Can MBS Duration Turn Negative?

- Historically high mortgage paydowns and price premium amid the current COVID-19 pandemic may lead to negative duration for mortgage-backed securities (MBS).

- MBS duration is a complex function of prepayment, mortgage rates and stochastic term-structure models, as well as the input price.

- We compared three versions of the MSCI prepayment model through the COVID-19 pandemic to identify shifts in MBS market regimes. These model versions show that the MBS universe will largely stay in positive-duration territory.

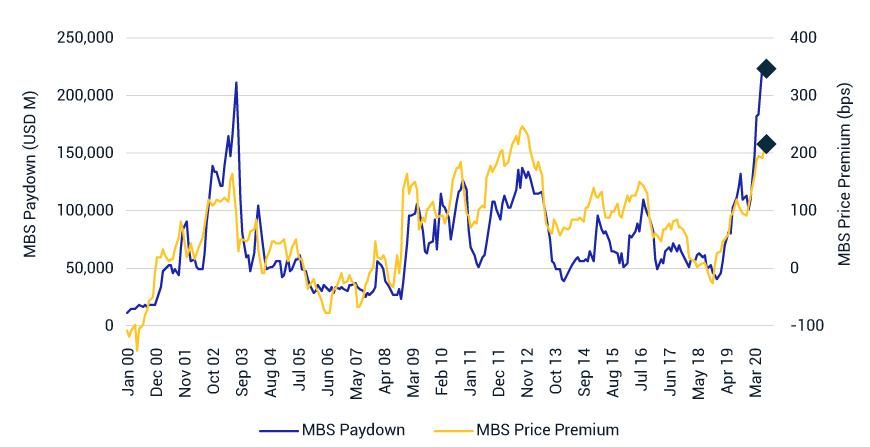

Historically High Paydown and Near-Historically High Price Premium

The historical monthly MBS price premium is defined as the outstanding MBS universe's weighted-average coupon - prevailing current coupon yield. Source: Fannie Mae, Freddie Mac, Ginnie Mae, Recursion, MSCI

The Mechanics of Negative Duration

Option-adjusted duration (OAD), the most common model-based MBS risk measure, is calculated via a prepayment, mortgage-rate and a stochastic term-structure model, with option-adjusted spread (OAS) held constant and rates shocked up/down — e.g., by 10 basis points (bps). A vanilla bond without any embedded option will have a positive duration due to the discount effect — i.e., the price goes up when the rate is shocked lower. But early paydown of mortgages, responding to lower interest rates, could erode the price gain from the discount effect, as the premium above par is lost for these early paydowns. In some cases, the prepayment effect could change the cash flow so much that the duration could turn negative.

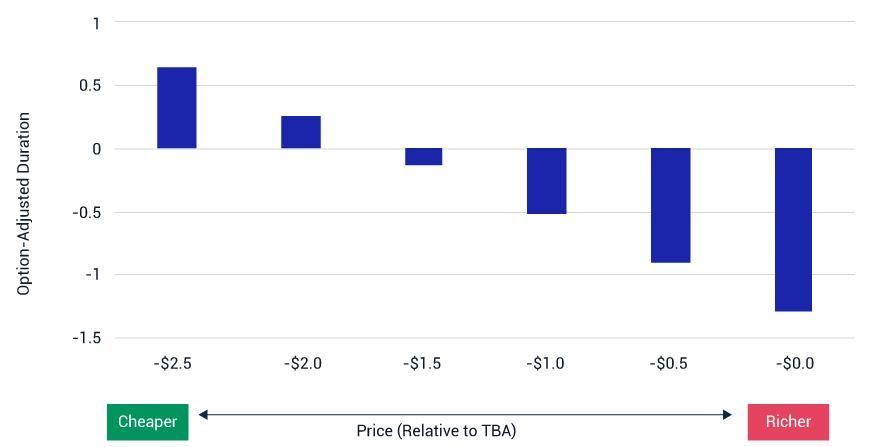

Certain mortgages may exhibit higher prepayment propensities — e.g., high-balance loans (those whose balance exceeds the agencies' conforming limit). High-balance loans are usually securitized separately to avoid disruption to the to-be-announced (TBA) market's pricing.3 These high-balance MBS are usually priced lower than TBA because of their greater sensitivity to being prepaid as rates decline. If the price is marked closer to TBA (richer), the ultrafast prepayment projection may dominate the OAD calculation, as we see in the exhibit below.

High-Balance MBS Are More Susceptible to Negative Duration

The analysis was performed for the Ginnie Mae II 3% coupon with the assumptions of loan balance = USD 650,000 and California = 50%. Various prices are assumed relative to the Ginnie Mae II TBA price.

The exhibit above shows the OAD profile across different price assumptions for a hypothetical Ginnie Mae II 3% coupon with high loan balances. The OAD was more negative for richer prices. When the input price was adjusted downward, enough to account for the collateral's more adverse prepayment response, the OAD eventually turned positive.

The choice of stochastic term-structure model for the valuation also impacts the OAD in a profound way,4 especially as market-implied volatility skew has turned to super-normal shape in the past two years — i.e., volatility is higher when the rate is lower, which tends to reduce OAD.

