Stress-Testing Risk-Parity Strategies

Blog post

February 16, 2018

The recent surge in volatility took some investors by surprise: The level of the VIX doubled in a day, and put an end to some strategies that involved short selling of the VIX. But larger exposures to rising volatility may be hiding elsewhere, including in volatility targeting and risk-parity strategies designed to better balance risk across asset classes. We stress tested potential scenarios to explore the vulnerabilities of these strategies to a sharp increase in the inflation rate.

A potential problem with investment strategies that rely on volatility to set asset class exposures is that they could exacerbate market turmoil by creating "feedback loops."1 Strategies such as volatility targeting and risk parity can drive stock sales when volatility rises, creating the potential to drive equity-market volatility even higher. Such strategies are estimated to have reached 1 trillion USD under management,2 dwarfing the approximately USD 10 billion directly exposed to the VIX. Deleveraging these portfolios could have a more harmful effect on the stock market than short volatility ETFs, which suffered heavy losses.

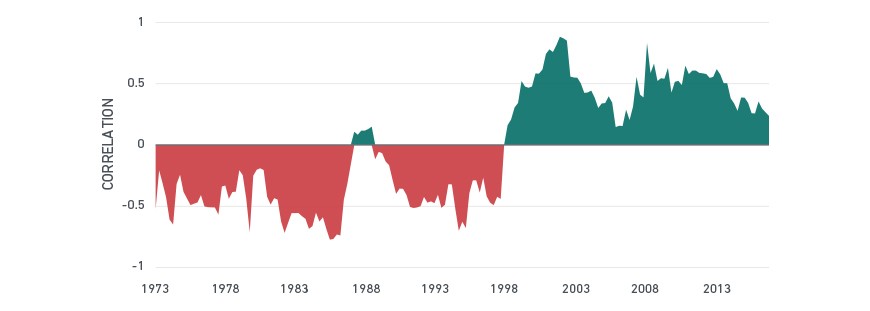

Risk-parity funds attempt to equalize the contribution of bonds and equities to the total risk. The resulting portfolio might be levered up to obtain a target volatility. Such strategies also benefit from positive correlation between equity and bond yields, which can provide a partial hedge. If this correlation breaks down, losses could mount as bonds no longer mitigate stock-market losses but potentially aggravate them. Historically, the correlation between the 10-year Treasury yield and MSCI USA Index has varied over time — it was largely negative from 1973-1998 and then positive since 1998, as can be seen in the exhibit below.

The correlation between U.S. equity and 10-year Treasury yield has varied over time

Source: MSCI, U.S. Department of the Treasury

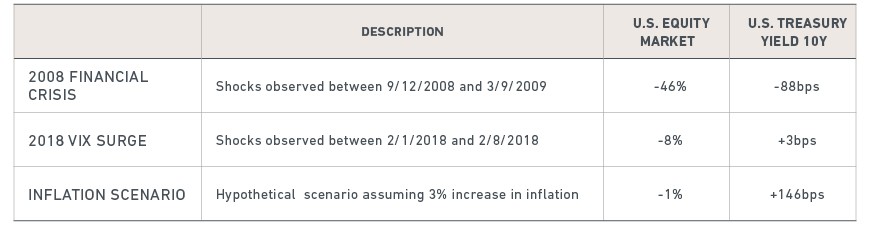

We examine three scenarios using MSCI's stress-testing capabilities. We model the recent volatility surge and compare it to the 2008 financial crisis and a hypothetical scenario that assumes a steep increase of 3% in the inflation rate.3

What might happen to markets if inflation rises?

