Did corporate-credit factors offer a risk-return edge?

Blog post

January 24, 2020

- Factors have gained popularity in equity investing for providing insight into the key drivers of portfolio risk and returns. We simulated the performance of five fixed-income factors using hypothetical portfolios, from September 2015 to June 2019.

- Tilts toward certain corporate-bond factors would have helped reduce risk, increase income or generate active returns in our simulated portfolios, during our analysis period.

- Indexes based on corporate-bond factors may also prove useful as benchmarks for active managers.

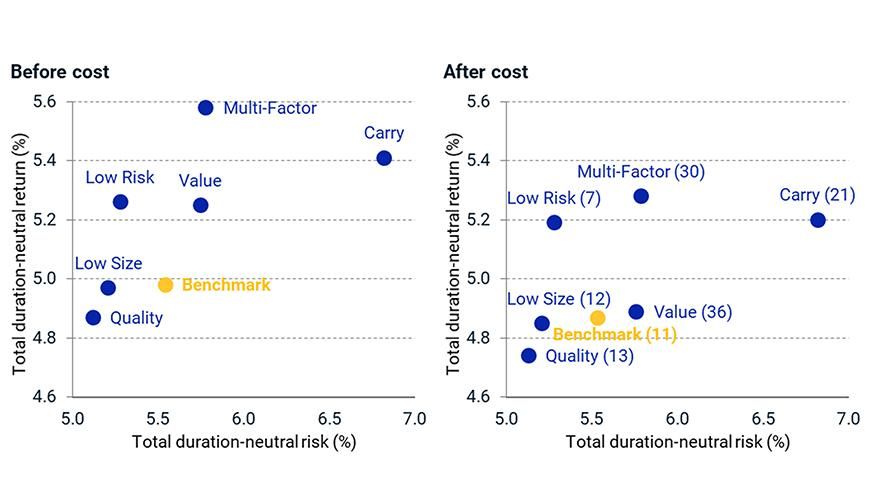

Factor approaches to USD investment-grade corporate bonds

Factors have gained popularity in equity investing for potentially providing insight into the key drivers of portfolio risk and returns. In a new research paper, we examined (among other things) whether tilting hypothetical fixed-income portfolios toward some bond-specific factors would have benefited investors, over the period of our analysis (September 2005 to June 2019). We focused on USD investment-grade corporate bonds because of their higher yet stable cash flows relative to the low- and negative-yielding debt issued by developed-market governments.2 Varying the simulated portfolios' exposures to value, low size, quality, carry and low risk delivered outperformance on an absolute or risk-adjusted basis, during our study period.3

Factor strategies' performance versus the benchmark

Simulated performance of long-only factor-tilted strategies and the MSCI USD IG Corporate Bond Index, before and after including transaction costs (cost in bps in parentheses). Total duration-neutral return (risk) is the return (risk) of the long-only corporate-bond strategy after neutralizing for the active (relative to benchmark) duration-matched Treasury returns. Multi-factor is derived from value, low size, carry and low risk. Sample period is September 2005 to June 2019.

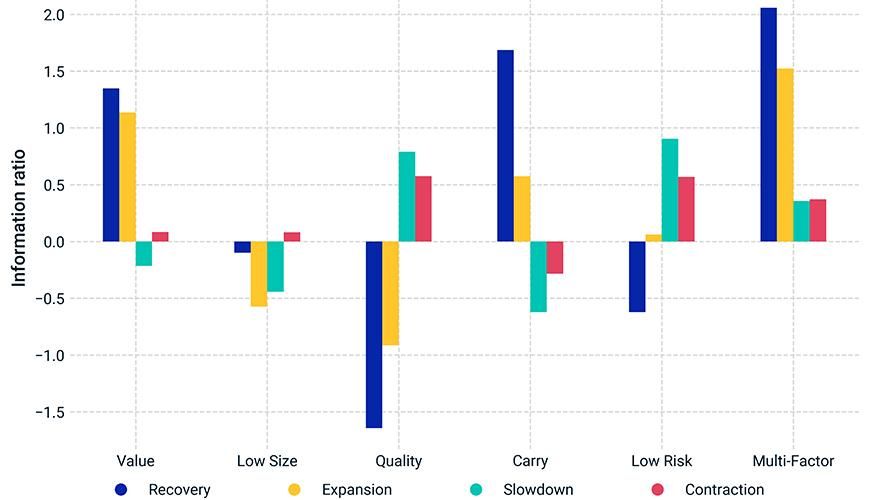

Like their equity counterparts, some fixed-income factors have historically displayed procyclical characteristics, while others have offered more defensive exposures at various points in the economic cycle. In the exhibit below, we plot the excess risk-adjusted returns of single- and multi-factor strategies during four economic scenarios based on the Organization for Economic Cooperation and Development's composite leading indicator (CLI) for USD-denominated corporate-credit factors. Factors such as value and carry have shown pro-cyclical characteristics in the past, while quality and low risk have shown defensive characteristics.

