Corporate-bond performance by factors and ESG

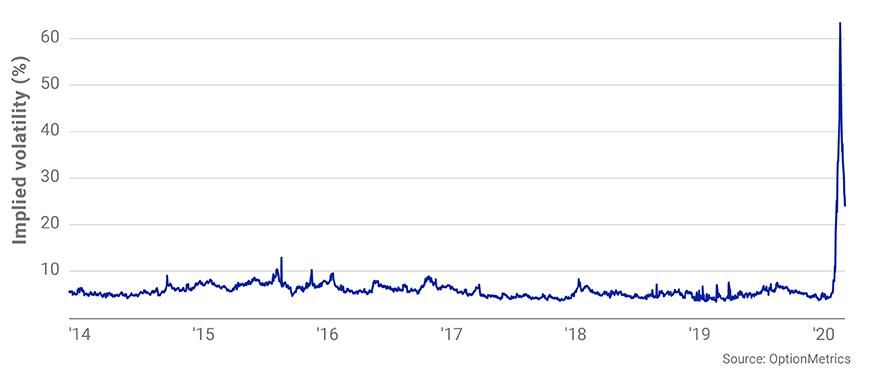

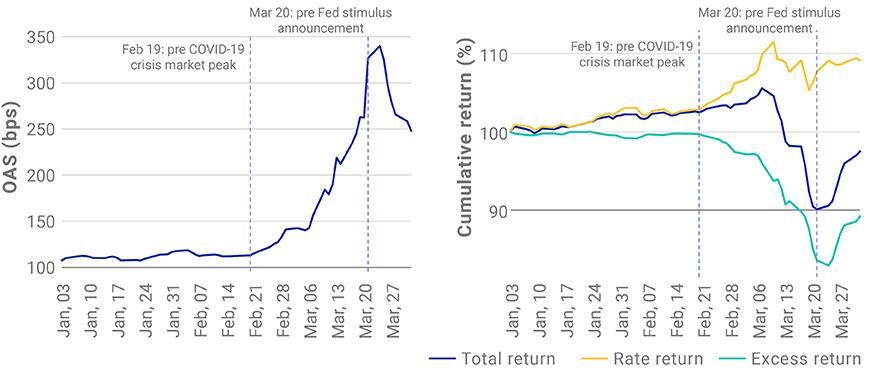

- The MSCI USD Investment Grade (IG) Corporate Bond Index ("parent index") experienced relentless bouts of market volatility over Q1 2020, despite these bonds' relatively higher credit rating on the credit spectrum.

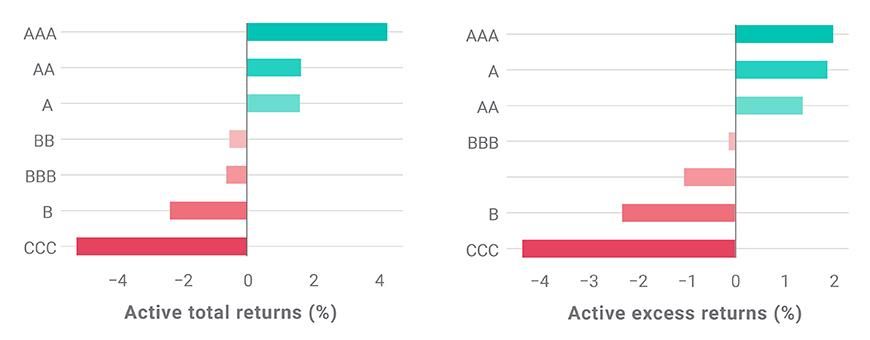

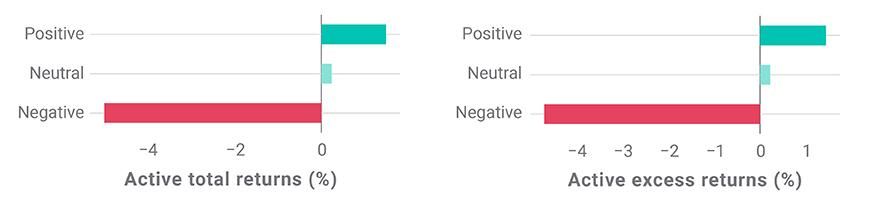

- Within corporate-bond segments, defensive factors, e.g., low risk and quality, fared relatively well. Issuers with higher ESG exposure displayed more resilient excess returns. A similar trend existed over the last five years.