Source: MSCI RiskManager

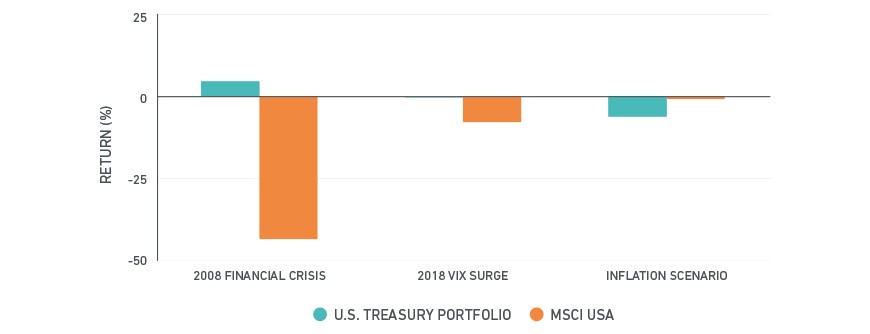

We apply these scenarios to two portfolios: a classic 60% U.S. equity/40% Treasury bond split4 and a simulated risk-parity strategy.5 First, let's look at bond and equity portfolio returns. While Treasurys partially offset the losses on the equity portfolio in 2008, this negative correlation did not hold in the first half of February 2018, as bond prices declined slightly. Under the hypothetical inflation scenario, the correlation is reversed: Bonds would lose even more than equities.

Shifting correlations: Asset class returns under various scenarios

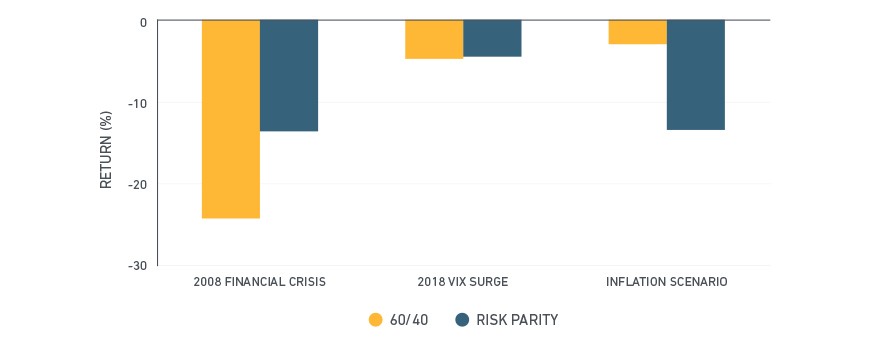

While this breakdown in correlations and decreased diversification also affects the 60/40 strategy, the implications for risk-parity strategies are more significant, as we can see in the exhibit below. A risk-parity strategy suffered only about half the loss of a 60/40 portfolio in the 2008 crisis, but barely outperformed in the recent volatility spike. Under the inflation scenario, which hurts bonds more severely than equities, the risk-parity portfolio's loss is roughly four times larger than that of the 60/40 portfolio, because of its overweighting of Treasurys.

The effect of changing regimes on 60/40 and risk-parity strategies

While the recent volatility spike has hit short volatility trades hard, much larger strategies without direct VIX exposures may be vulnerable to increasing volatility or changing correlations. Given the sheer size of these strategies, such unanticipated regime changes could have potentially stark consequences.

This blog post was written in collaboration with Thomas Verbraken.

1 For example, see Cole, C. (2015). "Volatility and the Allegory of the Prisoner's Dilemma." Artemis Capital Research.

2 Burger, D. "Map to the Underworld: $2 Trillion of Volatility Trades here." Bloomberg Markets, Feb. 7, 2018. https://www.bloomberg.com/news/articles/2018-02-07/a-map-to-the-underworld-2-trillion-of-volatility-trades-here

3 Suryanarayanan, R., C. Acerbi, T. Verbraken. (2015). "The Fed Rate Hike: Implications for U.S. and Global Multi-Asset Class Portfolios." MSCI Research.

4 We proxy the equity portfolio with the MSCI USA Index and the government bond portfolio with the ICE BofAML US Treasury Master Index.

5 We created a portfolio in which equities and bonds contribute equally to the total risk, resulting in a 20%/80% allocation to equities and bonds, respectively. This portfolio was levered up to obtain the same volatility as the 60/40 equity/bond portfolio.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.