- In the last week of February, markets and factors outside Asia reversed an initial mild response to COVID-19. We found significant effects for industry, style and country factors.

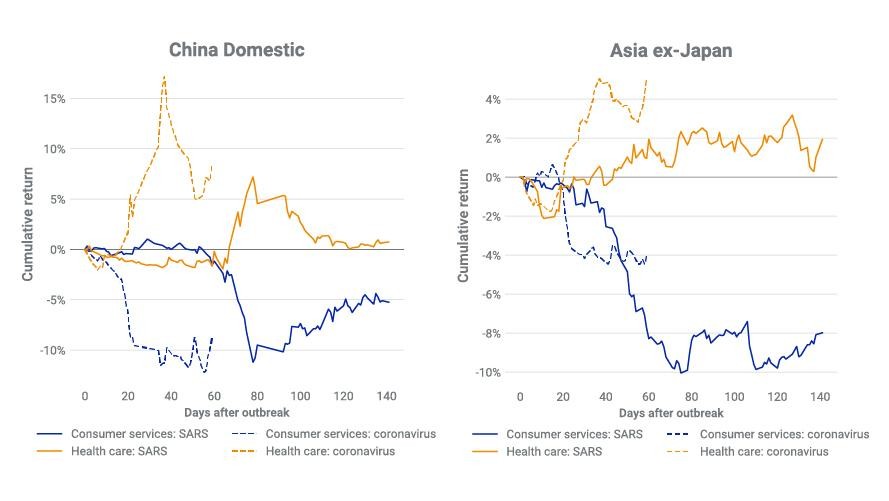

- During the SARS outbreak, we observed strong divergence between consumer services and health care companies for about one month, followed by reversal for several months in the most impacted countries.

- In the three most recent periods of sharp volatility spikes, volatility reverted to moderate levels in weeks or days. In other periods, it took months; after the 2008 crisis, it took over a year for volatility to moderate.

As the number of coronavirus cases continues to grow, fears of a global pandemic and ensuing economic impacts have increased, causing sharp drawdowns in many global markets, which had initially showed only a mild response at the start of the epidemic. For example, in the last week of February, the U.S. market fell by over 10% and companies in the consumer services and airline industries fell by significantly more while health care companies fared better. In addition, on Feb. 28, 2020, the Cboe VIX® index closed above 40 for the first time in over four years.

Following up on our previous post on COVID-19,1 we use MSCI's Barra® Global Total Market Equity Trading Model (GEMTR) and other MSCI equity factor models to understand the market movements from a factor perspective. Using the SARS epidemic as an analogue, along with other periods of elevated market volatility, we also investigate the time scale at which factor returns and volatility reverted in the past.Industry factors moved most during the last week of February

Consistent with what we observed at the start of the epidemic, during the last week of February we saw the largest moves in industry factors, including consumer services, airlines and health care. The exhibit below displays the returns of the most impacted industry, country and style factors during that period, based on GEMTR.

Industry, country and style factor returns

Data from Feb. 24 to Feb. 28, 2020. Industry and country returns are net of the overall global market. Returns are standardized (converted to z-score, or number of standard deviations, by dividing factor return by forecast factor risk) to facilitate comparison across factor buckets. For readability, we show only the top and bottom 12 factors for industries. For countries, we show developed market countries plus China, South Korea and Taiwan.

After moving only mildly at the start of the epidemic, we have now seen large moves globally in the same factors that earlier responded sharply in Asia. We examined industry, style and country factors.

- Industry factors: In the last week of February, the drop in airlines globally was over eight standard deviations and consumer services fell by over six standard deviations. The moves were not as dramatic on the positive side, but some industries in the health care and consumer staples sectors gained by two or more standard deviations.

- Style factors: Both beta and residual volatility made large negative moves as has been typical during previous large market drops, but the movements in other traditional style factors such as momentum, earnings yield, size and earnings quality were unremarkable. The large negative move in the liquidity factor indicates that "hot stocks" — those with very high trading volume for their size — sold off much more than "neglected stocks" — those with low trading volume for their size. This suggests investors may have sold off the most liquid names in their portfolios first to raise cash in response to a rapidly changing market.

