Senior bonds in name only

Blog post

October 2, 2019

- Too-big-to-fail European banks have started issuing a new layer of debt to respond to changing regulations: senior non-preferred bonds.

- As SNP bonds are required to be written down to absorb losses, their recovery rates differ from those of traditional senior debt.

- This recovery risk is captured by our analysis, which suggests an increased sensitivity during market stress.

Too big to fail, but we won't pay for it

In order to protect taxpayers and avoid another government bailout of too-big-to-fail banks, the Financial Stability Board and regulators prescribed additional total loss-absorbing capacity (TLAC) for global systemically important banks (G-SIBs).1 To help meet TLAC requirements, impacted European banks began issuing the new SNP bonds.2

Unlike other loss-absorbing capital, such as contingent-convertible bonds, SNP bonds cannot be written down without triggering a default. However, their defining characteristic is that, in the event of default, they are required to be written down to absorb losses. This means that their expected recovery rate is less than that of traditional senior bonds — one example of the phenomenon of recovery risk.

SNPs reacted negatively to periods of risk aversion

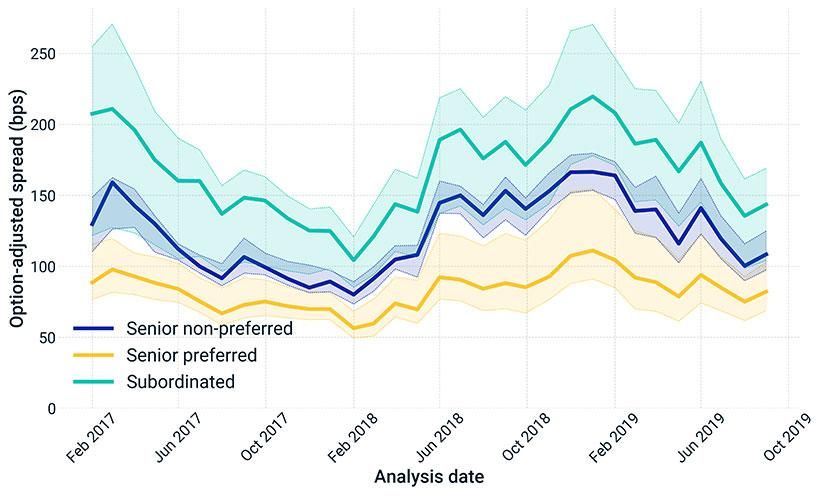

The market view on the recovery rate for SNP bonds can be seen indirectly by comparing the spreads of traditional senior and SNP bonds, as shown in the exhibit below.

Spread trends show market expects lower recovery rate for SNP bonds

The median option-adjusted spread of bonds in the Markit iBoxx EUR Banks Index by seniority groups. Shaded bands around the median represent the Q1-Q3 interquartile range. Month-end data. Source: IHS Markit

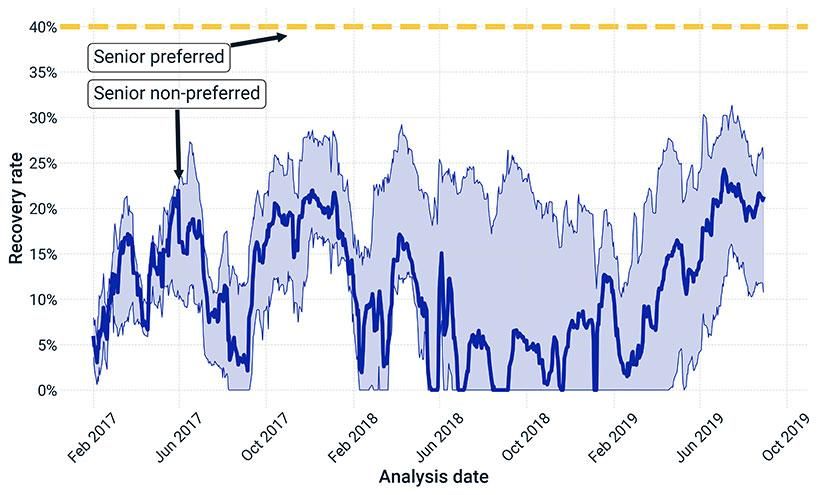

However, a more direct measure is the market's expected recovery rate, as this is where SNP bonds differ from traditional senior bonds. The next exhibit displays the median implied recovery rate based on senior-preferred/SNP bond pairs.3

Implied SNP recovery rates fell steeply during market stress

Median implied recovery rate for SNP bonds. The shaded band represents the 10/90 percentile range. Source: IHS Markit

The distinct recovery dynamics are clearly visible: While there is a dispersion across various assets, we can identify trends. Starting from the first SNP issuances, the market priced in a lower recovery rate compared to traditional senior bonds, reflecting SNPs' relative position in the capital structure. However, during the more risk-averse periods in 2018, the typical implied recovery rate shrank to levels close to zero, followed by a recent surge in 2019, indicating SNPs' increased sensitivity to risk aversion during market stress.

In sum, the choice to invest in SNP bonds depends on investors' appetites for recovery risk; valuation and risk measures can take this risk into account.

Other institutions with different regulatory demands and firm structures chose structural subordination, where the additional capacity is issued via the holding company and thus subordinated to the senior debt of the bank.

3A credit-triangle relationship was used (spread = (1 – recovery rate) * hazard rate). The hazard rate is the same for senior-preferred and SNP bonds. For illustrative purposes, we assumed a 40% recovery rate for all senior-preferred bonds in the sample. Implied SNP recovery rates were floored at 0. Bond pairs from the same issuers with close maturity times were selected.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The Financial Stability Board set G-SIBs’ TLAC at 16% of risk-weighted assets starting from Jan. 1, 2019, with the level rising to 18% at the beginning of 2022. At least 33% of TLAC must come from unsecured debt instruments earmarked for bail-in, or bondholder-borne losses in the event of the bank’s resolution. “Principles on Loss-absorbing and Recapitalisation Capacity of G-SIBs in Resolution: Total Loss-absorbing Capacity (TLAC) Term Sheet.” Financial Stability Board, Nov. 9, 2015.

A parallel, European Union regulation is the minimum requirement for own funds and eligible liabilities (MREL). For the latest addendum to the requirements, see “Minimum Requirement for Own Fundsand Eligible Liabilities (MREL): Addendum to the SRB 2018 MREL policy.” Single Resolution Board, June 25, 2019. on new CRR requirements.2

A parallel, European Union regulation is the minimum requirement for own funds and eligible liabilities (MREL). For the latest addendum to the requirements, see “Minimum Requirement for Own Fundsand Eligible Liabilities (MREL): Addendum to the SRB 2018 MREL policy.” Single Resolution Board, June 25, 2019. on new CRR requirements.2

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.