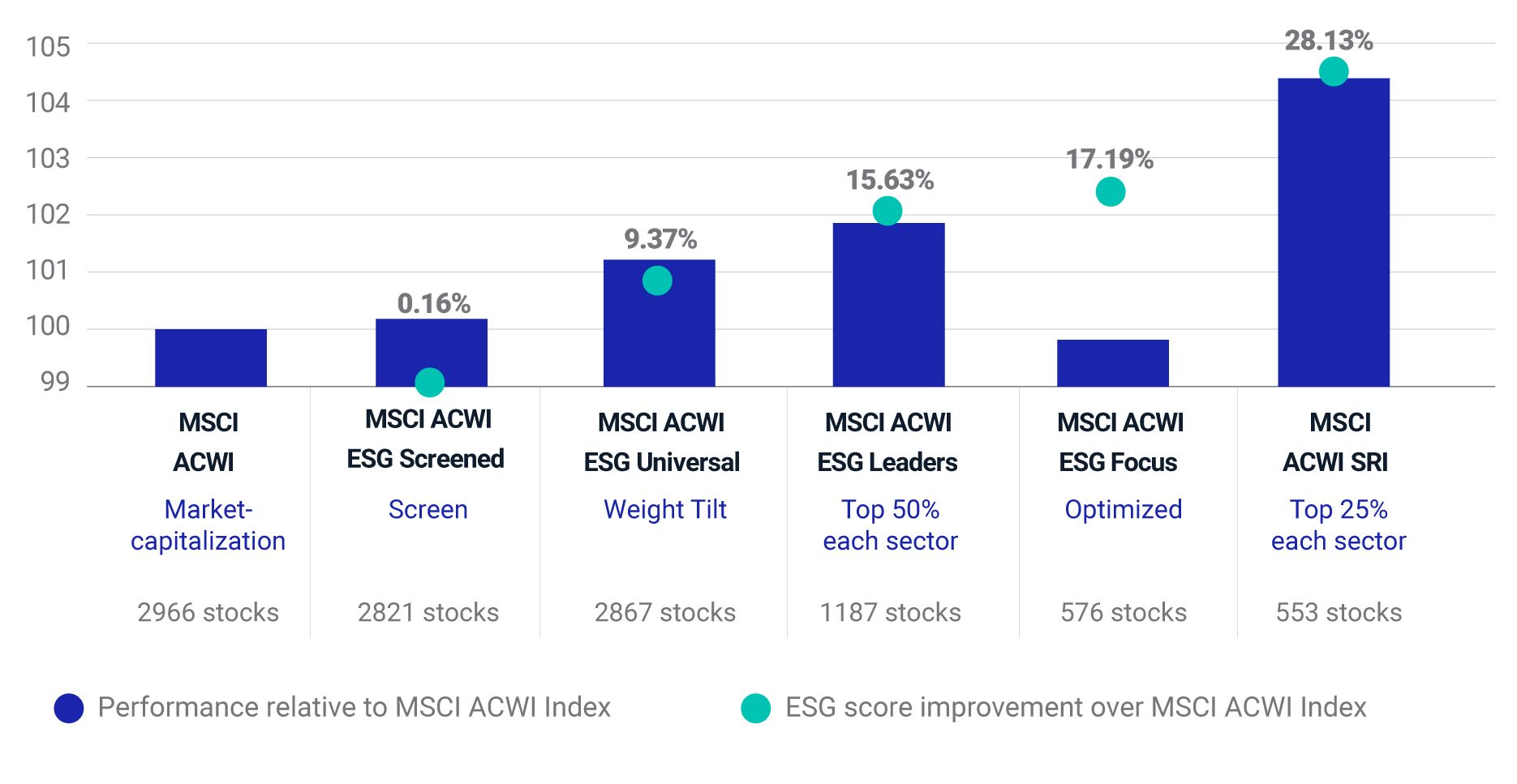

Despite Oil & Gas’s Rebound, ESG Indexes Outperformed

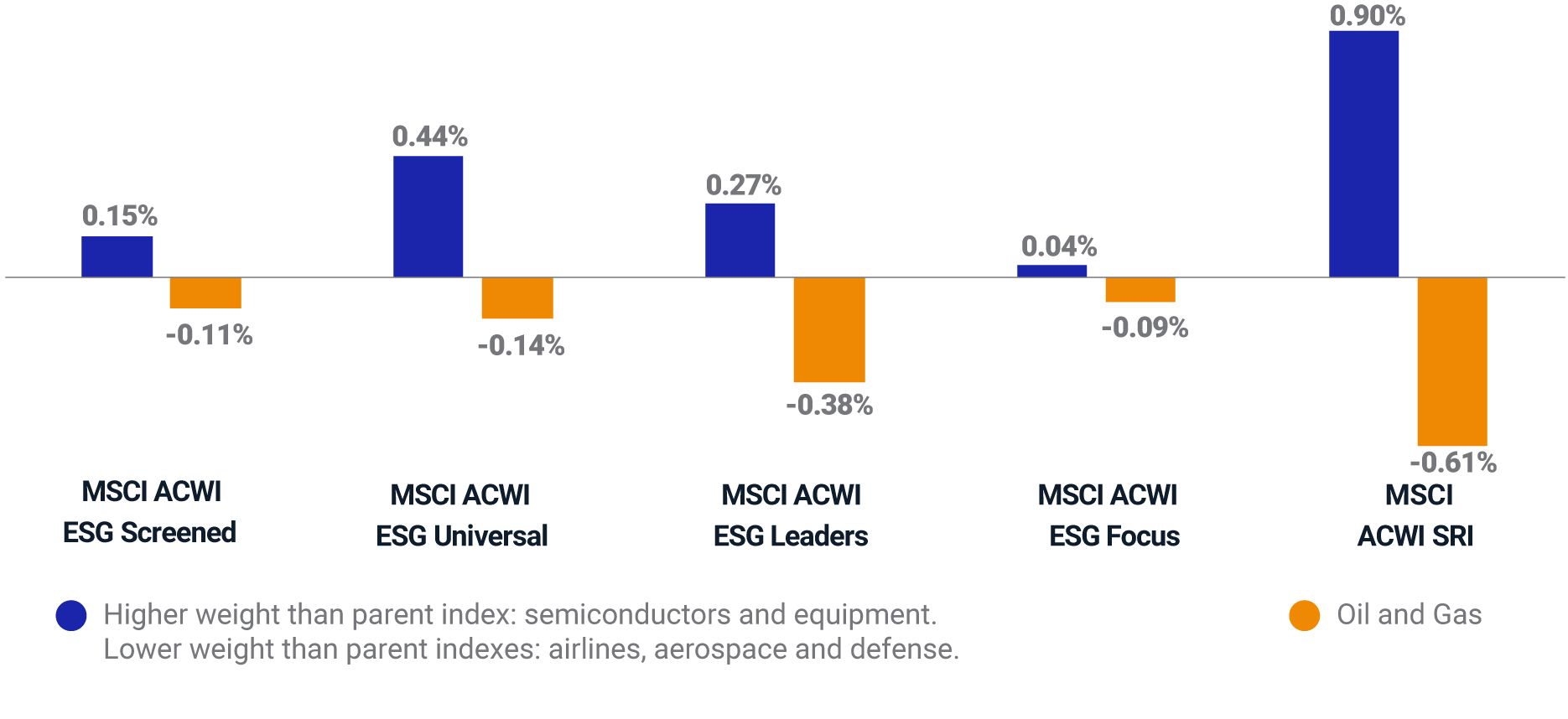

- Despite the rebound in oil and gas prices during 2021, the performance drag of lower weightings to oil and gas stocks on flagship MSCI ACWI ESG Indexes was marginal.

- Industries had a limited impact on the performance of MSCI ESG Indexes.