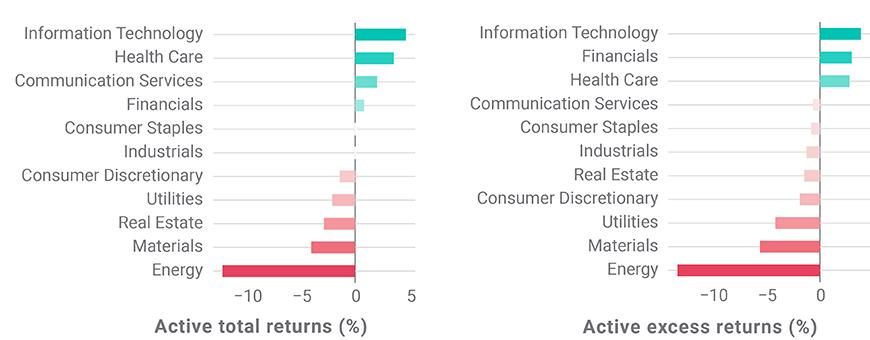

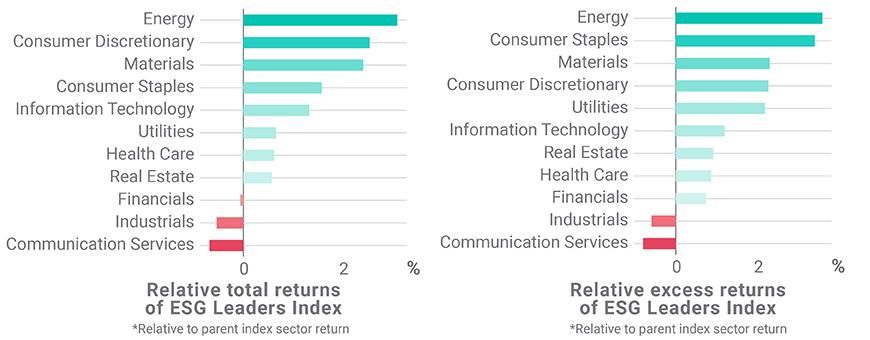

- Relative to the parent index, energy underperformed while IT and healthcare outperformed in Q1 2020. Most MSCI USD IG ESG Leaders Corporate Bond Index sectors outperformed the respective parent index sectors.

('MSCI USD IG Corporate Bond Index (Q1 2020 performance)', 'MSCI USD IG Corporate Bond Index (Q1 2020 performance)') | ('Total return', 'Unnamed: 1_level_1') | ('Rate return', 'Unnamed: 2_level_1') | ('Excess return', 'Unnamed: 3_level_1') |

|---|---|---|---|

('MSCI USD IG Corporate Bond Index (Q1 2020 performance)', 'MSCI USD IG Corporate Bond Index (Q1 2020 performance)') -2.50% | ('Total return', 'Unnamed: 1_level_1') 9.17% | ('Rate return', 'Unnamed: 2_level_1') -11.68% | ('Excess return', 'Unnamed: 3_level_1') None |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') | ('MSCI USD IG Corporate Bond index total returns', '1 Year') | ('MSCI USD IG Corporate Bond index total returns', '3 Year') | ('MSCI USD IG Corporate Bond index total returns', '5 Year') |

|---|---|---|---|---|---|

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Parent index | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') USD IG Corp Bond | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -2.5% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 6.0% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 13.8% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 18.1% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Low Risk | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -2.1% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 4.1% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 10.4% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 14.4% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Quality | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -0.8% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 7.1% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 14.7% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 18.7% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Carry | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -5.3% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 5.4% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 14.4% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 18.3% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Low Size | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -3.6% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 4.6% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 12.0% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 15.7% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Value | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -3.0% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 5.8% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 13.4% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 17.5% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') ESG indexes | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') ESG Leader | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -1.8% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 6.5% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 14.5% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 18.4% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') ESG indexes | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') ESG Universal | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -2.0% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 6.6% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 14.2% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 18.3% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') None | ('MSCI USD IG Corporate Bond index total returns', '1 Year') None | ('MSCI USD IG Corporate Bond index total returns', '3 Year') None | ('MSCI USD IG Corporate Bond index total returns', '5 Year') None |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') None | ('MSCI USD IG Corporate Bond index total returns', '1 Year') None | ('MSCI USD IG Corporate Bond index total returns', '3 Year') None | ('MSCI USD IG Corporate Bond index total returns', '5 Year') None |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') MSCI USD IG Corporate Bond index excess returns | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') MSCI USD IG Corporate Bond index excess returns | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') MSCI USD IG Corporate Bond index excess returns | ('MSCI USD IG Corporate Bond index total returns', '1 Year') MSCI USD IG Corporate Bond index excess returns | ('MSCI USD IG Corporate Bond index total returns', '3 Year') MSCI USD IG Corporate Bond index excess returns | ('MSCI USD IG Corporate Bond index total returns', '5 Year') MSCI USD IG Corporate Bond index excess returns |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') None | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') Q1 2020 | ('MSCI USD IG Corporate Bond index total returns', '1 Year') 1 Year | ('MSCI USD IG Corporate Bond index total returns', '3 Year') 3 Year | ('MSCI USD IG Corporate Bond index total returns', '5 Year') 5 Year |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Parent index | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') USD IG Corp Bond | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -11.6% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -8.6% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -7.1% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -4.6% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Low Risk | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -8.4% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -6.3% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -4.6% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -2.3% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Quality | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -9.9% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -7.5% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -6.0% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -3.8% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Carry | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -16.6% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -12.7% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -11.0% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -8.2% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Low Size | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -12.7% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -10.1% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -8.8% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -6.8% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') Factor indexes (tilt) | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') Value | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -12.1% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -9.0% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -7.5% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -5.1% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') ESG indexes | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') ESG Leader | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -10.4% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -7.7% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -5.9% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -3.7% |

('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 0_level_1') ESG indexes | ('MSCI USD IG Corporate Bond index total returns', 'Unnamed: 1_level_1') ESG Universal | ('MSCI USD IG Corporate Bond index total returns', 'Q1 2020') -11.2% | ('MSCI USD IG Corporate Bond index total returns', '1 Year') -8.1% | ('MSCI USD IG Corporate Bond index total returns', '3 Year') -6.8% | ('MSCI USD IG Corporate Bond index total returns', '5 Year') -4.4% |

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.