Which Factors Are More Time-Sensitive?

Blog post

September 28, 2016

Hedge funds and other investors who manage portfolios that rebalance frequently face a challenge when it comes to the use of factors for trading, hedging and risk monitoring: Which factors tend to break down over time?

To answer the question, we examined a universe of global stocks over the 24 years ended in May 2016. From that universe, we built model portfolios for each of 14 Systematic Equity Strategy (SES) factors that we implemented with delays ranging from one day to one month. MSCI's SES factors use rules-based algorithms to help investors monitor factor performance in their own portfolios.

By design, the exposures of eight of the factors (which are included in the Barra Global Equity Model for Long-Term Investors) are relatively stable, with average month-to-month correlations ranging from 0.98 for investment quality to 0.93 for momentum. Six additional SES factors that are included in the latest Barra Global Total Market Trading Equity Model showed less stability, with correlations that ranged between 0.83 for short interest (short-selling as a percentage of available shares for borrowing) and -0.12 for seasonality (how stocks perform similarly around the same time each year).

The other factors are short-term reversal (the expectation that performance will revert), industry momentum (how a stock relates to momentum trends in an industry), news sentiment (investor reaction to breaking news) and analyst sentiment (changes in earnings forecasts).

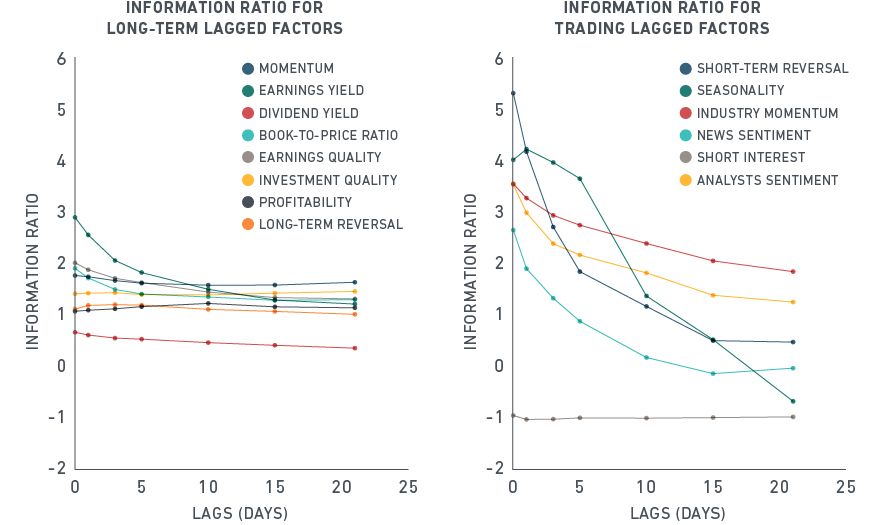

Measuring short-term signals

We examined how quickly information ratios for each of the 14 SES factors decayed. As the charts below show, the performance of some factors decayed faster than others. Note the stability of the factors at left. By comparison, the performance of factors in the chart at right decayed more quickly.

Measuring the time-sensitivity of 14 SES factors

Source: MSCI Research. The information ratio for each value of the lag is computed from the returns of the factor portfolios constructed at t but invested at t+lag, over a period that ranged from one to 21 days.

To put it simply, the factor information from the stable factors could be implemented following a substantial delay with only minor effects on the resulting information ratios. Most of the factors at right, however, depended on rapid implementation to provide significant positive information ratios.

There are exceptions. Among stable factors, the yield factors showed substantial decay over the first week. That variability highlights the complexity of these factors, with the components of each contributing to information ratios at different horizons, i.e., over long and short terms. Among the factors at right, note the performance of short interest, which remained stable across the horizon. The high-frequency component of exposure did not seem to contribute to the factor's information ratio. Again, that suggests complexity.

The analysis may benefit institutional investors who rebalance frequently and help them to think anew about implementation of SES factors in their portfolios. That can deepen insights into the factors that fuel performance.

The author thanks Andrei Morozov for his contribution to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.