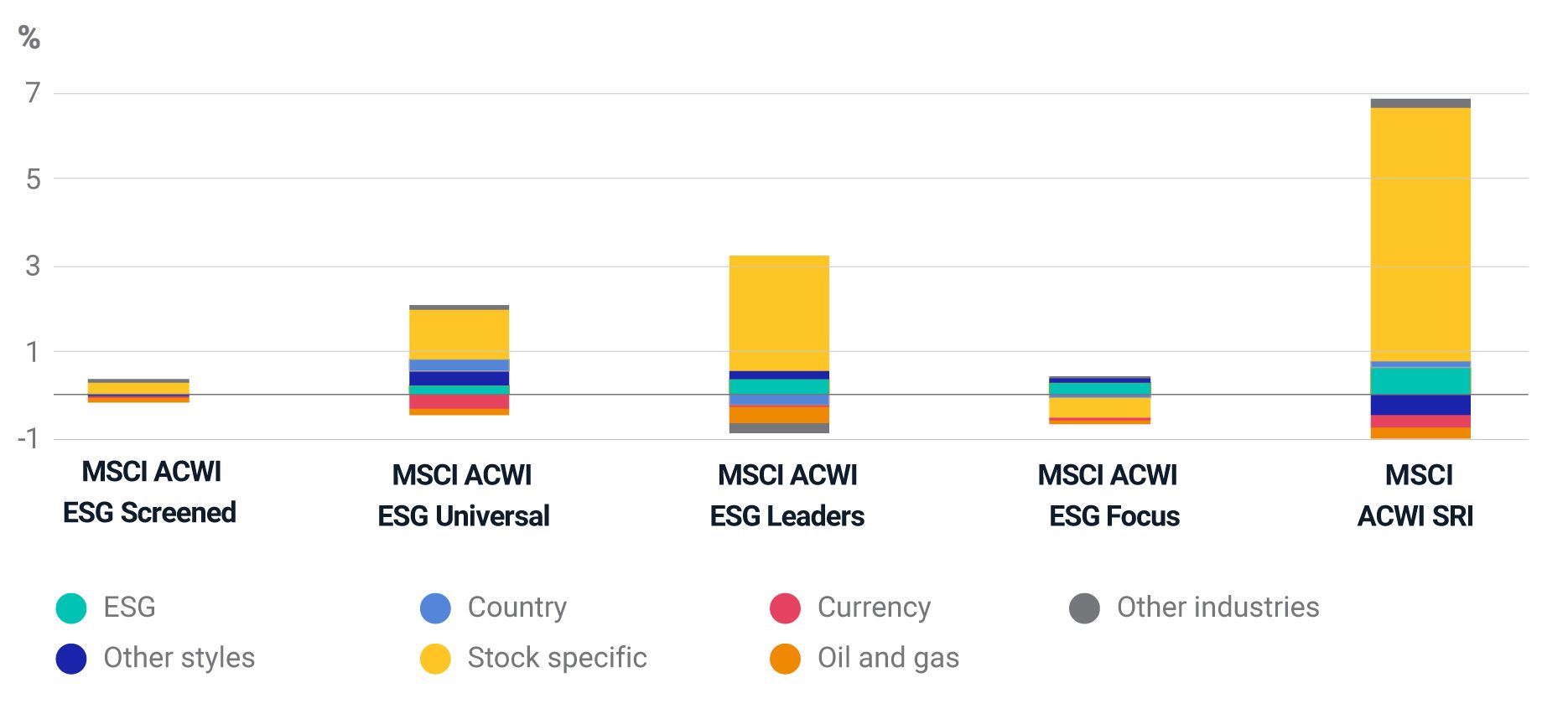

- The highest contribution to active returns for MSCI ESG Indexes in 2021 was from stock-specific returns.

None | MSCI ACWI | MSCI ACWI ESG Screened | MSCI ACWI ESG Universal | MSCI ACWI ESG Leaders | MSCI ACWI ESG Focus | MSCI ACWI SRI |

1 Yr | 19.0 | 19.2 | 20.5 | 21.3 | 18.8 | 24.5 |

3 Yr | 21.0 | 21.7 | 22.3 | 21.8 | 22.0 | 25.0 |

5 Yr | 15.0 | 15.4 | 15.8 | 15.5 | 15.8 | 18.0 |

Gross returns for the period ending Dec. 31, 2021. Returns are annualized for periods longer than a year.

MSCI ACWI ESG Screened | MSCI ACWI ESG Universal | MSCI ACWI ESG Leaders | MSCI ACWI ESG Focus | MSCI ACWI SRI |

MICROSOFT CORP.(AAA) | MICROSOFT CORP. (AAA) | MICROSOFT CORP. (AAA) | ALPHABET INC. (BBB) | MICROSOFT CORP. (AAA) |

WALMART INC. (BBB*) | NVIDIA CORP. (AAA) | TESLA INC. (A) | MODERNA INC. (BB*) | TESLA INC. (A) |

TESLA INC. (A) | HOME DEPOT INC. (AA) | ALPHABET INC. (BBB) | MEDTRONIC PLC (BB degrees ) | NVIDIA CORP. (AAA) |

ALPHABET INC. (BBB) | ALPHABET INC. (BBB) | NVIDIA CORP. (AAA) | BYD CO. LTD. (A) | HOME DEPOT INC. (AA) |

NVIDIA CORP (AAA) | NETFLIX INC. (BB) | HOME DEPOT. INC (AA) | NUCOR CORP. (BBB) | SHOPIFY INC. (AA*) |

HOME DEPOT INC. (AA) | NOVO NORDISK A/S (AAA) | THERMO FISHER SCIENTIFIC INC. (BBB) | PELOTON INTERACTIVE INC. (CCC degrees ) | NOVO NORDISK A/S (AAA) |

PFIZER INC. (B) | SONY GROUP CORP. (AAA) | SHOPIFY INC. (AA*) | HUBSPOT INC. (AA*) | SONY GROUP CORP. (AAA) |

META PLATFORMS INC. (B) | INTUIT INC. (AA) | NOVO NORDISK A/S (AAA) | NATURGY ENERGY GROUP S.A. (AAA) | CHARLES SCHWAB CORP. (BBB*) |

UNITEDHEALTH GROUP INC. (BB) | QUALCOMM INC. (BB*) | ACCENTURE PLC (AA*) | CONTEMPORARY AMPEREX TECHNOLOGY CO. LTD. (BBB degrees ) | ASML HOLDING N.V. (AAA) |

SHOPIFY INC. (AA*) | LOWE'S COMPANIES INC. (AA) | SONY GROUP CORP. (AAA) | SONY GROUP CORP. (AAA) | LOWE'S COMPANIES INC. (AA) |

We explain the methodology of MSCI ESG Ratings in What is an MSCI ESG Rating? If a stock improved its ESG rating since last rating revision, we identify it as positive trend. If the rating has declined, it is a negative trend. See MSCI ESG Investing, Better investments for a better world for more details. Data from Dec. 31, 2020, to Jan. 2, 2022.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.