Is Europe more than the sum of its parts?

Blog post

October 8, 2019

- Institutional investors in European equities typically have a choice between investing in country or pan-European regional index-based portfolios.

- Not constrained by a fixed number of constituents, the regional approach we tested captured a wider opportunity set, with smaller but still investable stocks.

- Over the past 18 years, the regional approach more efficiently captured the full European risk premium, posting an extra 50 basis points (bps) per year, with the same volatility.

What's my opportunity (set)?

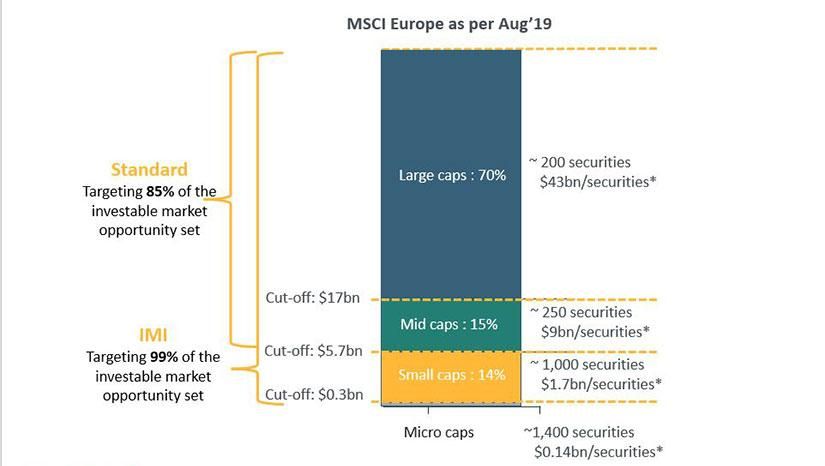

Local-market indexes, most of which have a fixed number of stocks, have tended to focus on companies with the largest market capitalizations in each country, leaving aside smaller companies that were nonetheless liquid and investable. Thus, the average size of stocks from individual markets can vary substantially. At the end of last year, the free-float-adjusted market cap of the five smallest stocks in the German or French local index averaged above USD 11 billion — well above the nearly USD 2 billion average in Italy and Spain.

Consequently, a hypothetical portfolio of funds based on individual local-country indexes did not provide exposure to the full European-equity opportunity set. Such a portfolio represented only 83% of the market cap of a regional index like the MSCI Europe Investable Market Index (IMI), which included liquid, smaller-market-cap stocks alongside large- and mid-cap stocks. In contrast, the MSCI Europe IMI aims to capture 99% of the overall European listed equity market (see exhibit below). The gap was even larger when considering the number of stocks covered (1,438 vs. 533), which means that many smaller, growing companies were omitted from the local-country indexes.

MSCI Europe IMI opportunity set

As of Aug. 30, 2019.

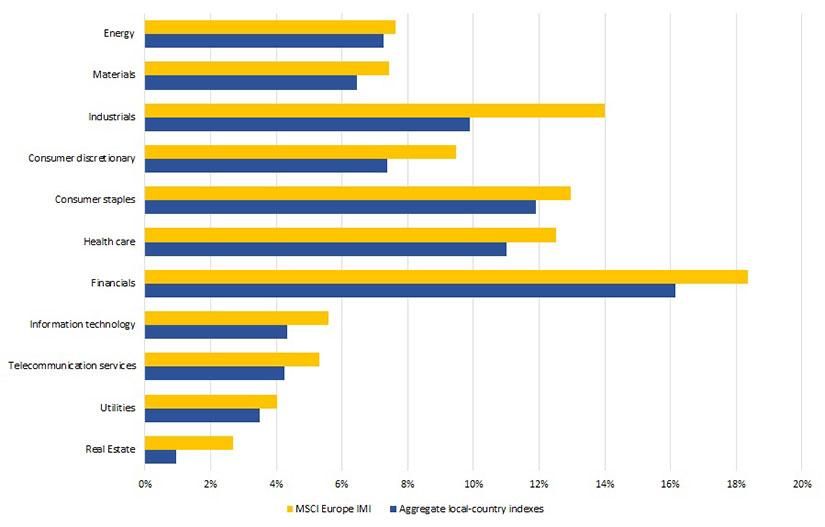

Additionally, our hypothetical regional fund included more of the opportunity set in each sector — industrials, consumer discretionary, financial and real estate, in particular.

Regional approach provided greater sector exposure

Sector exposure as a percentage of MSCI Europe IMI as of Dec. 31, 2018. Data sources: DataStream, MSCI

