- The aggregate volume of Chinese nonperforming loans (NPL) and related asset-backed securities (ABS) has grown rapidly in recent years.

- Phase one of the U.S.-China trade deal opened the opportunity for U.S. managers to invest in this asset class.

- Examining the performance of Chinese NPL ABS could help address the challenges that investors face of modeling key inputs like recovery rates and liquidation timing.

Chinese NPL asset class has rapidly expanded

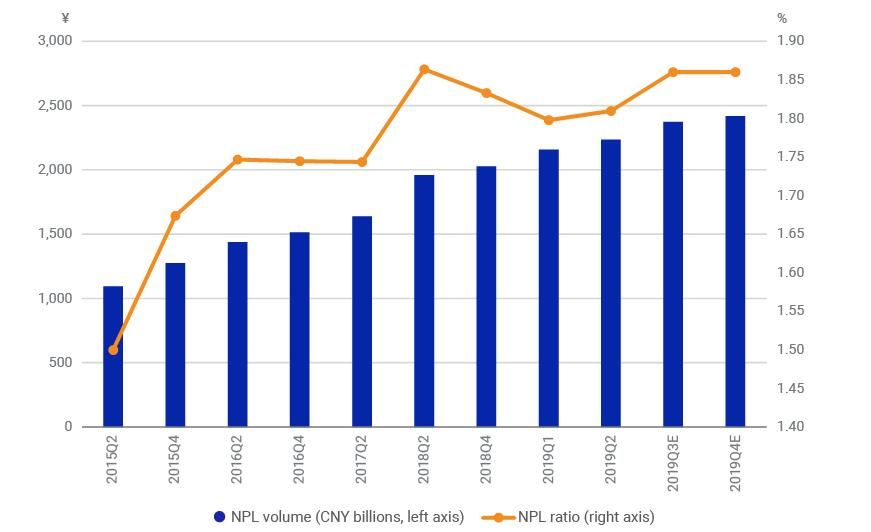

According to data from the International Monetary Fund and People's Bank of China, total domestic loans outstanding in China's depositary institutions was roughly CNY 129 trillion, as of December 2019. The China Banking and Insurance Regulatory Commission reported the NPL ratio for these loans was 1.9% in the third quarter of 2019 (though many estimates are much higher) — which translates to about CNY 2.4 trillion of NPL outstanding.3 Only a small number of these assets are securitized as NPL ABS, as we discuss below.

NPL in China's depository institutions

Volumes for the third and fourth quarters of 2019 are estimated from NPL ratio and outstanding loan volume. Source: International Monetary Fund, People's Bank of China, China Banking and Insurance Regulatory Commission

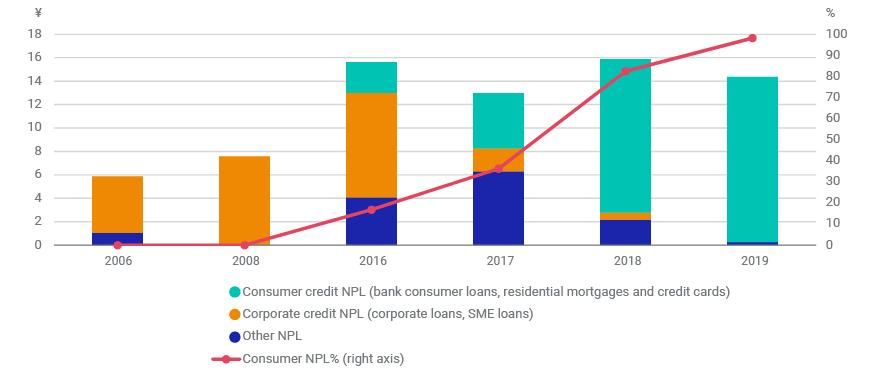

Total issuance of NPL ABS since 2006 is only CNY 72.2 billion, or less than 1% of the total Chinese ABS issuance of CNY 8 trillion. The exhibit below shows that consumer loans (bank consumer loans, residential mortgages and credit card loans, etc.) accounted for only 17% of the total NPL ABS issuance in 2016, but made up 98% of the total issuance in 2019.

