Using Systematic Equity Strategies to Build Better Portfolios

Blog post

April 23, 2015

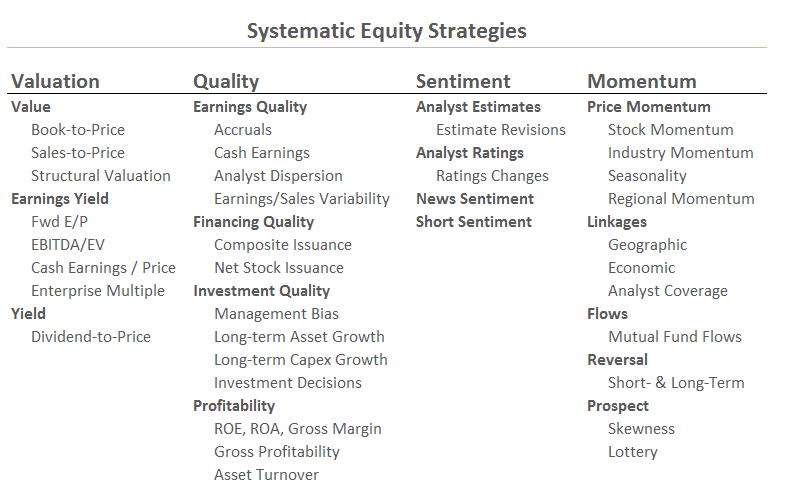

Systematic Equity Strategies, when represented as factors in risk models, allow investment managers to better monitor the sources of risk and return in equity portfolios. We believe that they also improve forecast accuracy and help construction of portfolios that tilt towards (or away from) these strategies, which are rules-based or computer-based implementations.

There are two main reasons for incorporating SES factors into a risk forecasting model:

- The majority of SES factors are viewed by the market as predictors of future cash flows of companies. As a result, they are drivers of expected stock returns. In practice, these factors have also been viewed as important sources of abnormal returns. As drivers of stock returns, SES factors are also drivers of volatilities and correlations among stocks. SES factors in risk models allow investment managers to measure this volatility and its correlation effect.

- Some Systematic Equity Strategies may lead to crowding risk as large pools of capital flow into these strategies. Investors using risk models with SES factors are able to measure and monitor their exposures to these crowded strategies and make more informed risk and return tradeoff decisions.

Crowding in a strategy may result in improved market efficiency, such as faster price discovery in the short-term. While crowding reduces effectiveness of the strategy in predicting stock returns, it is still an important source of risk during the price discovery period due to frictions such as shorting constraints and transactions costs.

There is an additional dimension of crowding risk that is valid for a wide range of "unanchored" strategies especially when the investor pursuing the strategy does not know how much capital is pursuing it. Crowding in these strategies may result in prices moving towards and then further away from fundamental prices. When there is enough of a deviation from fundamental prices, other managers (following valuation strategies) may step in to benefit from the investment opportunity. In this case, crowding in the strategy introduces additional volatility during the price discovery process.

We believe that incorporating SES factors in risk models can do the following:

- Improve portfolio risk forecasts, especially for portfolio managers who purposefully take largebets on SES Factors

- Help investors make better trade‐off decisions between risk and returns of these strategies

- Provide a framework for analyzing potentially crowded investment strategies

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.