The Value Factor Marks A Decade of Disappointment

Blog post

March 9, 2016

Call it a lost decade. The value factor recently marked 10 years of decline in the U.S.

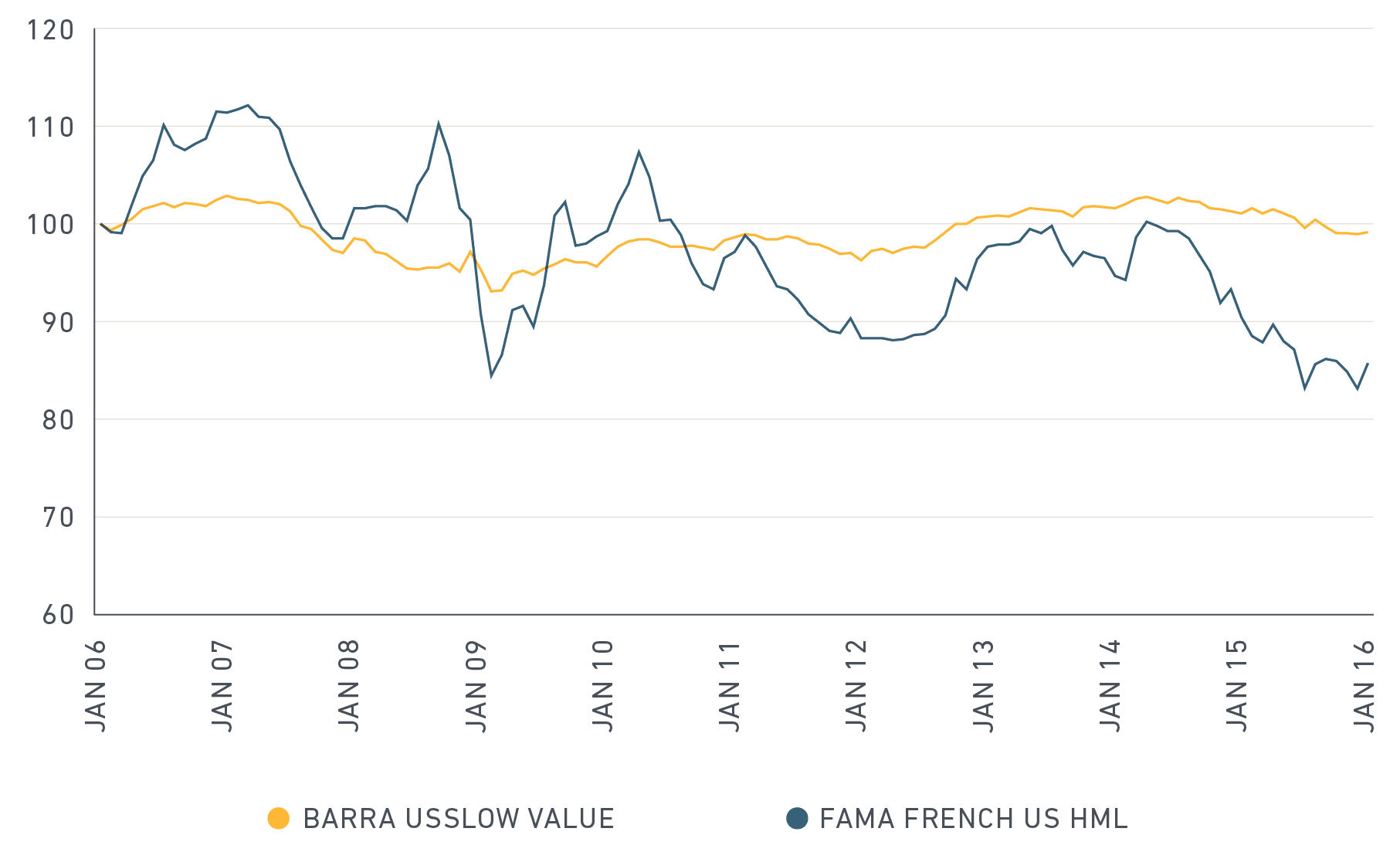

The two most common measures of the value factor: the Fama-French HML factor and the MSCI Barra Value pure factor—both displayed below—point to low returns over the last 10 years, in sharp contrast with the previous decade.

