Companies May Not Be Ready for SEC Climate-Disclosure Rules

- Only 28% of companies we analyzed recently disclosed Scope 1 and 2 emissions, and 15% disclosed any portion of their Scope 3 emissions.

- Disclosure rates were highest on average in some of the most emission-intensive sectors and lowest in the least emission-intensive sectors.

- Less than 2% of companies had set a Scope 3 target but not disclosed Scope 3 emissions.

Emission footprints are a starting point for assessing climate-related risk

Disclosures of GHG-emission metrics are of particular interest to investors as they form the basis for further assessments of climate-related risk. How exposed is a company to carbon-pricing mechanisms and other aspects of transition risk? How comprehensive and ambitious is a company's climate target? An investor likely needs to know a company's GHG emissions to be able to make these assessments. Or to use a cliché: You can't manage what you can't measure.

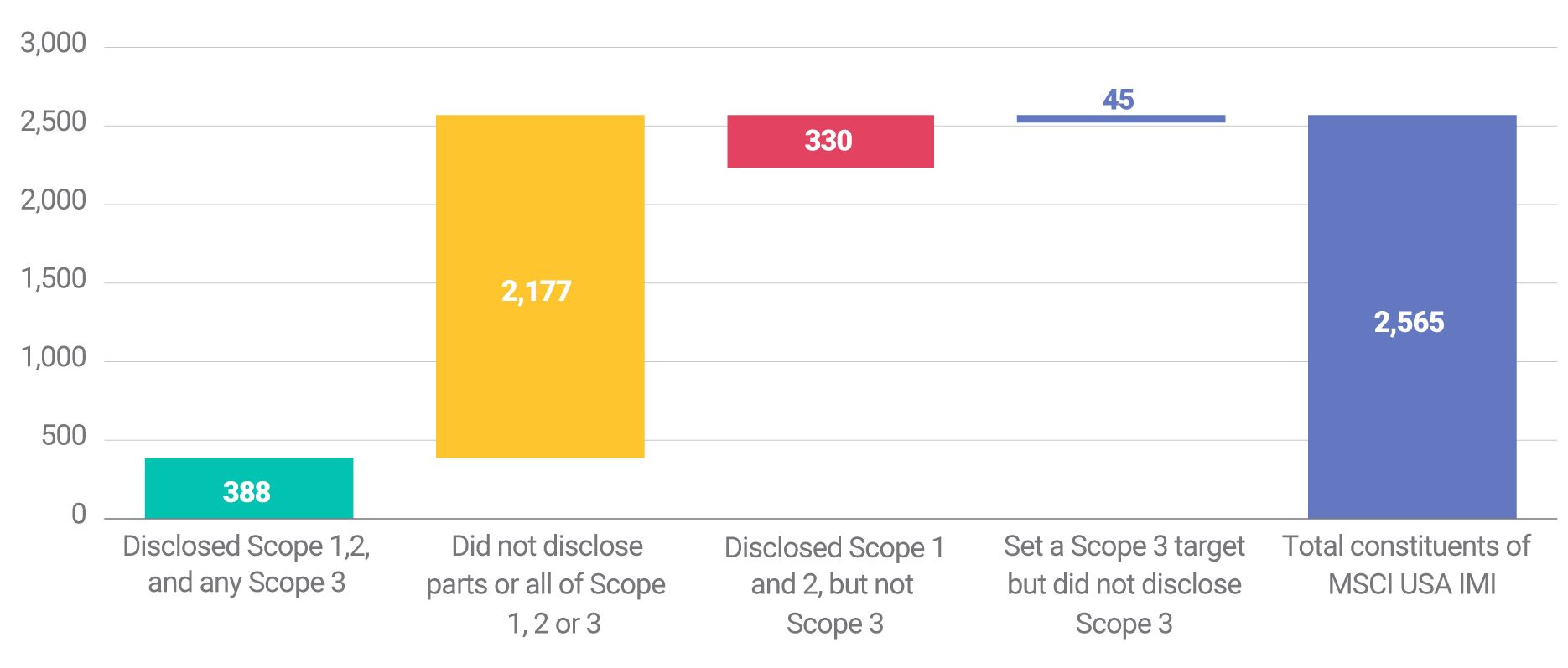

The status of US-listed companies' emission disclosures

Data as of March 23, 2022. Total universe includes the 2,565 constituents of MSCI USA Investable Market Index, as of March 22, 2022, with market cap greater than USD 75 million and which are covered by MSCI ESG Research Carbon Metrics. Data includes latest disclosures, as of 2019 or 2020. Source: MSCI ESG Research LLC

Disclosure rates of GHG emissions in this sample of companies were low: 28% of companies disclosed both Scope 1 and 2 emissions. Under the proposed rule, all companies would be required to disclose these emissions and meet attestation requirements.

Only 15% disclosed any Scope 3 emissions (i.e., those from a company's value chain). Already low, 15% is likely an overestimate of the number of companies that may already meet proposed Scope 3 disclosure requirements. Often, companies disclose only a portion of their Scope 3 emissions, such as business travel, but not other, potentially more relevant emission categories, such as emissions from the use of the products the company sells. The proposed rule does not include an attestation requirement for Scope 3 emissions.

The proposed rule also includes requirements for companies that set emission-reduction targets that include Scope 3 emissions to disclose those emissions. We found that less than 2% of companies (45) in our sample had set targets that included Scope 3, but had not yet disclosed their Scope 3 emissions.

