Bridging the gap: Adding factors to indexed and active allocations

Blog post

May 2, 2017

How can asset owners integrate an equity factor allocation into their existing roster of active managers?

There is no one answer that suits all. The response may be different for each asset owner, depending on its investment beliefs, goals and risk tolerance. However, we can use a risk budgeting framework1 to create a core-satellite structure consisting of indexed, active and factor allocations.

For example, a board of trustees may want to adopt a factor program with the goal of harvesting long-term premia. Investment staff decides to use a top-down factor allocation, with the added restriction of preserving existing managers.2 The existing equity portfolio is two-thirds passively managed and one-third actively managed. These capital weights correspond to 150 basis points (bps) of active risk – all of which is consumed by the active managers. We then gradually fund a factor allocation from the indexed allocation, subject to the 150 bps constraint on overall active risk.

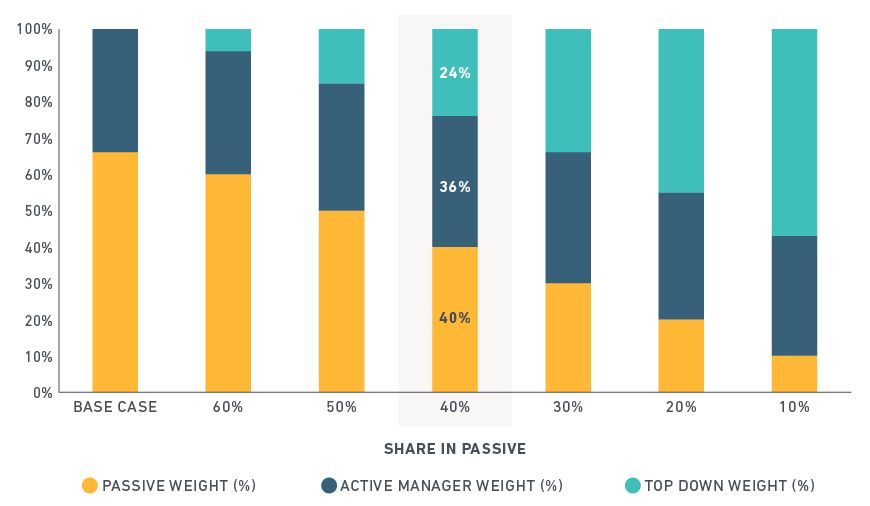

Below, we can see how the indexed allocation can be reduced while staying within the overall risk constraint. For example, the top bar chart shows that it is possible to fund a factor program without necessarily defunding active management. A 40% weight to core indexed corresponds to approximately 40% and 20% weights to the active and factor allocations, respectively.

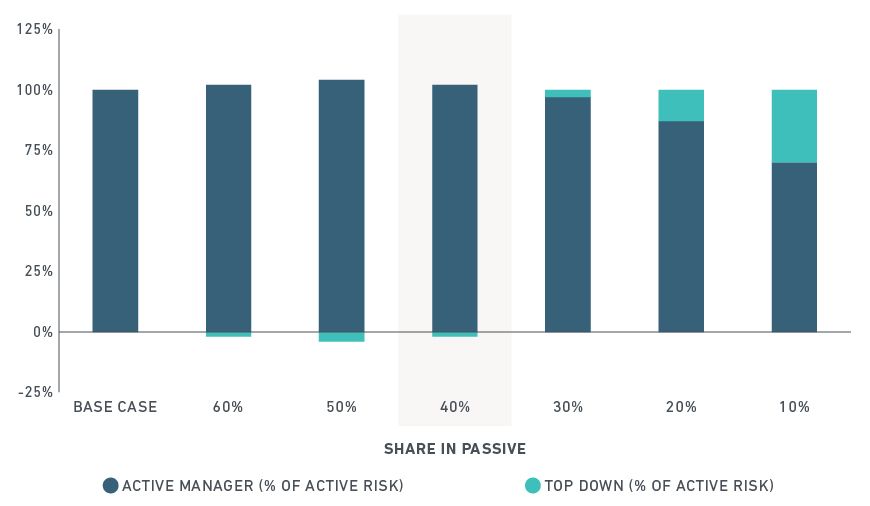

The bottom bar chart shows that this set of weights distributes almost all of the active risk to the active managers, implying that deviations in the equity program's active return will most likely be due to decisions by the active managers.