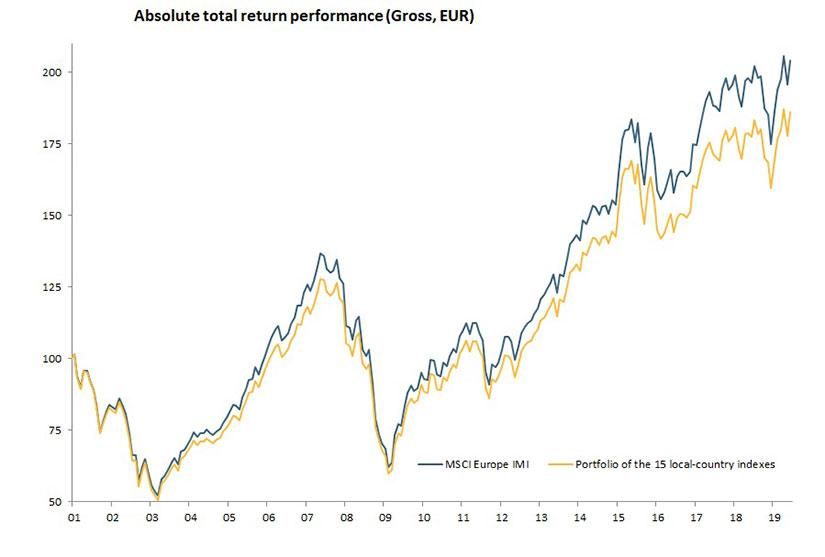

Absolute and relative performance

We simulated the gross total return of a hypothetical portfolio of funds based on 15 local-country indexes, from the start of January 2001 through the end of June 2019, matching the countries and their weights in the MSCI Europe IMI. Over this period, the collection based on local indexes returned 3.4% per year with a volatility of 15.1%, while the MSCI Europe IMI more efficiently captured the full European risk premium, posting an extra 50 bps per year (with a 3.9% annual return). Significantly, the regional approach better captured the low-size factor premium, while providing the same level of volatility.

Regional vs. local-country approach performance

Performance from Jan. 1, 2001, through June 30, 2019. Data sources: DataStream, MSCI

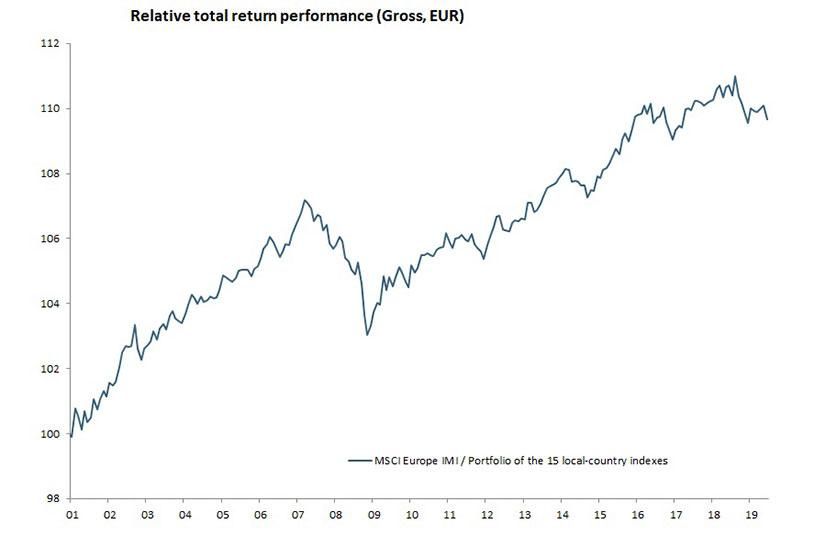

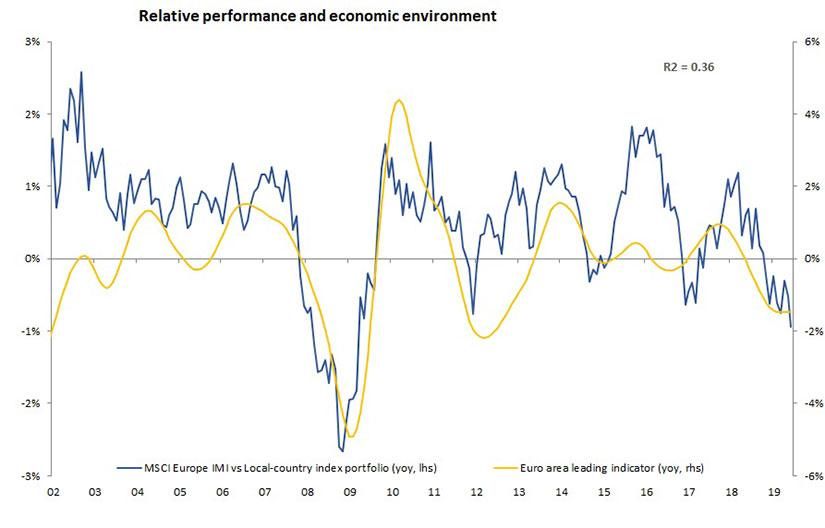

We should note that, though a regional approach outperformed over the full period, there were occurrences of underperformance over some one-year rolling periods, the largest one being around -2.5% in 2008 — i.e., during the global financial crisis. As seen in the exhibit below, underperforming periods happened during times of economic slowdown in Europe, as proxied by the euro-area-wide leading indicator.

Regional approach underperformed during economic slowdowns

One-year rolling periods from Jan. 1, 2002, through June 30, 1019. Data sources: DataStream, MSCI

While investors' approaches to European equities depend on a variety of factors, and past performance is not indicative of future results, investing in a fund based on a regional index, such as the MSCI Europe IMI, provided greater diversification and outperformance versus a portfolio of individual country funds during our study period.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1We looked at the 15 European countries included in the MSCI Europe IMI: the U.K., France, Germany, Switzerland, the Netherlands, Sweden, Spain, Italy, Denmark, Belgium, Finland, Norway, Ireland, Austria and Portugal.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.