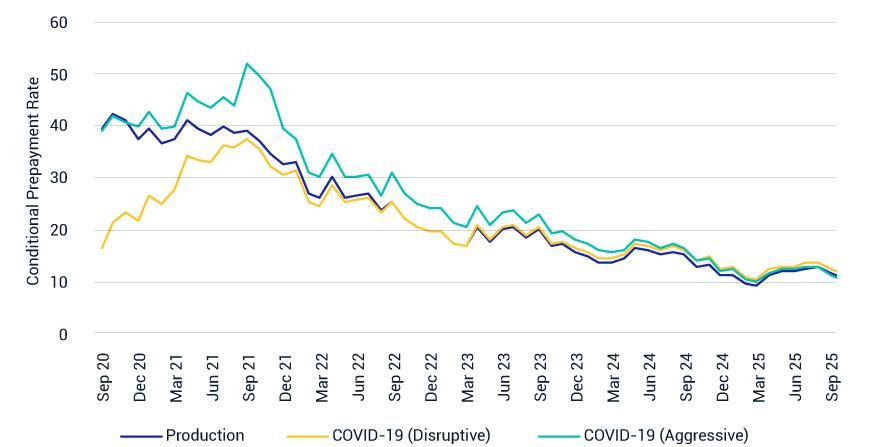

Three Model Versions: One Prepayment Story

The COVID-19 pandemic created large prepayment uncertainties in the second quarter. Due to the accommodative policy changes from Fannie Mae, Freddie Mac, Ginnie Mae and government entities, the mortgage-origination process experienced only minimal disruption. We drew on the comparison between three versions of MSCI's prepayment model through the pandemic to gauge the market's implied view on durations. The three model versions are:

- Production: the current released version of the MSCI Agency Prepayment Model5

- COVID-19 (Disruptive): 30-40% near-term prepayment slowdown due to COVID-19

- COVID-19 (Aggressive): Further decrease of mortgage rates (alleviation of mortgage-origination capacity constraint) and reduction of the refinance burnout effect (high prepayment speed sustained for longer time)

Different Prepayment Projections ...

Fannie Mae 30-year 3% coupon, 2019 vintage.

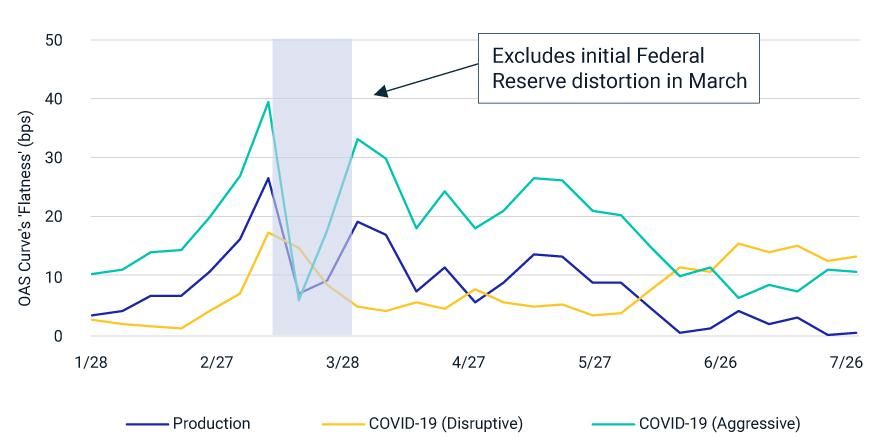

The OAS for different uniform MBS (UMBS) TBA coupons can be calculated with the three model versions. When a model is consistent with market expectations, the OAS curve across the coupon stack tends to be flatter, or have a smaller standard deviation. In the early months of the pandemic, the market expected a large prepayment disruption, even when realized overall prepayment nearly reached 30 CPR in April and May.

Flatter OAS Curve of 'COVID-19 (Disruptive)' Model Implied Refinance Disruption Before June

"Flatness" is defined as the standard deviation of OAS across the UMBS coupon stack.

The exhibit above also shows the flatness of the OAS curve for the "COVID-19 (Aggressive)" model. Can the mortgage rate grind lower as the origination capacity ramps up in the near term and the spread between the mortgage rate and 10-year Treasury tightens? The "Production" model shows this spread may tighten gradually under the condition that refinance activity starts to slow down. The net effect is that prepayment speed will remain flat in the near term.

In contrast, the "COVID-19 (Aggressive)" model, with the combination of unconditional mortgage-rate reduction in the near term, as well as reduction of refinance burnout effect, may lead to a shorter MBS duration (negative in some cases). Currently, the "COVID-19 (Aggressive)" model still underperforms the "Production" model, in terms of the flatness of the OAS curve.

'COVID-19 (Aggressive)' Model May Lead to More Negative Durations

In summary, the combination of high prepayment expectation and MBS price premium may lead to negative MBS duration. Even though our analysis shows that negative duration largely remains a special case, investors may want to take heed.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The most recent 30-year mortgage rate is quoted at 2.9% on average, according to Freddie Mac’s weekly survey.2Certain MBS collateralized mortgage obligations — e.g., interest-only bonds — have negative duration naturally, as their cash flows are dominated by changing prepayment projections, due to their capital structure. We focus on the largest asset class, pass-throughs, in this blog post.3High-balance loans can consist of up to 10% of conventional MBS pools to satisfy SIFMA’s “Standard Requirements for Delivery on Settlements of UMBS and Ginnie Mae Securities.”4Yu, Y. and Zhang, D. 2020. “A ‘Normal’ Choice of Interest-Rate Model for MBS.” MSCI Research Insight.5Yu, Y. 2020. “MSCI Agency Prepayment Model performance and updates through COVID-19.” MSCI Model Insight.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.