What market volatility has meant for factors

Blog post

February 13, 2019

We recently examined how factors have performed in different interest rate regimes. In this post, we examine factor performance during periods of high and low volatility.

A little more than one year ago (Feb. 9, 2018), the CBOE Volatility Index (VIX) surged to an intra-day peak of 41.06 from a level of 12.5 earlier that month. The VIX had not reached a level that high since August 2015. In the face of market volatility that continued throughout 2018, we saw rapidly shifting factor rotation, as well as a preference for historically defensive factors in the latter half of the year. As investors continue to focus on factor investing in periods of heightened volatility, we ask how volatility has affected factor performance.

We found that, over the last 28 years, lower volatility favored historically pro-cyclical factors, such as momentum, size and value, while historically defensive factors, such as quality, volatility and yield outperformed during periods of high volatility.

And momentum, generally considered a pro-cyclical factor, actually outperformed in both regimes – raising questions about its "pro-cyclical" designation.

How have factors performed during periods of low and high volatility?

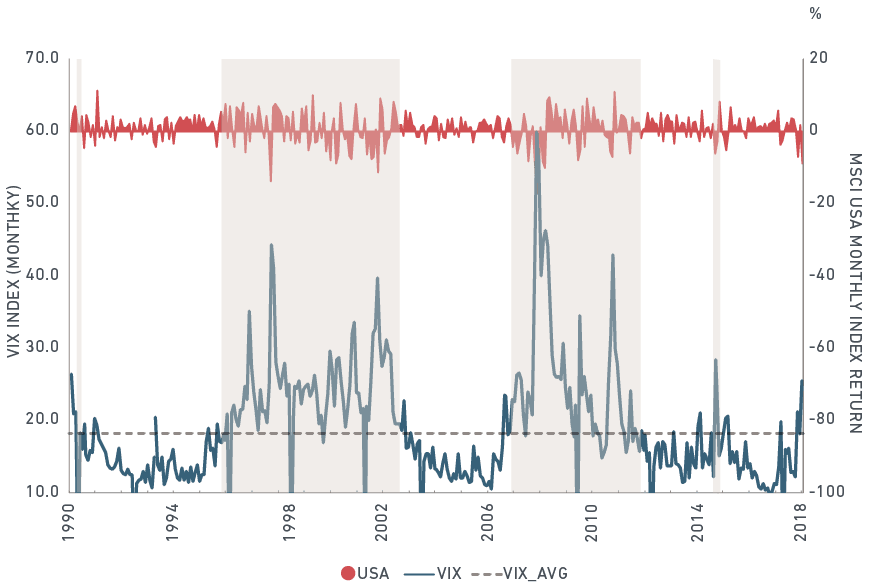

We examined the VIX and observed several episodic shifts between high and low volatility. The dotted line in the exhibit below represents the average VIX level for 336 monthly observations from December 1990 to December 2018. Over this 28-year period, we saw approximately five volatility regimes, including a high volatility environment during the run-up to and collapse of the internet bubble (December 1996 to September 2003) and another during the credit crisis that triggered the global financial crisis (November 2007 to May 2012). The chart also shows periods that where the VIX rose sharply, this coincided with more pronounced positive and negative market moves in the U.S., using the MSCI USA Index as a proxy.

Five volatility regimes over the last three decades

Source: Data based on performance of the MSCI USA Index and the VIX from Dec. 31,1990 to Dec. 31,2018

To understand how factors performed in the two regime types i.e., the internet bubble and the credit crisis, we grouped all monthly observations into either high or low volatility and calculated risk and return statistics for the MSCI USA Factor indexes.1

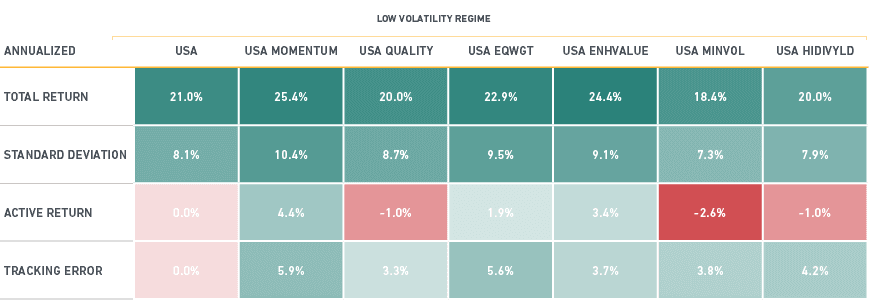

The download on low volatility

The low-volatility regimes include 198 monthly observations which cover approximately 16 ½ of the 28 years. Absolute total return for each of the MSCI USA Factor indexes was above 20% except for the MSCI USA Minimum Volatility Index. Active return differences provide some insights. During periods when the VIX was below average, thus implying lower expected market volatility, historically pro-cyclical factors such as momentum, size and value outperformed the market. Historically, defensive factors, such as quality, yield and volatility underperformed. We saw the largest level of underperformance from the MSCI USA Minimum Volatility Index, which underperformed the MSCI USA Index by 2.6% with about 10% lower standard deviation.

