Santander’s Coco extension: The New Market Norm?

Blog post

March 18, 2019

On Feb. 12, Banco Santander announced it would extend — i.e., not call — its additional-tier-one contingent-convertible (coco) bond issuance SAN Mar 19.1 The news media depicted the event as upending banks' standard practice of calling bonds on their first call date.2 But was the market caught off guard, and is Santander's decision a watershed in the evolution of the USD 200-billion coco market? Despite the media reaction, markets did not seem altogether surprised that Santander extended its coco issue.

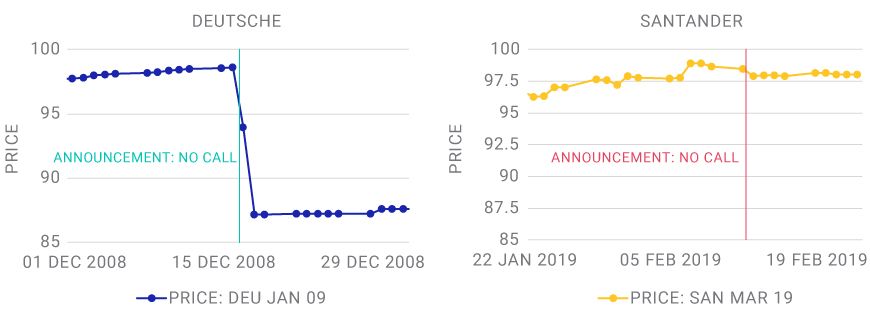

The coco market is still relatively young, and extensions have so far been infrequent. A previous well-known extension occurred a decade ago, when Deutsche Bank AG decided not to call one of its hybrid capital bonds (DEU JAN 09) — an event that resulted in a sharp decline in the bond's price. In contrast, the recently observed price swings in the SAN Mar 19 coco issue were relatively small.

MUTED MARKET REACTION TO SANTANDER'S COCO EXTENSION

Source: Refinitiv

The Santander coco bond's relative price stability might be a sign that the market has changed and extensions may become more common. Indeed, European regulators had seemed to encourage issuers to make call decisions based on "economic" rather than "reputational" considerations, according to a strategist quoted recently by Reuters.3

Thus, changing market conventions and regulatory expectations perhaps signal that investors now have an additional portfolio-management consideration: extension risk. There is indeed uncertainty around call decisions: While the Santander issue was extended, KBC Group NV recently announced that it will call its coco bond.4

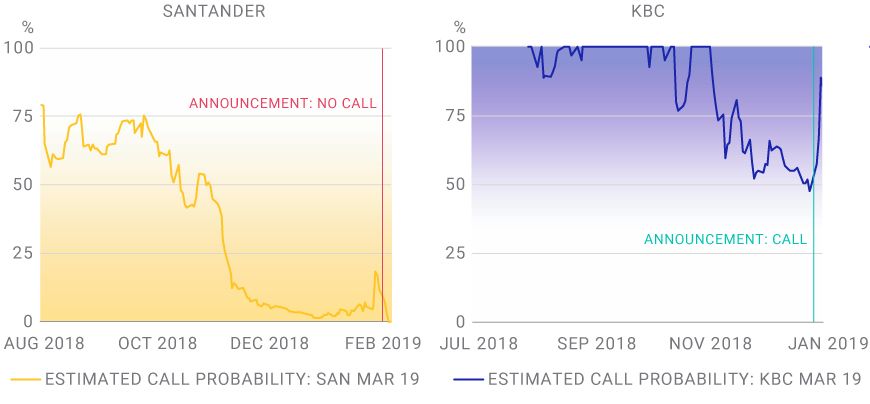

MODELING CALL PROBABILITIES

Models are designed to draw on market prices and other metrics to provide insight on call probabilities. This information may be used to complement accounting information, such as the funding situation of the issuer, or anecdotal information, such as how keenly the issuer participates in the coco market. To illustrate, we compare forecasted call probabilities prior to the announcement of the call decision for the extended Santander issue and for the issue KBC said it will call.

PRE-ANNOUNCEMENT CALL PROBABILITIES

Source: Refinitiv

Our model had forecasted uncertainty over both banks' call decisions. In the case of Santander, however, the model projected the distinct possibility that Santander would not call the bond. In the case of KBC, however, the model exhibited much less certainty. It should be noted that neither of these results should be used as an indicator of the potential future performance of such models.

The relatively minor price swing in Santander's bond hinted that the coco market was not surprised by the bank's extension. Extension risk on coco bonds may become a more common concern, as issuers increasingly focus on the economics of calling (or not calling) their bonds. Modeling the chance of an extension can help investors evaluate the risks of an extension.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 We refer to bonds by their first call dates rather than their designated maturities, as is otherwise common.2 “How Santander kept a $200bn bond market guessing.” The Financial Times, Feb. 13, 2019.3 “Banco Santander opts to roll-over CoCo bond.” Reuters, Feb. 12, 2019.4 “KBC to call Additional Tier-1 (AT1) securities it issued in 2014.” KBC, Jan. 21, 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.