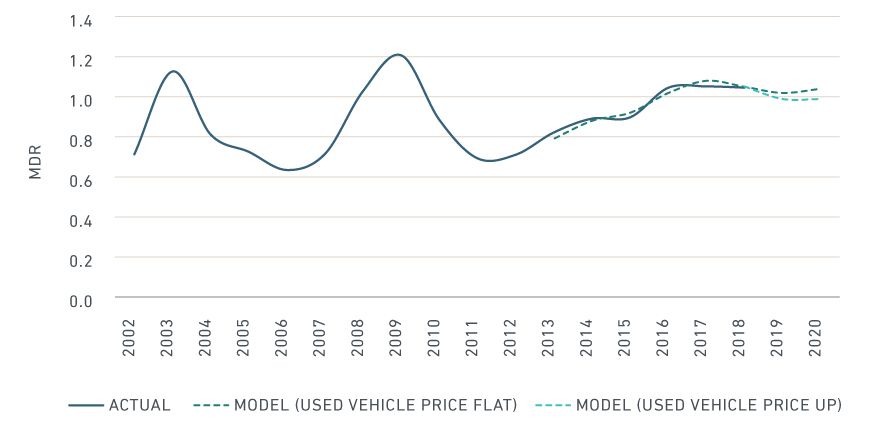

Investors and the media have lately turned their attention to credit risk in U.S. subprime automotive lending — concerns that increased during the recent market volatility.1 Based on MSCI's new U.S. auto-loan model, under current conditions, we think monthly default rates (MDR) are likely to stay flat in the near term and potentially even decrease if used-vehicle prices rise.

MONTHLY DEFAULT RATE IN US SUBPRIME AUTO ABS — HISTORICAL MDR AND MODEL PROJECTIONS USING DIFFERENT ASSUMPTIONS

Source: MSCI, INTEX

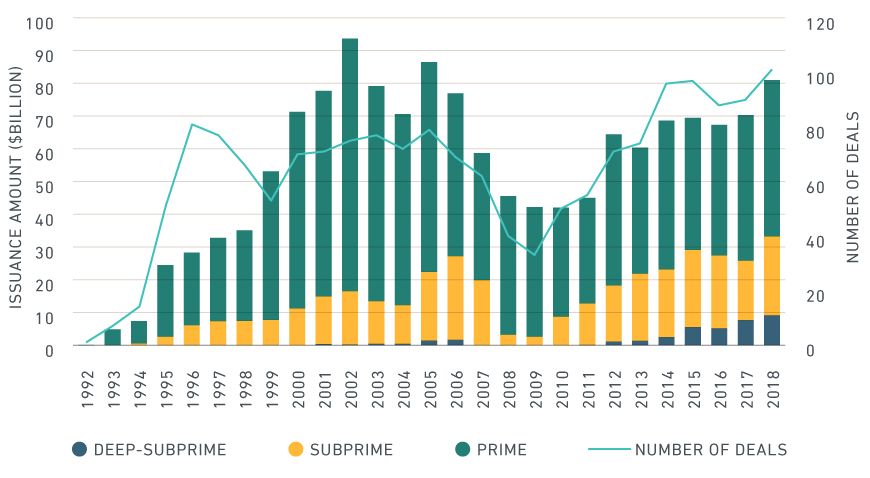

Since the global financial crisis, subprime consumer and mortgage lending and securitization have been subject to greatly increased regulation, which has decreased activity in these areas — with some notable exceptions: Subprime and deep-subprime auto-loan issuance and securitization have bounced back and lately exceeded pre-crisis levels.2 During 2018, issuance of subprime auto asset-backed securities (ABS) reached about USD 33 billion and represented roughly 41% of total U.S. auto ABS issuance (vs. USD 27 billion and 35% of total issuance in 2006).

