Are You Ready For Uniform MBS? (Part 1)

Blog post

April 8, 2019

FREDDIE MAC SECURITIES EXCHANGE

Fannie Mae and Freddie Mac will conclude the Single Security Initiative (SSI) on June 3, 2019, creating a single to-be-announced (TBA) market1 and introducing a new TBA security: the uniform mortgage-backed security (UMBS). As this multiyear effort finally approaches its go-live date, we'll share key analyses in two blog posts to help clients navigate this transition. In this first post, we focus on holders of Freddie Mac securities — who may want to exchange their securities. Our analysis suggests that a lack of pricing differentiation within Freddie Mac's indicative price grid across different securities with different attributes may create mispricing.FREDDIE MAC INVESTORS STEP THROUGH THE LOOKING GLASS

The objective is to enhance TBA liquidity and efficiency, by consolidating the securitizations of Fannie Mae (accounting for $2.4 trillion of TBA-eligible securities) and Freddie Mac ($1.1 trillion). While Fannie Mae TBA-eligible securities will be automatically deliverable to the new UMBS, Freddie Mac securities will need to be exchanged into mirror securities first.2 These UMBS-eligible mirror securities are essentially the same as Freddie Mac's original Gold securities — except that the mirror securities' payment delay will be 55 days (the same as Fannie Mae's), instead of 45 days. Starting in May 2019, investors can decide whether to exchange their Gold securities, receiving the float compensation for the additional 10-day delay. One concern of the current Freddie Mac float compensation is that the price grid does not provide very granular price tiering.

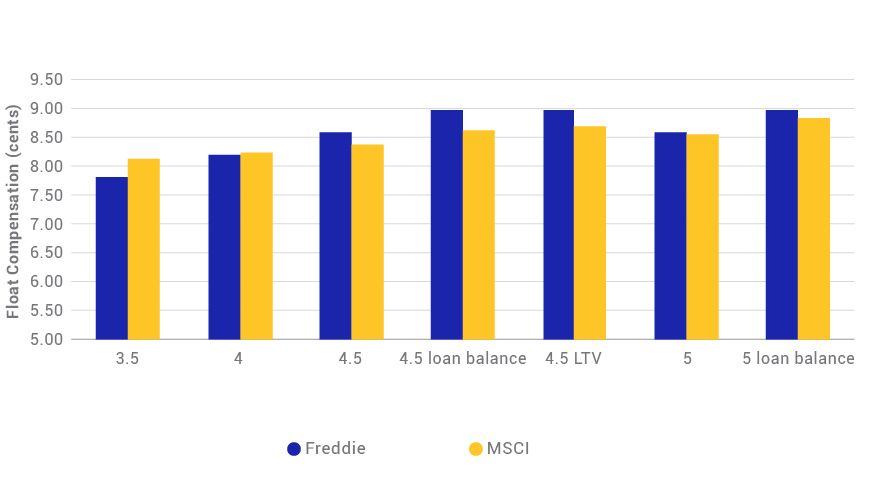

To examine this, we ran all exchange-eligible Freddie Mac Gold securities and corresponding mirror securities through the MSCI Agency Prepayment Model, assuming a constant option-adjusted spread (OAS).3 The pool-level price difference is the theoretical fair float compensation for each security. We then aggregated the results according to Freddie Mac's base (term and coupon) and payup (loan balance, FICO score, loan-to-value ratio and weighted average loan age) cohorts. Freddie Mac's indicative price grid is in line with MSCI pricing models at the aggregated level. The maximum difference at cohort level between the MSCI pricing models and Freddie Mac is within 0.3 cents.

FREDDIE MAC'S FLOAT COMPENSATION PRICES ARE IN LINE WITH MSCI MODELS

Source: Freddie Mac, MSCI Agency Prepayment Model

The float compensation for the 10-day delay depends on the expected amount of cash flow, reinvestment rate and discount rate.

- The reinvestment rate is generally assumed to be one-month LIBOR, with a higher reinvestment rate increasing the value of the compensation.

- The discount rate is usually also based on one-month LIBOR plus the OAS calculated from the prepayment and interest-rate models. A higher discount rate will reduce the present value of the compensation. The discount rate and reinvestment rate largely offset each other.