- Country factors: Those in Asia and the greater China region fared best, including China, Hong Kong, Taiwan and Singapore, perhaps because the impact of the epidemic had already been priced in during the early stages of the epidemic. In contrast, those in Europe and the Americas, which fell very little at the start of the epidemic, suffered the most during the last week of February.

Time scale of reversion in factor returns

We can't predict future market moves, but we can examine past behavior to provide perspective and gauge possible scenarios if the current situation were to unfold similarly to past episodes. As we showed in our previous post, we observed strong reaction and initial divergence between consumer services and health care in Asian markets. Below, we show the cumulative returns to consumer services and health care in China (left) and greater Asia ex-Japan (right) during the SARS episode and the current epidemic. Consumer services and health care returns

Data from Dec. 31, 2019 to Feb. 28, 2020, for coronavirus, and from February 2003 to June 2003 for SARS.

During the SARS episode, the strong divergence between consumer services and health care lasted approximately one month, followed by slow convergence or stabilization. Since the first case of COVID-19 was reported over two months ago, we observed strong divergence for approximately three weeks, followed by stabilization or even reversion in the last three weeks. The market response in the current episode has occurred more rapidly. To gain further insight as to the time frame of reversion, we next examine the behavior of reversion in volatility during previous periods of market crisis or elevated volatility.

Historical time scale of reversion in volatility

No one knows whether the VIX's over-40 close on Feb. 28, 2020, will represent the peak in volatility for this event, or simply the first date the VIX closes above 40. Here we study the time scale for mean reversion in volatility from elevated levels in past events. To start, we examine the evolution of the MSCI US Total Market Model (USTMM) volatility forecasts along with VIX. The USTMM comes in several flavors of responsiveness — USFAST, USMED and USSLOW — targeting varying investment horizons. As the name suggests, USFAST is the most responsive to market moves while USSLOW is the most stable.

Volatility over time

As expected, we see that the USSLOW forecasts were the most stable and moved least during spikes in market volatility, while USFAST responded quickly to spikes in volatility and at times exceeded VIX during moderate spikes. The USFAST forecast also tended to revert more quickly than VIX after large spikes in volatility. To study the time scale of mean reversion in volatility more precisely, we selected periods when the VIX rose above 40 (or near 40 for the two episodes in 2018) and then examined the evolution of volatility from the first date the VIX closed above 40 (or from its peak for the two episodes in 2018).

In the exhibit below, we see that, on average, it took about six months for the VIX to close below 20 following the event date, but there was a very wide range in this duration. More recent spikes in volatility subsided much more rapidly — in a matter of weeks rather than months.

Previous high volatility events

We define "Event date" as the date the VIX first closed above 40 during the given event (or reached its peak for the events in 2018). "Trading days to VIX peak" is defined as the number of days from the event start date to the date of peak VIX close of the event. "Trading days to VIX < 20" is defined as the number of days until the first day the VIX closed below 20 after the event start date.

To view the data visually, we grouped the events into two categories — "fast events" and "slow events" — based on how quickly volatility reverted during each episode. We put the episodes of 2018 and 2015 into the "fast" group and those from the other events into the "slow" group. We then calculated the simple average level of VIX and the USFAST forecast as a function of time from the event date.

In the exhibit below, we see the striking rapidity with which volatility subsided in the recent fast episodes as compared to the slow ones. We also see the USFAST model forecast volatility reverted even faster than VIX, particularly during the "fast" events. This was most pronounced during the February 2018 "Volmageddon" event, which was perhaps driven more by short volatility trades imploding than economic fundamentals, and caused the risk model to find less evidence of risk based on factors than implied by VIX. Therefore, the model's volatility forecast didn't rise as high and also came down more quickly than VIX. We also see that the USFAST forecast volatility and VIX generally moved in tandem, and that VIX typically maintained a volatility risk premium above the USFAST forecast.