High Tracking Error Managers and a Top-Down Factor Implementation

Capital Allocation

Active Risk Allocation

In our second scenario, a board of trustees again decides to adopt a factor program with the goal of harvesting long-term premia. This time, however, investment staff is given greater discretion in having the factor program compete with active managers for funding and the risk budget.

The baseline portfolio is the same as in the previous scenario; however the factor allocation is now accomplished via the bottom-up implementation.3 In the below exhibit, we see a very different outcome for asset owners who choose this method.

A 40% weight to indexed results in approximately 30% in both of the factor and active allocations (top bar chart). These weights indicate that staff has higher conviction in factor premia than in the previous scenario. This time, some of the funding for the factor allocation comes from the active managers; in the previous scenario, the factor allocation was funded entirely from the indexed allocation.

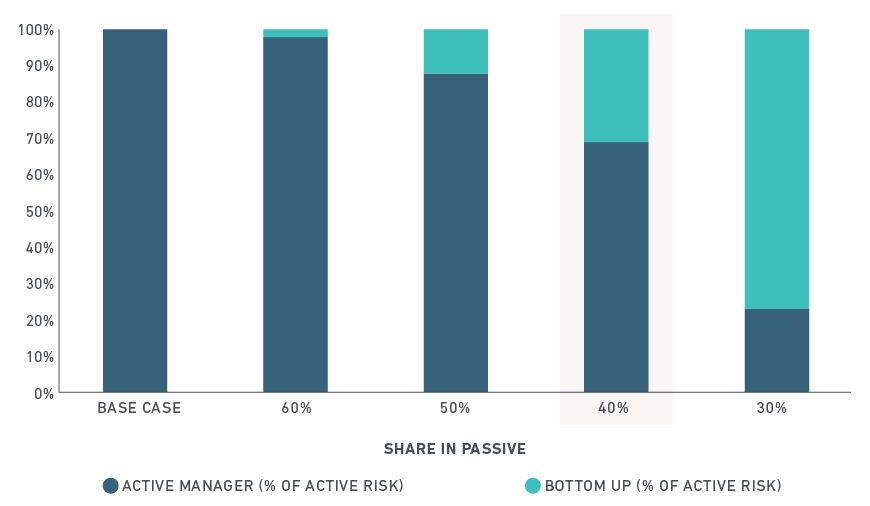

The lower bar chart shows that the active risk is now more evenly shared between the active and factor allocations. In the previous scenario, the active managers consumed the bulk of the 150 bps risk budget.

High Tracking Error Managers and a Bottom-Up Factor Implementation

Capital Allocation

Active Risk Allocation

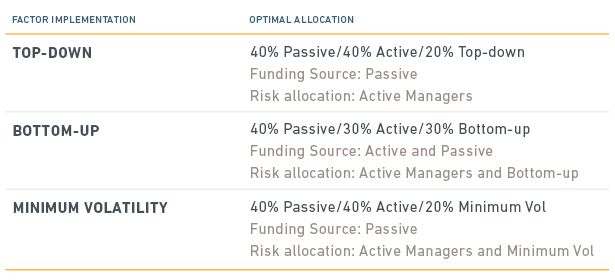

In short, asset owners who wish to preserve their existing roster of active managers, and incorporate factor views, might consider a top-down factor implementation. This approach distributes the bulk of the risk budget to active management, while funding the factor allocation from the core indexed allocation.

Asset owners who wish to preserve their existing roster of active managers, and have high-conviction factor views, might consider a split of capital between active management and a bottom-up factor implementation. This approach more evenly distributes the risk budget to active management and the factor allocation. The factor allocation is partially funded from active management in this scenario.

Lastly, asset owners who pursue a "barbell" strategy between core indexed and active management might consider a low volatility factor allocation. This approach can either derisk the equity program, or increase the allocation to active management. These three approaches are summarized below.

Implementing a factor allocation using risk budgeting

This example assumes that the existing equity portfolio is two-thirds passively managed and one-third actively managed. Active managers have high tracking error (largely value and small-cap managers). The total risk budget is 150 bps.

1 Risk budgeting is helpful because it connects the manager selection process with the factor selection process, without requiring asset owners to forecast expected return assumptions.

2 The top-down approach equal weights six single-factor indexes (size, momentum, quality, value, yield and volatility). The existing manager roster comprises largely value and small-cap managers.

3 The bottom-up strategy tracks the ACWI Diversified Multiple-Factor Index, a stock-level approach that combines value, momentum, size and quality with a control mechanism designed to keep volatility close to the market level.

The author thanks Raman Aylur Subramanian and Dimitris Melas for their contributions to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.