- Slower prepayment will effectively increase the cash flows of additional coupon payments over a longer period of time. Therefore, securities with more favorable prepayment attributes should generate higher compensation, such as low-loan-balance, low-FICO and New York pools.

- Higher coupons naturally bear greater cash flows of interest payments for reinvestment, therefore leading to higher float compensation, especially given the current relatively flat prepayment intensity across the coupon stack.

FREDDIE MAC'S CURRENT PRICE GRID MAY DISCOURAGE EXCHANGES

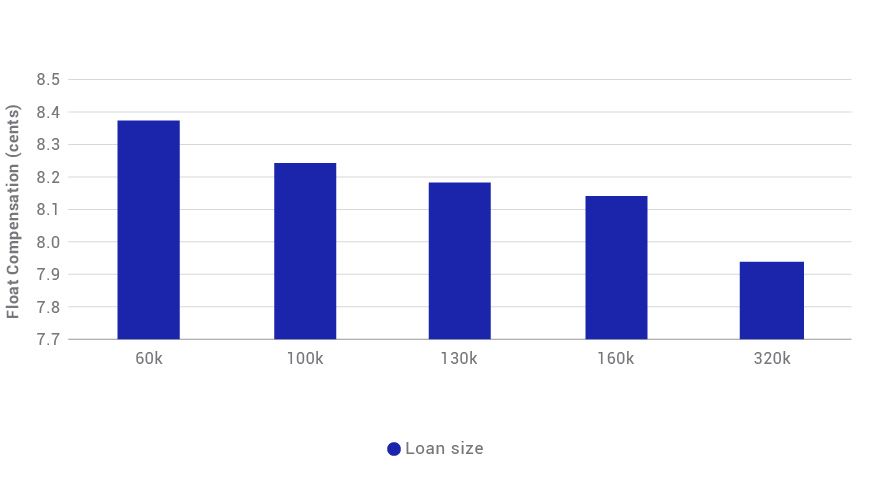

Very often, Freddie Mac's current price grid is the same for all the securities with the same coupon. For example, even though Freddie Mac creates seven buckets for loan balance (ranging from below $85,000 to super-conforming), the actual price grid mostly shows no differential. For example, in the grid published on March 20, all loan-balance buckets showed zero additional compensation for loan-balance payup for the 30-year coupon-4 security. But MSCI models indicate additional float compensation for a fair exchange. The current pricing grid may discourage investors from exchanging certain high-payup securities, such as New York low-loan-balance pools.

MSCI MODELS SHOW ADDITIONAL COMPENSATION FOR LOAN-BALANCE-PAYUP COHORT

Source: Freddie Mac, MSCI Agency Prepayment Model

THE IMPACT OF RATE CHANGES

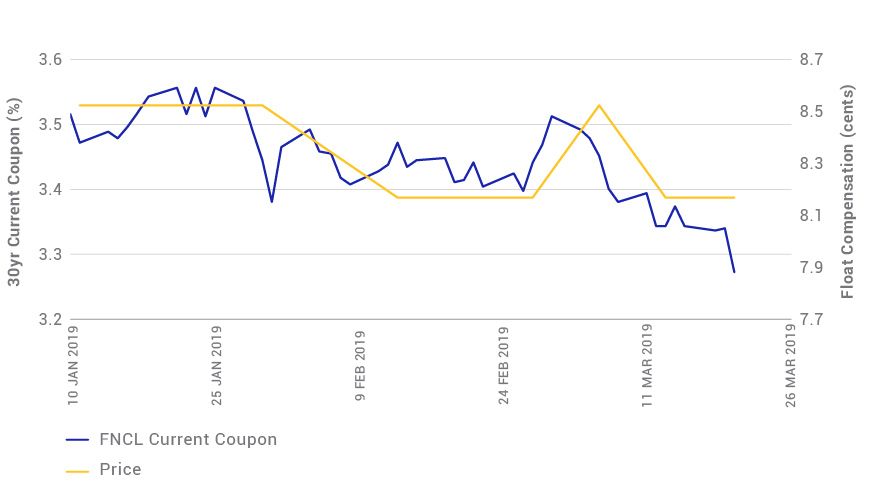

A rate sell-off will slow down the prepayment. As a result, the value of float compensation will increase. This is reflected in Freddie Mac's price grid published during the past three months. Prices dropped about 0.4 cents as rates rallied by about 10 basis points (bps) from January into February, before a quick reversal at the beginning of March. The rally afterward pushed compensation back down to the February level.