How factors performed in four economic scenarios

Simulated average active excess risk-adjusted returns of long-only factor-tilted strategies versus the MSCI USD IG Corporate Bond Index, without transaction costs, under four economic scenarios. Multi-factor is derived from value, low size, carry and low risk. In the four economic scenarios, recovery is defined as a positive three-month change in the OECD's CLI with current level below 100; expansion as a positive three-month change in CLI with current level above 100; slowdown as a negative three-month change in CLI with current level above 100; and contraction as a negative three-month change in CLI with current level below 100. Sample period is September 2005 to June 2019.

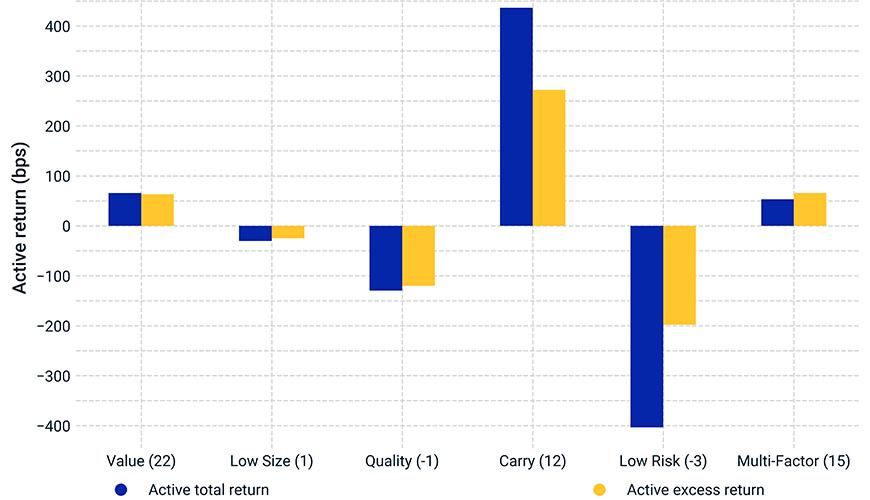

2019 was a year to keep calm and 'carry' on

We now take a look at the recent performance of indexes that track corporate-bond factor strategies. Over 2019, the MSCI USD IG Corporate Bond Index returned 14.4% (excluding transaction costs), of which 8% stemmed from the performance of rates (duration-matched Treasury return) and 6.4% was due to credit-spread return (excess return). The benchmark OAS (duration-weighted) decreased from 168 bps at the end of December 2018 to 107 bps at the end of December 2019, while Treasury yield (duration-weighted) fell from 310 bps to 245 bps during the same period. The effective duration of the benchmark increased from 6.7 to 7.5 years over the period. The low-interest-rate environment flattened the growth of new U.S. investment-grade debt issuance versus 2018, as corporate issuers took the opportunity to pay down existing debt.4

Buoyant markets led to the outperformance of the carry factor relative to all the other factors. Carry outperformed the benchmark by 437 basis points (bps), or 272 bps of excess return, having benefited from a longer spread duration and higher-yielding assets within the investment-grade universe. A multi-factor strategy derived from value, low size, carry and low risk would have benefited from diversification across factors and outperformed the benchmark by 53 bps, or 66 bps excess return, during the sample period from January 2019 to December 2019.

A carry tilt boosted returns in 2019

Active returns of long-only MSCI factor-tilted USD investment-grade corporate-bond indexes versus the MSCI USD IG Corporate Bond Index, without transaction costs (active transaction costs in bps in parentheses; negative implies transaction cost of parent index is greater than that of the factor index). Multi-factor is derived from value, low size, carry and low risk. Sample period is January 2019 to December 2019.

Overall, corporate-bond factors could potentially provide investors with insight into their fixed-income allocations. During our study period, certain factor tilts would have helped reduce risk, increase income or generate active returns in our sample portfolios. Indexes based on corporate-bond factors may also prove useful as benchmarks for active managers.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 In our research, we found that transaction costs impacted the long-term strategy performance, particularly in higher-turnover factors, such as value. For readers interested in a longer-form analysis of simulated historical fixed-income factor performance, please see: Varsani, H., Jain, V., and Mendiratta, R. 2020. “Factor and corporate bonds: Single- and multi-factor approaches to corporate credit.” MSCI Research Insight.2 See, for example: Kruger, D. “Bond Investors Worry This Is as Good as It Gets.” , Oct. 14, 2019.3 The factors discussed in the paper are drawn from the academic literature on bond factors. Roughly speaking, size is a measure of the issuance and the issuer’s outstanding debt; quality is based on credit ratings; carry is the corporate bond’s option-adjusted spread; risk is measured by the effective duration of the bond; and value is calculated as the residual spread not explained by size, risk and quality factors.4 “US Bond Market Issuance and Outstanding.” Securities Industry and Financial Markets Association.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.