INCREASED ISSUANCE OF LOWER-CREDIT-QUALITY AUTO-LOAN ABS SINCE THE CRISIS

Source: MSCI, INTEX

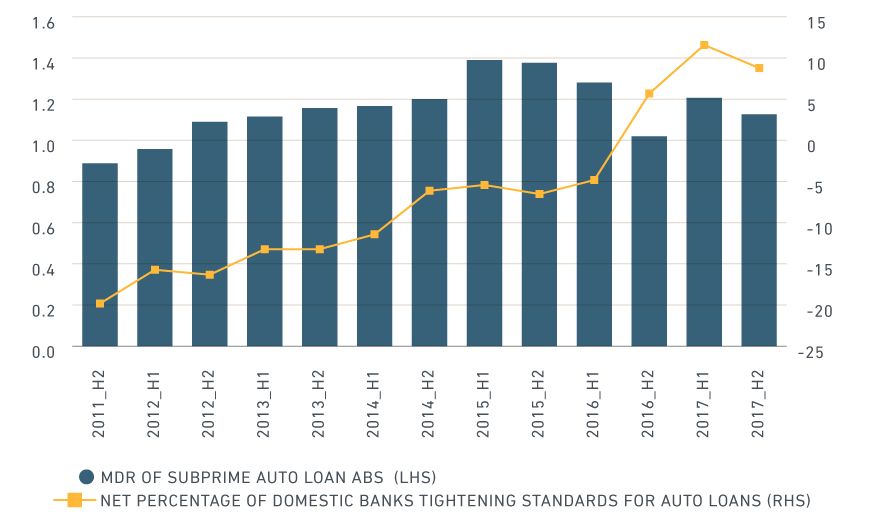

Overall default rates for subprime auto ABS climbed between 2011 and 2018. The 2015 vintage's default rates approached the peak levels of the financial crisis. Loosened underwriting standards were likely a key contributor to this drop in performance. Despite the increased issuance of deep-subprime auto loans in recent years, banks' auto-loan credit standards tightened in 2016, according to a survey by the Federal Reserve Bank of St. Louis.3 And historically, changes in banks' underwriting standards have appeared to be a good indicator of credit quality of auto-loan ABS (issued during the period) and to drive the default rates of subprime auto-loan ABS, as we can see in the exhibit below.

CREDIT STANDARDS AND DEFAULT TRENDS IN US AUTO LENDING

The MDR represents the average default rate of loans with age between 12 and 36 months. Source: Federal Reserve Bank of St. Louis, INTEX, MSCI

Several market dynamics have appeared to influence the level of delinquencies and defaults in subprime auto loans.4

- Loan age — The default rate has tended to increase initially with loan age; but after reaching a plateau, it has generally decreased as loans age. Borrowers' financial situation has typically improved, as loan amortization kicked in and relatively stronger borrowers survived periods of uncertainty early in the life of the loans.

- Borrowers' creditworthiness — Relevant credit criteria include borrowers' credit scores, the spread between the loan rate and prevailing market rates and loan-to-value ratios.

- Used-car prices — Higher used-car prices generally reduced borrowers' incentive to default. Used-car prices trended downward since 2011 and appear to have contributed to the rise in default rates in recent years, according to MSCI's model for U.S. auto ABS.

- Loan originators' business strategy — Companies may apply different underwriting standards — based on their business strategy.

- Other factors — Unemployment rates, seasonality and vehicle characteristics are some of the other factors that may drive delinquencies and defaults.

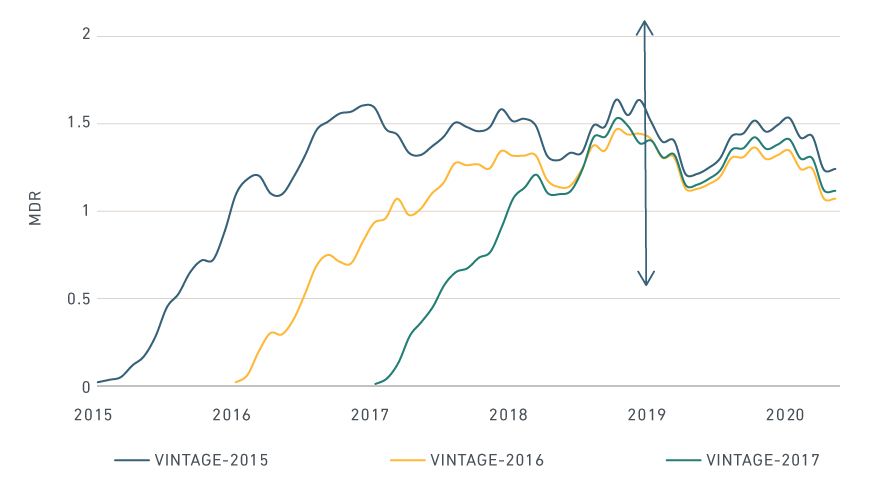

HISTORICAL PERFORMANCE AND MODEL PROJECTIONS FOR 2015-2017 VINTAGES OF US SUBPRIME AUTO ABS

Model projections start from 2019. Source: INTEX, MSCI

Because underwriting standards improved in 2016, our model projects post-2016 vintages will experience about a 0.2 improvement in MDR levels versus the 2015 vintage, assuming used-car prices stay at the current level. The 2015 and prior vintages' performance could start to improve as a result of amortization and weaker borrowers' departure from the cohorts. Subprime auto loans could prove stable, especially if used-car prices increase, according to our model. However, if originators loosen underwriting standards — for example, to compete for market share — subprime-loan performance could deteriorate again.

2 Subprime auto borrowers usually have a credit score below 620, while deep-subprime borrowers' credit scores come in at or below 550.

3 Net Percentage of Domestic Banks Tightening Standards for Auto Loans." Federal Reserve Bank of St. Louis.

4 MSCI Auto Loan Collateral Model." Client access only.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 See, for example: “Investors Rev Up Risk in Subprime Auto Deals.” The Wall Street Journal. Dec. 1, 2018; and “How Scary Are Subprime Auto Loans?” Bloomberg Opinion. Feb. 20, 2019

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.