Time scale of reversion in volatility from elevated levels

While no two crisis events are identical, we can gain perspective from examining prior periods. If the factor response of the coronavirus event follows what we observed during the SARS epidemic, the divergence between consumer services and health care stocks may have already started to revert in Asia. So far, the evidence supports this hypothesis. Also, if current market volatility follows the trajectory of recent large spikes in volatility, it could revert to more moderate levels quickly — in a matter of weeks rather than months.

Coronavirus impacts on the market

A coronavirus stress test for global markets

The coronavirus epidemic: Implications for markets

Factors separated fact from fiction

The FaCS report

Data from Dec. 31, 2019 to Feb. 28, 2020, for coronavirus, and from February 2003 to June 2003 for SARS.

During the SARS episode, the strong divergence between consumer services and health care lasted approximately one month, followed by slow convergence or stabilization. Since the first case of COVID-19 was reported over two months ago, we observed strong divergence for approximately three weeks, followed by stabilization or even reversion in the last three weeks. The market response in the current episode has occurred more rapidly. To gain further insight as to the time frame of reversion, we next examine the behavior of reversion in volatility during previous periods of market crisis or elevated volatility.

Historical time scale of reversion in volatility

No one knows whether the VIX's over-40 close on Feb. 28, 2020, will represent the peak in volatility for this event, or simply the first date the VIX closes above 40. Here we study the time scale for mean reversion in volatility from elevated levels in past events. To start, we examine the evolution of the MSCI US Total Market Model (USTMM) volatility forecasts along with VIX. The USTMM comes in several flavors of responsiveness — USFAST, USMED and USSLOW — targeting varying investment horizons. As the name suggests, USFAST is the most responsive to market moves while USSLOW is the most stable.

As expected, we see that the USSLOW forecasts were the most stable and moved least during spikes in market volatility, while USFAST responded quickly to spikes in volatility and at times exceeded VIX during moderate spikes. The USFAST forecast also tended to revert more quickly than VIX after large spikes in volatility. To study the time scale of mean reversion in volatility more precisely, we selected periods when the VIX rose above 40 (or near 40 for the two episodes in 2018) and then examined the evolution of volatility from the first date the VIX closed above 40 (or from its peak for the two episodes in 2018).

In the exhibit below, we see that, on average, it took about six months for the VIX to close below 20 following the event date, but there was a very wide range in this duration. More recent spikes in volatility subsided much more rapidly — in a matter of weeks rather than months.

Previous high volatility events

We define "Event date" as the date the VIX first closed above 40 during the given event (or reached its peak for the events in 2018). "Trading days to VIX peak" is defined as the number of days from the event start date to the date of peak VIX close of the event. "Trading days to VIX < 20" is defined as the number of days until the first day the VIX closed below 20 after the event start date.

To view the data visually, we grouped the events into two categories — "fast events" and "slow events" — based on how quickly volatility reverted during each episode. We put the episodes of 2018 and 2015 into the "fast" group and those from the other events into the "slow" group. We then calculated the simple average level of VIX and the USFAST forecast as a function of time from the event date.

In the exhibit below, we see the striking rapidity with which volatility subsided in the recent fast episodes as compared to the slow ones. We also see the USFAST model forecast volatility reverted even faster than VIX, particularly during the "fast" events. This was most pronounced during the February 2018 "Volmageddon" event, which was perhaps driven more by short volatility trades imploding than economic fundamentals, and caused the risk model to find less evidence of risk based on factors than implied by VIX. Therefore, the model's volatility forecast didn't rise as high and also came down more quickly than VIX. We also see that the USFAST forecast volatility and VIX generally moved in tandem, and that VIX typically maintained a volatility risk premium above the USFAST forecast.

Time scale of reversion in volatility from elevated levels

While no two crisis events are identical, we can gain perspective from examining prior periods. If the factor response of the coronavirus event follows what we observed during the SARS epidemic, the divergence between consumer services and health care stocks may have already started to revert in Asia. So far, the evidence supports this hypothesis. Also, if current market volatility follows the trajectory of recent large spikes in volatility, it could revert to more moderate levels quickly — in a matter of weeks rather than months.