Time to Rethink Emerging-Markets Allocations?

Blog post

February 23, 2017

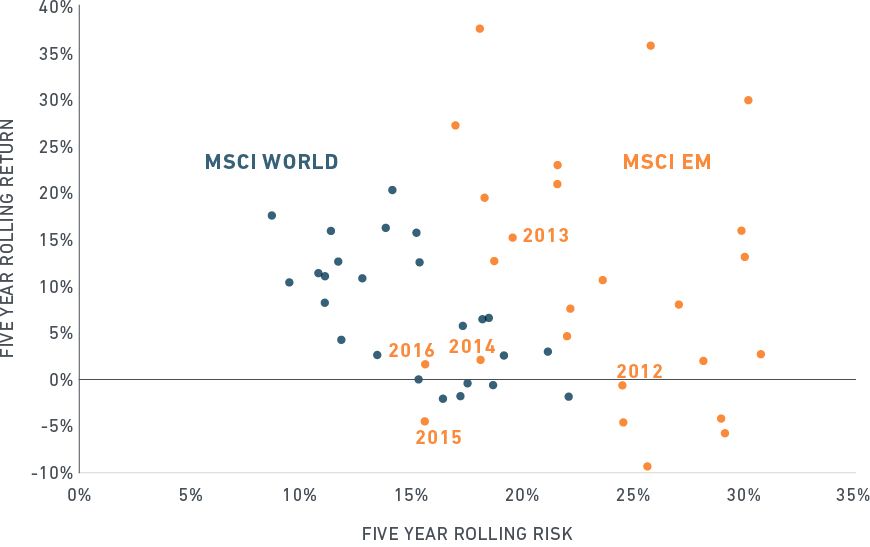

Over the last five years, the risk and return profile of emerging markets has started to resemble that of developed markets (below chart). That leaves many large asset owners to ask how to structure mandates to take advantage of the variation in the behavior of emerging markets.

The risk/return profile of emerging markets has become more like that of developed markets

Points represent rolling, end-of-year annualized return and standard deviation. Data covers December 1992 to December 2016.

Institutional investors face at least three choices in their allocations to emerging markets. They can allocate to an integrated, global equity approach, whether it is active or indexed. They can adopt a dedicated emerging markets allocation. Or they can make active allocations to particular countries within emerging markets.

Global equity approaches that are benchmarked to integrated indexes such as MSCI ACWI IMI capture the full opportunity set within equities. Dedicated allocations that separate developed and emerging markets provide flexibility in active views to either market, but introduce market-timing risk.

Due to the convergence of return and risk profiles between developed and emerging markets, together with the dispersion between countries within emerging economies, some institutional investors are reconfiguring mandates to take more active views on individual countries, recognizing that most dispersion between emerging market stock returns is due to country factors. For example, some investors have turned to targeted mandates to express a view on a bloc of countries, or to manage specific sources of risk.