FREDDIE MAC'S INDICATIVE PRICE GRID SHOWS PRICE REACTION TO RATE CHANGES

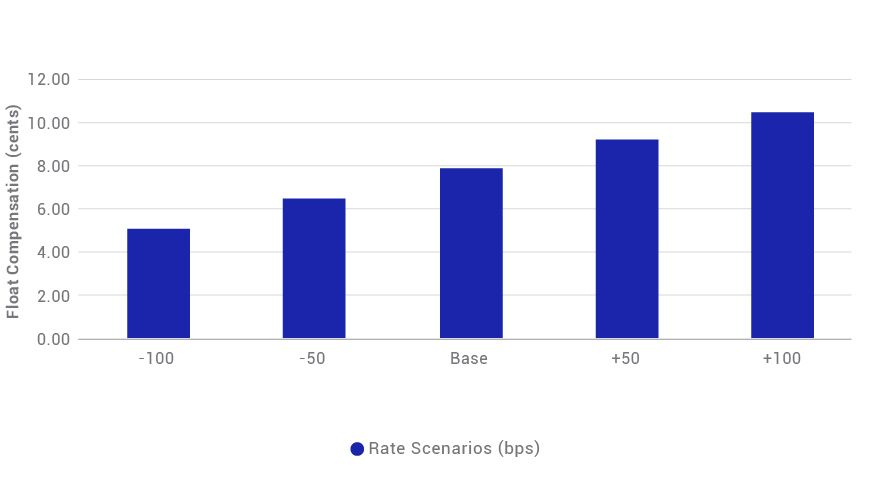

We ran the MSCI prepayment model to price a typical coupon-4 Freddie Mac security with various rate shocks. Freddie Mac's price grid is mostly in line with MSCI models. But the current indicative price grid does not differentiate the loan age for most of the cohorts. For coupon-4 securities, seasoned pools and new originations could have very different rate sensitivity, as they have experienced very different burnout history. Also, the recent extremely high gross/net coupon spread (e.g., for 3.5-coupon securities, a recent 100 bps vs. historical 60 bps) may create a 2-cent compensation discrepancy due to the lack of gross/net coupon spread differentiation, according to the MSCI Agency Prepayment model.

FLOAT COMPENSATION CHANGES UNDER DIFFERENT RATE SCENARIOS

Source: Freddie Mac, MSCI Agency Prepayment Model

In summary, the current float compensation indicated by Freddie Mac for the mirror-security exchange is in line with MSCI models, generally. But the lack of pricing differentiation may create mispricing, which may deter investors from exchanging, or create arbitrage opportunities. Investors, as well as Freddie Mac, may benefit from running bond-level analysis with a well-calibrated prepayment model.

1 "Single Security Initiative and Common Securitization Platform," Federal Housing Finance Agency, March 28, 2018.

2 "Gold PC Exchange." Freddie Mac.

3 Yu, Y. (2018) "MSCI agency fixed rate refinance prepayment model." MSCI Model Insight. (client access only)

Yu, Y. (2018) "MSCI Agency Fixed Rate Base Prepayment Model." MSCI Model Insight. (client access only)

Yu, Y. and Zhang D. (2019) "MSCI Current Coupon Models: Model Risk Premium in a Risk-Neutral Model." MSCI Model Insight. (client access only)

Yu, Y. (2019) "MSCI Primary - Secondary Mortgage Spread Model." MSCI Model Insight. (client access only) 4 Zhang, D. (2017) "Agency MBS Current Coupon Calculation from TBA Prices." MSCI Model Insight. (Client access only)

Yu, Y. (2018) "MSCI Agency Fixed Rate Base Prepayment Model." MSCI Model Insight. (client access only)

Yu, Y. and Zhang D. (2019) "MSCI Current Coupon Models: Model Risk Premium in a Risk-Neutral Model." MSCI Model Insight. (client access only)

Yu, Y. (2019) "MSCI Primary - Secondary Mortgage Spread Model." MSCI Model Insight. (client access only) 4 Zhang, D. (2017) "Agency MBS Current Coupon Calculation from TBA Prices." MSCI Model Insight. (Client access only)

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.