What do Factors Tell us About Regime Change in U.S. Stocks Following the Election?

Blog post

December 2, 2016

Pro-cyclical factors are in, defensive factors are out. That, in a nutshell, describes how the U.S. equity market has responded to the presidential election.

To better understand the environment that has emerged since Nov. 8, we compared the performance of six MSCI USA Factor Indexes¹ with the MSCI USA Index, which measures the performance of the large- and mid-cap segments of the U.S. market.

President-elect Donald Trump's statements favor higher infrastructure and defense spending, along with corporate tax reform and lighter regulation. The market's assessment is revealed in changes in the performances of the factor indexes before and after the election, as seen in the chart below.

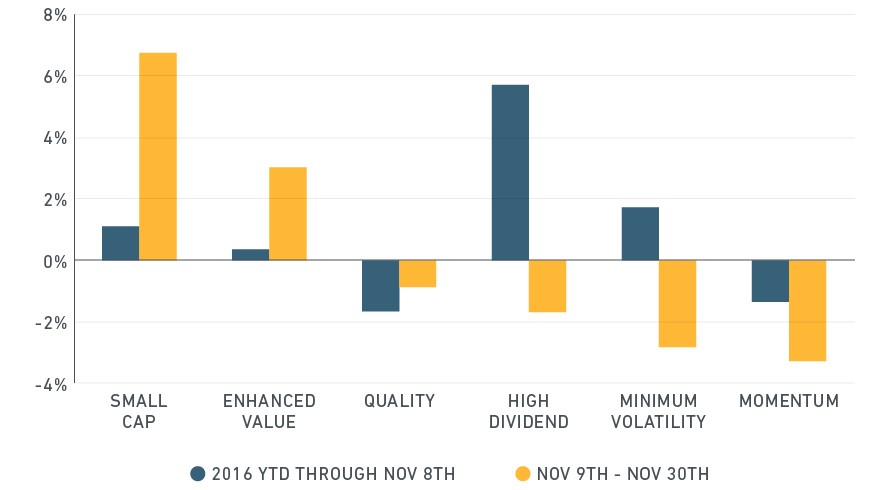

Since the election, expectations of economic growth have propelled factor indexes such as small cap and enhanced value, which have outperformed the MSCI USA Index, while quality, dividend yield, minimum volatility and momentum indexes have underperformed. In contrast, prior to the election, dividend yield, minimum volatility and small cap were the best performers.

Pro-cyclical factors up, defensives down

Source: MSCI Research. The chart shows excess returns of MSCI's USA Factor Indexes vs. MSCI's USA Index, which is weighted by market capitalization of constituents.

The performance of each of the factor indexes suggests that investors are pricing in expectations about the incoming administration's policies. The outperformance of the small cap index presumes that tax cuts may benefit companies that generate most of their revenue in the U.S., compared with multinationals, which may earn the bulk of their revenues overseas.

Similarly, a tilt toward protectionism would hit large-cap companies harder than their smaller counterparts. A boost in infrastructure spending together with an uptick in interest rates diminishes the appeal of high dividend-paying stocks, as evidenced by the underperformance of the corresponding factor index.

Going for granularity

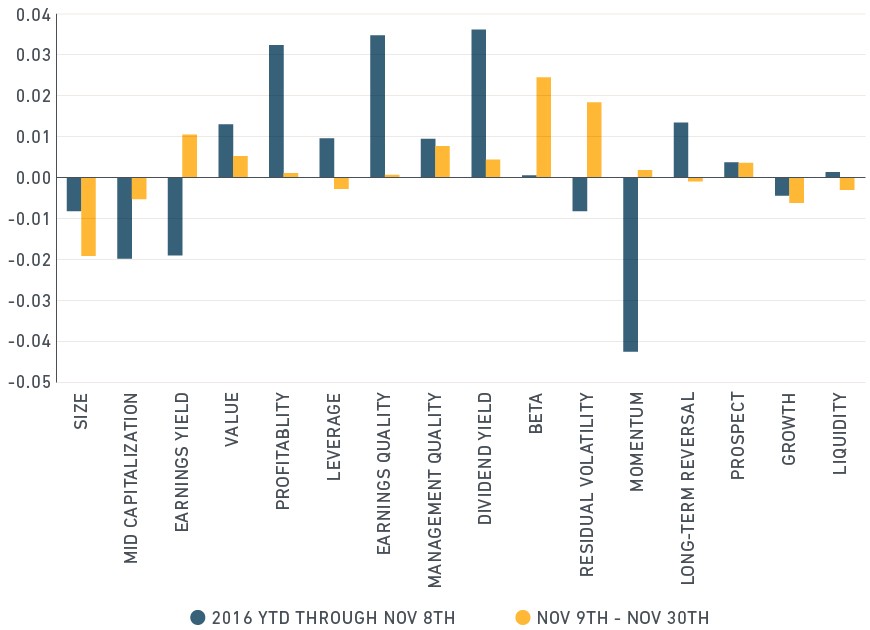

The reaction to the election also shows up in the returns of style factors,² as described in the MSCI Barra U.S. Total Market Equity Model. The outperformance of earnings yield, beta and volatility and underperformance of size and mid-cap factors since the election (below chart) mirrors the performance of the MSCI Factor Indexes, suggesting that the factor indexes are reasonable proxies for the "purer" style factors. The underperformance of the growth and liquidity factors shows investors moving toward riskier investments.

Before and after: Factor returns suggest the U.S. market has entered a new regime

Source: MSCI Research. This figure displays returns of MSCI BARRA U.S. Total Market Equity Model style factors.

Underperformance since the election of the profitability factor, a proxy for quality, suggests that investors have adopted a risk-on outlook and are eschewing quality stocks.

That's not to suggest that the election alone is the only factor that is driving changes in systemic risk. Even before the election, markets had started pricing in a potential interest rate hike and reflected investor sentiment on yield strategies. The recent underperformance of the leverage factor seems to attest to the same concern. If anything, the election may have accelerated the trend.

The performance of the management quality factor, which favors companies that return capital to stockholders via dividends and share repurchases, may reflect the effect of the proposed one-time tax holiday from repatriation of cash held overseas. These firms can deploy the new funds for increased dividends and/or share repurchases, which makes them more attractive to investors.

There are limits to what investors can infer from roughly two weeks of trading since the election. Still, factors tell us something about what investors are thinking amid a period of change in financial markets.

¹ These are rules-based indexes that capture the returns of systematic factors that have historically earned a persistent premium over long periods of time.

² Style factors tend to be purer than factor indexes, which, by definition, must be investable. Style factors are long-short, dollar-neutral and have unit exposure to the target style and zero exposure to all other styles, industries and U.S. country factors.

The author thanks Leon Roisenberg for his contributions to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.