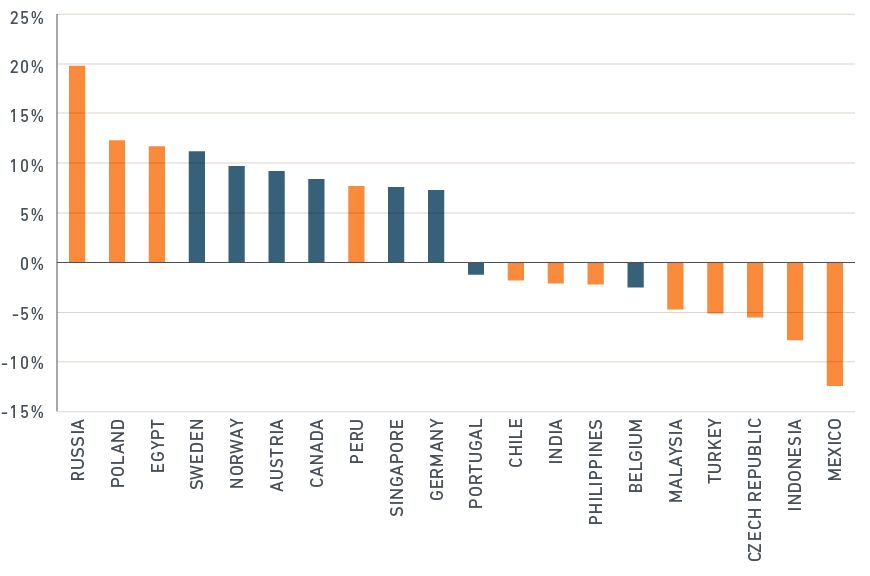

Though many emerging market equities dipped in the immediate aftermath of the U.S. election, others fared well and the group as a whole has rebounded since Jan. 1. Russian stocks have climbed 20% since Nov. 8. Polish and Egyptian equities are up about 12% over the same period. Mexican stocks, on the other hand, have fallen 12%.

Differences in the performance of emerging-market equities since the US election

POST-U.S. ELECTION PERFORMANCE

Cumulative performance from Nov. 8, 2016 to Jan. 31, 2017 based on MSCI indexes. Returns are Gross, and in USD.

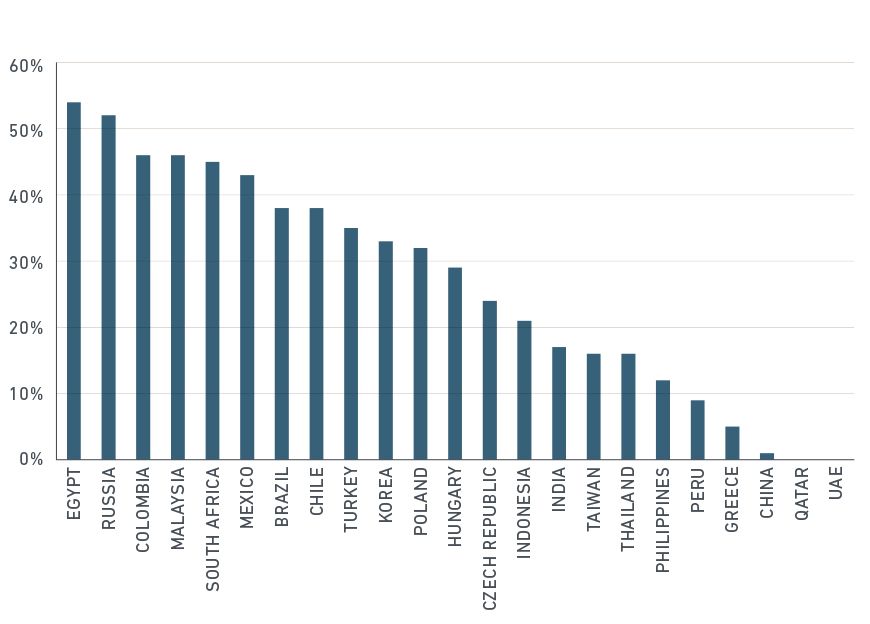

To be sure, targeted mandates can magnify sources of risk. Emerging-market equities remain riskier than their developed market counterparts by one important measure: currency risk (below chart). In many countries, over 40% of market volatility ties solely to currency effects. Hedge strategies may mitigate – and mask – this volatility.

Currency risk was on display when central banks in Brazil and India cut rates, as well as when India implemented a surprise demonetization program. Stocks in Russia benefited from a rise in its Purchasing Managers' Index and appreciation of the ruble. Likewise, Egyptian equities recovered from a decision in November by the country's central bank to let the pound float.

The policies of the new U.S. administration may impact some emerging-market currencies more than others. For example, the falloff in Mexican stocks reflects fears of protectionism. But exposure to the peso has pummeled dollar-based investors much more.

Currency risk can be as significant as equity risk in single country investing

CURRENCY SHARE OF TOTAL VOLATILITY

Volatility contribution based on EMM1 as of Jan. 31, 2017.

The divergence in results across emerging markets suggests that as emerging markets mature and both country and currency effects widen, institutional investors can implement more active mandates to take advantage of the differences. Provided, that is, they are willing to incur the risk.

The author thanks Anil Rao for his contributions to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.