Evolution of Fund Naming Calls for Deeper, Data-Driven Sustainability Insights

With less than three months to go until the European Securities and Markets Authority's (ESMA) Guidelines on funds' names using ESG- or sustainability-related terms takes effect on May 21, 2025, fund rebranding is well underway.1 The latest data reveals notable trends in fund-naming conventions for Article 8 and 9 funds, as defined under the Sustainable Finance Disclosure Regulation (SFDR).2

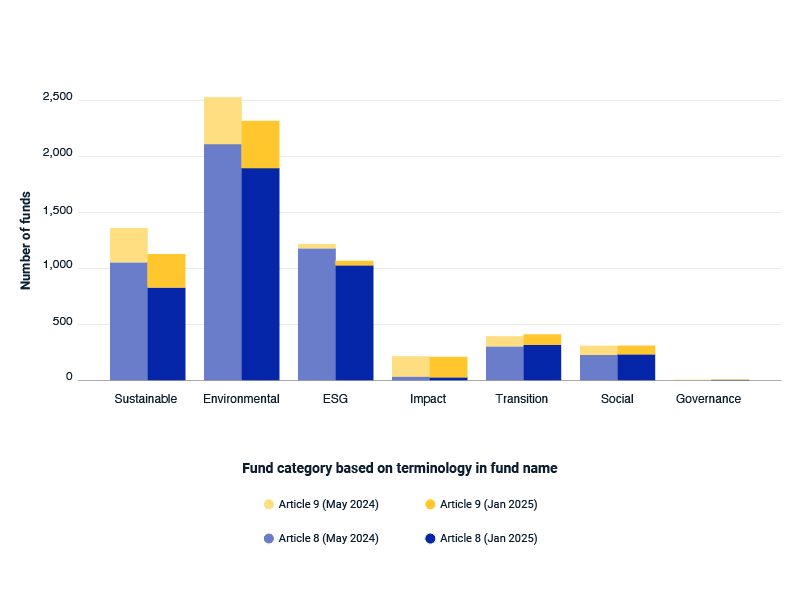

Since ESMA's Guidelines were published in May 2024, the number of funds with sustainability-related names has declined approximately 20%. Such funds are subject to EU Paris-aligned Benchmarks (PAB) exclusions and required to "meaningfully invest in sustainable investments (SI)."3 This activity has been primarily driven by the renaming of Article 8 products, indicating that ESMA's clarification of "meaningfully investing in SI" as being at least 50% of a fund's assets is challenging for some Article 8 strategies, as highlighted in our recent analysis.4 Environmental- and ESG-related fund names, which are subject to PAB criteria but not the 50% SI threshold, declined by 10% and 12%, respectively. In contrast, transition-related fund names, which are subject to EU Climate Transition Benchmarks exclusions that allow fossil-fuel based investments, grew by 4%.5

Fund-renaming activity and the launch of transition-related products are likely to accelerate as ESMA's deadline for compliance with the Guidelines approaches. Fund names related to social-, governance- and impact-related terms remained relatively stable, with renaming activity mostly occurring in Article 8 products.6 The impact of ESMA's Guidelines also extends beyond Europe. For example, our data shows that EU-domiciled funds sold in Asia replaced "sustainability" with "transition" in fund names.

As funds continue to drop ESG- and sustainability-related terms from their names, transparent fund-level insights are likely to play a growing role in communicating the underlying sustainability characteristics of investment products. This change is especially relevant in the wealth-management industry, where studies suggest retail fund flows are disproportionately influenced by fund names,7 underscoring the importance of data-driven insights to differentiate funds in an evolving market.

Fund-renaming activity is underway

Data as of Jan. 31, 2025. ESG-named funds are a subset of the environmental category. Number of unique SFDR Article 8 and 9 funds with identifiable keywords related to ESMA guidance classification: 4,376. Source: MSCI ESG Research

Subscribe todayto have insights delivered to your inbox.

The Fund-Name Challenge: Matching Investor Needs and Supervisory Expectations

To adhere to ESMA’s fund-naming guidelines, sustainability-minded fund managers may have to choose between fund name and preferred investment strategy. Our analysis shows that almost 11% of MSCI ACWI IMI constituents by weight could become ineligible investments for such funds.

Identity Check — ESMA’s New Name Guidelines for ESG and Sustainability-Related Funds

ESMA’s new fund-naming guidelines could impact one in three SFDR Article 8 and 9 funds, necessitating name changes or adherence to new investment thresholds and fossil-fuel exclusions for compliance.

Stop! In The Name Of Sustainability Funds (i.e., ESMA’s New Guidelines)

Maybe a rose by any other name would smell as sweet, but that’s not going to fly for sustainability funds in the EU. On this episode we break down ESMA’s latest fund guidelines and discuss their place in a regulatory landscape with all kinds of moving pieces.

1 “Final Report – Guidelines on funds’ names using ESG or sustainability-related terms,” ESMA, May 14, 2024. For new funds released after Nov. 21, 2024, the rules already apply. Funds existing prior to this date need to be compliant by May 21, 2025.2 Based on keywords identified in fund names, including variant forms of in-scope words across European languages.3 Article 12(1) of Commission Delegated Regulation (EU) 2020/1818 of 17 July 2020 on minimum standards for EU Climate Transition Benchmarks and EU Paris-aligned Benchmarks.4 “ESMA puts forward Q&As on the application of the Guidelines on funds’ names,” ESMA, Dec. 13, 2024.5 Article 12(1) (a) – (c) of Commission Delegated Regulation (EU) 2020/1818 of 17 July 2020 on minimum standards for EU Climate Transition Benchmarks and EU Paris-aligned Benchmarks.6 Social- and governance-related fund names are subject to CTB exclusion criteria. Impact-related fund names are subject to PAB exclusion criteria and, jointly with transition-related funds, must fulfil additional conditions linked to clear and measurable progress/impact. All funds with ESG- or sustainability-related terms must invest 80% of assets in line with the binding elements of their investment strategy (either environmental or social characteristics, or sustainable-investment objectives).7 Kevin Birk, Stefan Jacob and Marco Wilkens, “What attracts sustainable fund flows? Prospectus versus ratings,” Journal of Asset Management, June 2024.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.