Consumer loans' dominance in recently issued Chinese NPL ABS

Source: MSCI, CNABS

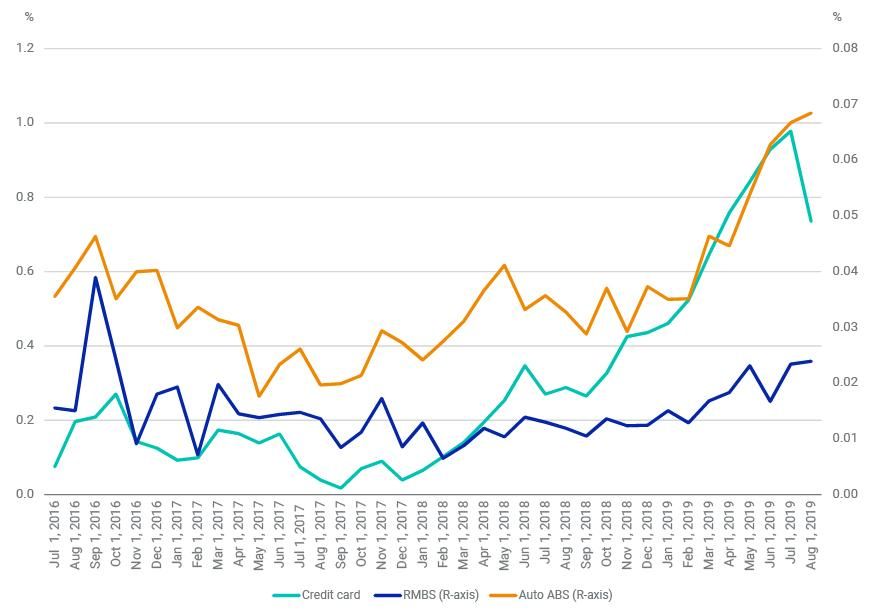

The exhibit below shows a rapid increase in overall consumer-loan delinquency, which may have helped fuel this trend in the issuance of NPL ABS. As we discussed in a previous blog post, the default rate for pre-2019-vintage auto loans have increased more than 100% from September 2018 to August 2019. For similar vintages, the default rate for loans backing credit-card ABS has increased 700% — more than eight times the average default rate between 2016 and 2017. Even for residential mortgages with the same vintages, which is often considered the safest consumer loan, the default rate was twice as high as the historical average through Dec. 31, 2018.

Chinese consumer-loan defaults generally rose since 2018

Source: MSCI, CNABS

As bad loans increased, in late 2019, China's regulatory agencies started a third round of their pilot program for NPL ABS. Twenty-two new institutions — including the four largest state-owned asset management companies, and multiple urban, commercial and rural banks — are now on the list of qualified NPL ABS issuers. The State Council has granted a quota of CNY 100 billion to the overall origination volume — twice the amount allocated to the previous two pilot programs.

Historical recovery rates and liquidation timing

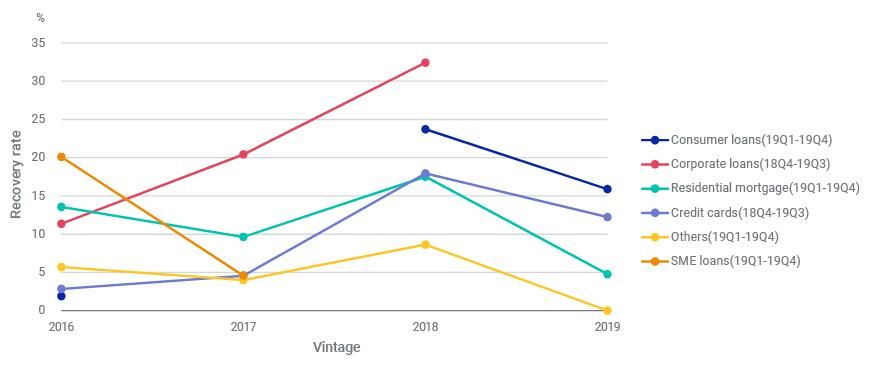

The economic value of NPLs is driven by their recovery rates and the liquidation time. The exhibit below shows the the most recent year's recovery rates for various NPL ABS collateral pools, with vintages between 2016 and 2019. We find the ranges are very wide: The 2019 recovery rate for 2018 corporate loans was 32.4%, while it was 4.8% for 2019 residential mortgages.

2019 recovery rate of NPL ABS by vintage

2019 recovery rates of various NPL-ABS collateral pools for 2016-2019 vintages. Source: MSCI, CNABS

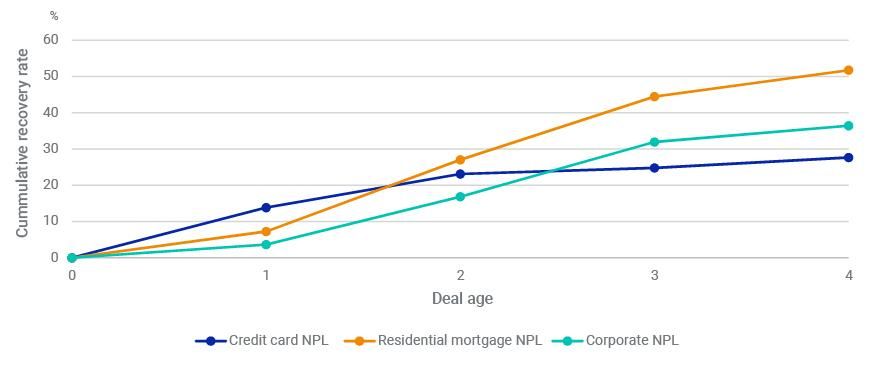

Recovery rates and liquidation times are driven by many factors: collateral value and type, leverage ratios, property-market momentum, servicer quality and the macroeconomic and policy environment. The exhibit below shows our model's analysis of the baseline cumulative recovery rates for three sample NPL ABS asset types (credit card loans, residential mortgages and corporate loans), based on MSCI's models for Chinese ABS. For loans in NPL card ABS, the model total recovery plateaus within two to three years and converges to around 25%. For NPL RMBS, the model total recovery has longer timelines and converges to around 50% — which assumes no big drop in overall house prices. The model overall recovery rate of loans in NPL corporate ABS converges to about 35%. However, this would depend on the mix of collateral, which varies considerably across deals.

Model's baseline cumulative recovery rates for NPLs

Source: MSCI Chinese ABS Model

The phase-one U.S.-China trade agreement broadened opportunity to invest in Chinese NPL, and investors may be able to utilize models to analyze collateral performance and potential recovery outcomes.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1“Economic And Trade Agreement Between The Government Of The United States Of America And The Government Of The People’s Republic Of China Text.” Office of the U.S. Trade Representative, Jan. 15, 2020.2Chen, J. and Yang, Y. 2020. “MSCI China Non-Performing Loan ABS Collateral Model.” MSCI Model Insight. (Client access only.)3“China NPL Ratio.” CEIC.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.