Performance of the value factor (01/31/2006 to 01/29/2016)

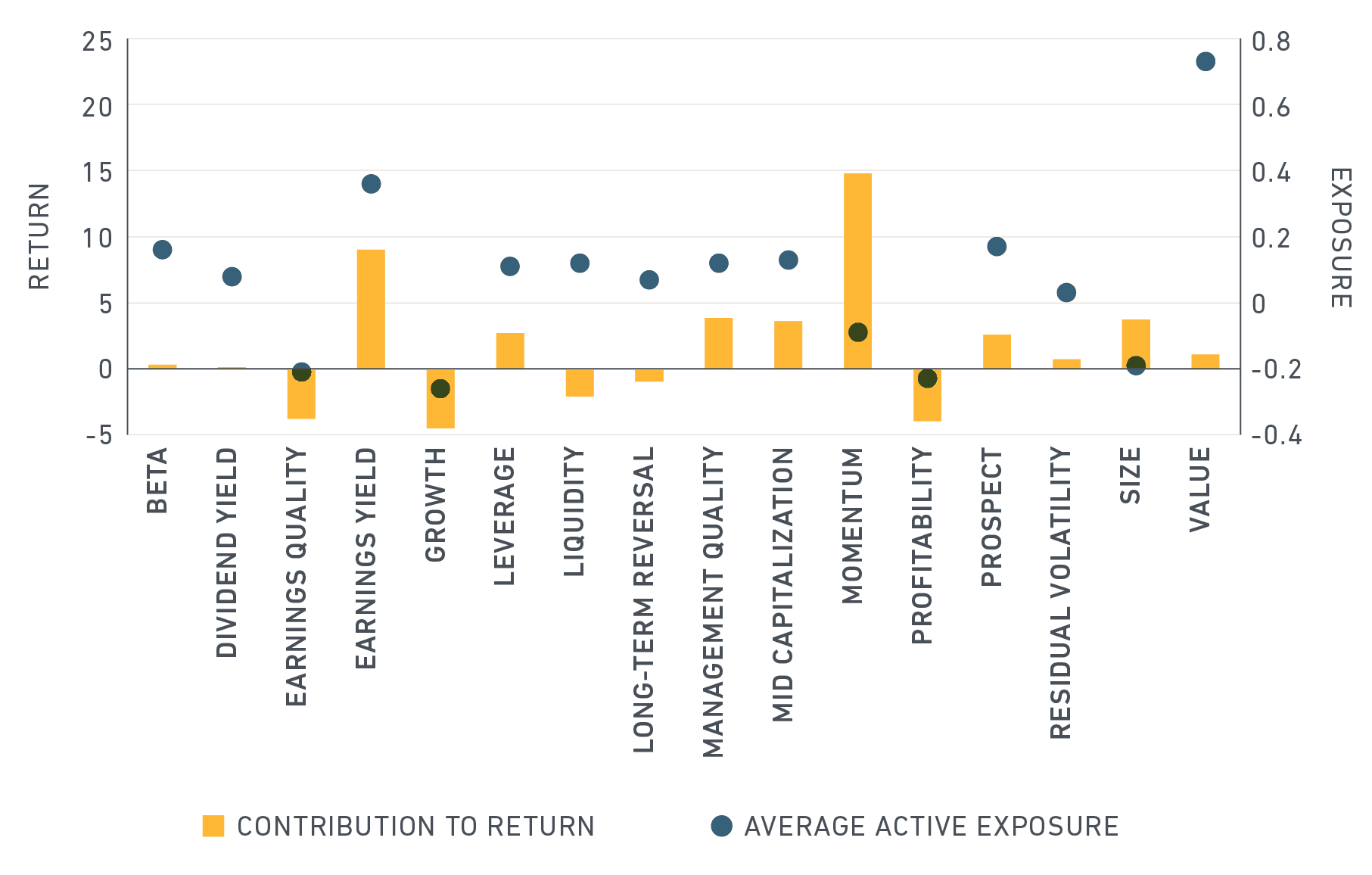

Average active exposure and cumulative contribution to return for MSCI USA Enhanced Value Index using MSCI US Total Market Equity Model for Long-Term Investors (01/31/2006 to 01/29/2016)

The investable indexes that aim to reflect the value factor, whether through fundamental weighting or a sector-neutral value approach, show this shortfall as well. We can attribute the sources of underperformance of these strategies by examining the MSCI USA Enhanced Value Index, which combines securities of large- and mid-capitalization stocks that have low price-to-book value, price-to-forward earnings, and enterprise value-to-cash flow from operations ratios in a sector-neutral index.