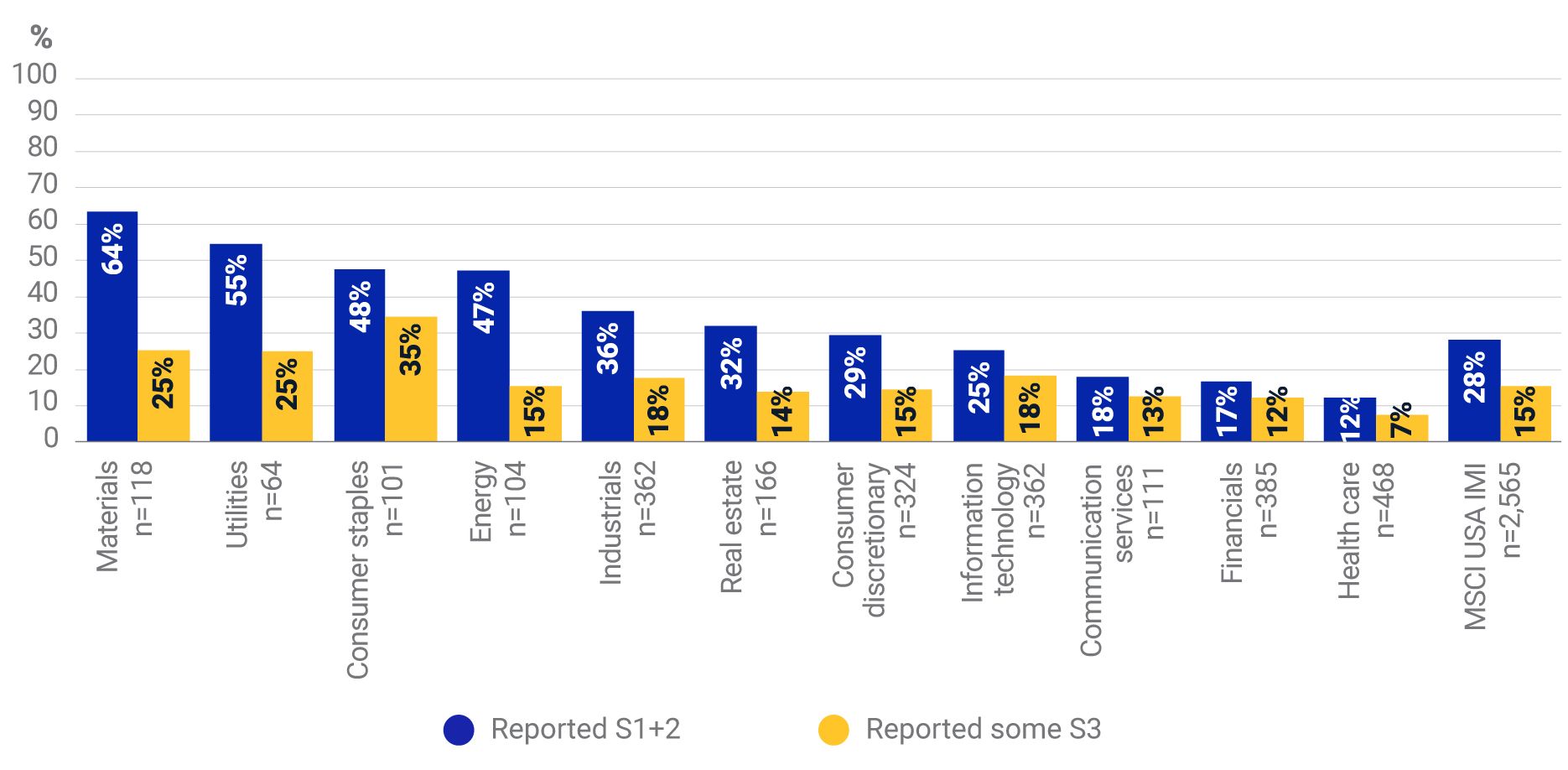

Average GHG-emission disclosure rates of US-listed companies by sector and scope

Data as of March 23, 2022. Total universe includes 2,565 constituents of the MSCI USA Investable Market Index, as of March 22, 2022, with market cap greater than USD 75 million and which are covered by MSCI ESG Research Carbon Metrics. Sectors are derived from the Global Industry Classification Standard (GICS®), which was jointly developed by MSCI and S&P Global Market Intelligence. Data includes latest disclosures, as of 2019 or 2020. Source: MSCI ESG Research LLC

We also looked at how disclosure rates varied on average by sector. Two results stood out.

- Disclosure rates were higher on average in some of the most emission-intensive sectors: materials (64%), utilities (55%), consumer staples (48%) and energy (47%).

- Disclosure rates were lower on average in the least emission-intensive sectors: health care (12%), financials (17%), communication services (18%) and information technology (25%).

Many companies face an uphill battle

Climate-related disclosure requirements are also becoming more common in jurisdictions outside the U.S. At least 12 jurisdictions — including the EU, Canada, China and Japan — have implemented some form of TCFD-aligned regulations. While targeting the same goal, they often vary in stringency, specificity and timeline. Regulators have listened to growing demand from investors for these disclosures. But the road ahead appears to be uphill for U.S.-listed companies, as most will have to get their emission-accounting books in order to meet these requirements (if unchanged from the current proposal) by 2024, 2025 or 2026, depending on their filing requirements.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The rule proposed batches of disclosure requirements. The first batch covers the largest companies and would require them to disclose Scope 1 and 2 emissions beginning in 2024 and Scope 3 emissions the following year. The second batch of smaller companies would follow on the same two-year schedule, but starting in 2025. Finally, the smallest companies regulated by the SEC would be required to disclose Scope 1 and 2 emissions in 2026, but not required to disclose Scope 3 emissions. “Proposed rule: The Enhancement and Standardization of Climate-Related Disclosures for Investors.” Securities and Exchange Commission, March 21, 2022.2The proposed rule, released on March 21, is in a 60-day comment period as of this writing, and may change.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.