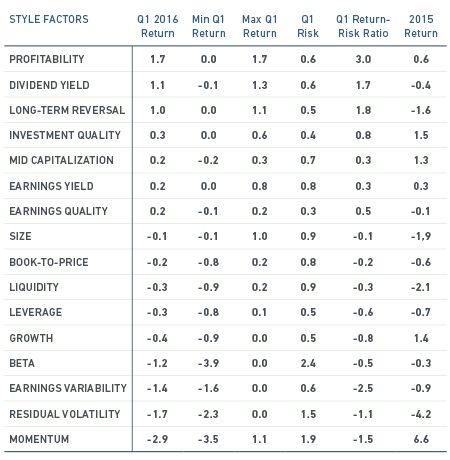

Style factors

Factors that embody defensive styles, including low volatility and quality, outperformed factors that tilt toward such growth-sensitive styles as momentum and value, amid a volatile quarter for equity markets (Exhibit 2). The underperformance of momentum also may be the result of crowding in the strategy, as signaled by MSCI's scorecard in the previous quarter. The observed dispersion in style factor returns could be consistent with investors' fears of a global economic slowdown.

EXHIBIT 2: GLOBAL EQUITY STYLE FACTOR RETURNS

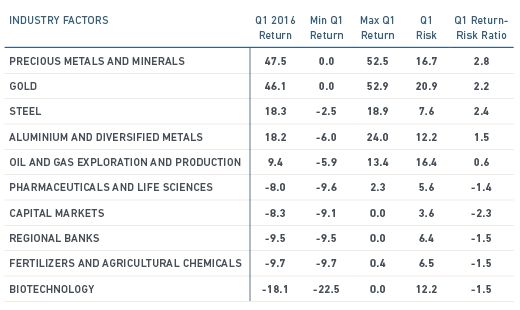

Industry factors

The quarter showed dispersion in the performance across industry factors (Exhibit 3). Returns on precious metals (47.5%) and gold (46.1%) topped the list as investors sought to insure against macroeconomic uncertainty. Returns for regional banks (-9.5%) and capital markets (-8.3%), which ranked among the worst-performing factors, appeared to reflect defaults in loans to borrowers hit by the falloff in oil prices and uncertainty about the long-term profitability of banks in a negative interest rate environment.

Biotechnology and pharmaceuticals fell 18.1% and 8.0%, respectively. The drop appeared to reflect concerns that a rise in the cost of prescription drugs in the U.S. could lead the government to take steps to constrain prices.

EXHIBIT 3: GLOBAL INDUSTRY FACTOR RETURNS

Fixed Income, currency and commodity FACTORS

Bond factors

Factor returns for bonds reflected investors' perception of a slowdown in global growth and the continuation of lowflation, which sent nominal and real yields down across markets (Exhibits 4 and 5).

Lower yields signified demand for – and shortage of –government bonds and other assets that investors perceived as safe. Yields also reflected the response by central banks to the persistence of slow growth and low inflation. The U.S. Federal Reserve responded by delaying further interest-rate hikes, while central banks in Europe and Japan cut short-term rates to below zero.

EXHIBIT 4 : GOVERNMENT BOND SHIFT FACTOR RETURNS

All returns are shown in local currency terms

EXHIBIT 5: GOVERNMENT INFLATION-LINKED BOND SHIFT FACTOR RETURNS

All returns are shown in local currency terms

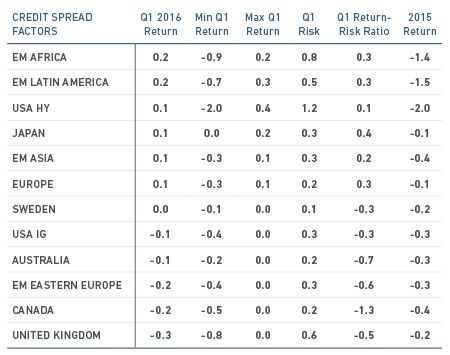

Credit spread factors

Credit spread factors changed little over the quarter (Exhibit 6). One exception: a divergence in spreads between the high-yield and investment-grade sectors in the U.S. The deviation reflected the impact of low oil prices on the high-yield issuers and flows of capital to investment-grade issuers in the U.S. and U.K. The change also reflected investors' searching for alternatives to negative rates on government bonds across most developed-market economies outside the U.S. and U.K.

EXHIBIT 6: CREDIT SPREAD FACTOR RETURNS

All returns are shown in local currency terms

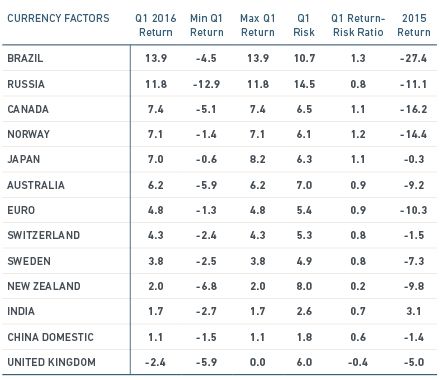

Currency factors

The Brazilian real experienced the strongest appreciation against the U.S. dollar during the first quarter amid an uptick in expectations by investors of changes in the government that could lead to economic reforms (Exhibit 7). The performance marked a reversal from 2015, when the real fell to a record low against the dollar amid a recession and inflation that continue to plague Brazil's economy.

One surprise: the appreciation of the yen despite deflation and sluggish growth. The change appeared to reflect investors' viewing the currency as a safe haven amid uncertainties about prospects for growth in Japan and worldwide.

The British pound depreciated during the quarter. The drop may have reflected investors' assigning a greater probability that Britons will vote this June to leave the European Union.

EXHIBIT 7: CURRENCY FACTOR RETURNS (RELATIVE TO THE U.S. DOLLAR)

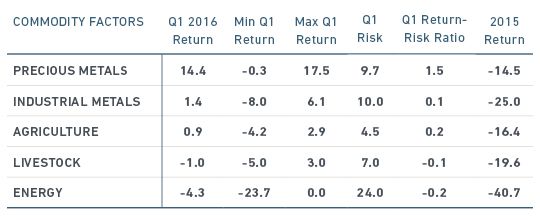

Commodity factors

The energy factor dipped 4.3% during the first three months of 2016, which marked the fifth straight quarter of decline (Exhibit 8). Precious metals outperformed all other sectors. The rise reflected demand by investors for insurance in a market marked by macroeconomic uncertainty and volatility.

EXHIBIT 8: COMMODITY FACTOR RETURNS

For more information, please contact:

Roman Kouzmenko

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.