As the chart below shows, the index tilts substantially toward the value factor, as expected. However, the index's relative performance attributed to factors comes primarily from its exposure to momentum and earnings yield, both of which contributed positively to return, whereas value contributed only minimally.

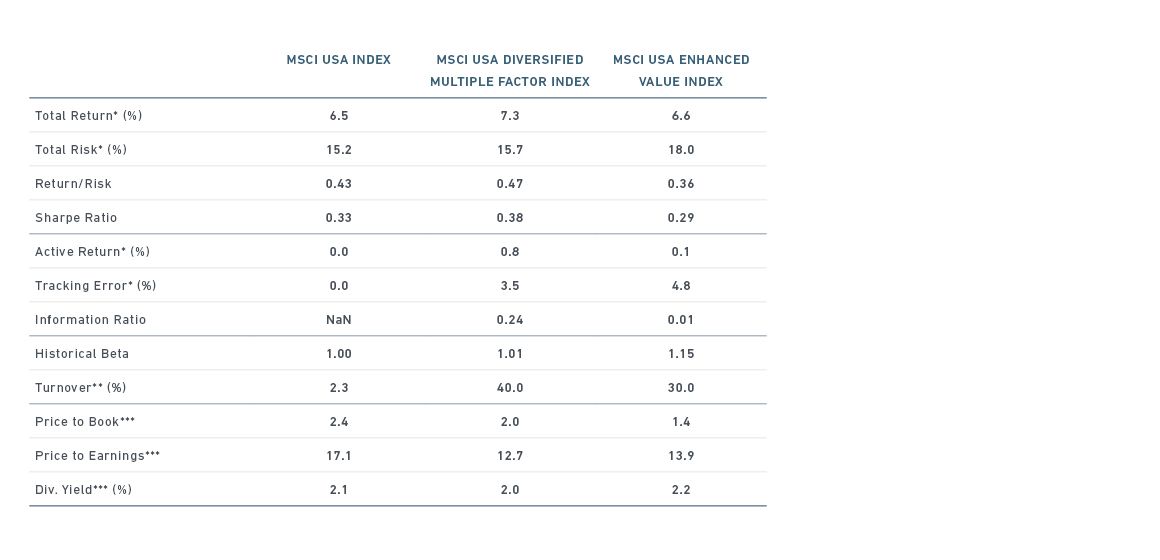

Comparing the MSCI USA Diversified Multiple Factor Index and the MSCI USA Enhanced Value Index

So what to do from here?

At the core of value investing is the belief that relatively cheaply valued assets tend to outperform richly valued assets over a long horizon. As I wrote recently, the value factor, which by definition is inexpensive relative to the market, is particularly inexpensive lately compared with its historical average.

Value has been among the most resilient and well accepted of factors for more than 80 years. In MSCI's experience value almost always appears among factor allocations in institutional portfolios.

The value factor seems likely to revert to its mean eventually based on changes in the macroeconomy. A recent study by MSCI that analyzed the sensitivity of our factor indexes to changes in GDP found that the value factor has exhibited high sensitivity to growth over the long run.

Still, the performance of value over the past decade reminds us that factors can experience long periods of underperformance. The ability to fully capture the risk premium associated with factors requires either extraordinary timing or the ability to remain fully exposed through the whole cycle.

Fortunately for investors, factors cycle independently of one another. That is why MSCI has long highlighted the advantage of combining factors such as value, momentum, quality and low volatility—which display different drivers of performance—into allocations. For example, over the decade that ended Jan. 29, an index that combined value, size, quality and momentum would have returned 7.3% annually compared with 6.6% for one that tilted solely towards value.

*Gross returns annualized in USD for the 01/31/2006 to 01/29/2016 period

**Annualized one-way index turnover for the 01/31/2006 to 01//29/2016 period

***Monthly averages for the 01/31/2006 to 01/29/2016 period

Further reading:

Finding Value: Understanding Factor Investing

Deploying Multi-Factor Index Allocations in Institutional Portfolios

Index Performance in Changing Economic Environments

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.