Source: MSCI data from Dec. 31,1990 to Dec. 31,2018

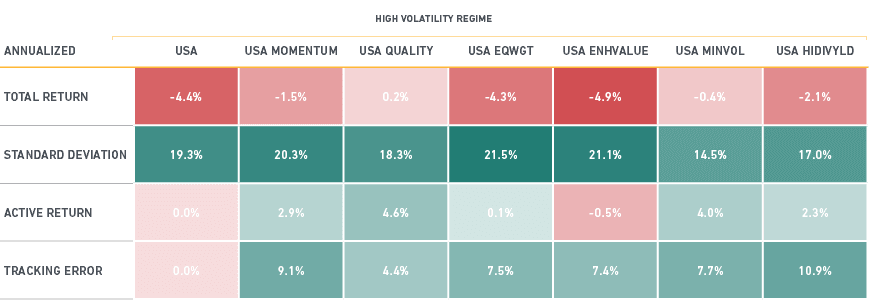

The high volatility regimes include 138 monthly observations which cover the other approximately 11 ½ years of the period under examination. Absolute total return for each of the indexes was either low or negative. When we again look to active return we found that, during periods when the VIX was above-average, implying higher expected market volatility, historically defensive factors, such as quality, volatility and yield outperformed the market, while historically cyclical factors, such as size and value underperformed.

The upshot on high volatility

Source: MSCI data from Dec. 31,1990 to Dec. 31,2018

One notable finding was that the momentum factor outperformed the market in both low and high volatility regimes, suggesting that it may not always behave as a pro-cyclical factor. We also observed that under the high volatility regime the tracking error for the MSCI USA Minimum Volatility Index and MSCI USA High Dividend Yield Index increased by 3.9% and 6.7% respectively. This tracking error leads to our next question:

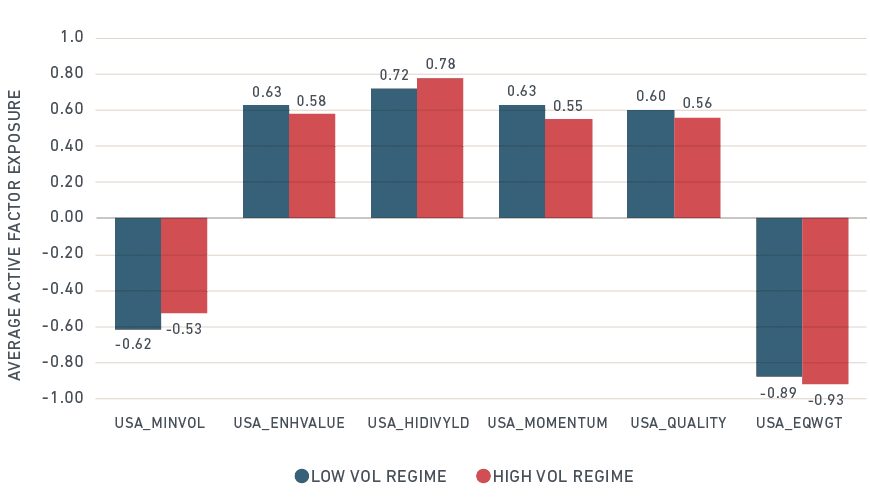

Have factor exposures within factor indexes shifted with volatility regimes?

Starting from the target MSCI FaCS exposures for each of the MSCI USA Factor Indexes in the chart below, we examined the magnitude of the exposure achieved under each volatility regime. In general, the high volatility regimes resulted in slightly lower exposure for each of the target factors except for size and yield. Nonetheless, the magnitude of the exposure achieved for every factor was ± 0.20 and under either type of regime provided meaningful exposure to the target factor.2

Exposure was varied but meaningful across volatility regimes

Source: Average Active Exposure for MSCI USA Factor Indexes from Dec. 31, 1998 to Dec. 31, 2018

The analysis we conducted over the 28-year observation period highlighted the risk/return differences of factors in low and high volatility regimes. Generally speaking, pro-cyclical factors outperformed the market in a low volatility regime, while defensive factors outperformed during periods of high volatility. The momentum factor was an exception, as it outperformed during both regimes. As investors evaluate factor allocation decisions they may find it important to consider volatility regimes in addition to interest rate and other macro regime changes.

The author thanks Raman Aylur Subramanian and Raina Oberoi for contributing to this blog

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Analysis was based on the MSCI USA Momentum Index, MSCI USA Quality Index, MSCI Equal Weighted Index, MSCI Enhanced Value Index, MSCI USA Minimum Volatility Index and the MSCI USA High Dividend Yield Index.2Bonne, G., L. Roisenberg, R. Subramanian and D. Melas. (2018). “Introducing MSCI FaCS: A New Factor Classification Standard for Equity Portfolios” MSCI Research Insight.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.