Don’t confuse capital growth and asset-value growth

Blog post

March 21, 2019

How to measure real estate growth is not a simple matter. Many investors look at asset-value growth (AVG), which shows the simple change in property value. Capital growth (CG) is more complicated and nuanced, as it reflects the influence of capital expenditures (capex), which are needed to maintain and improve properties. The challenge for investors is to figure out which measure to use.

In a previous blog post, we looked at the difference between AVG and CG and where each might be appropriate, from a high level. In this post, we explore capex trends in more detail: We analyze how capex has varied over time and across markets by examining historical property-index data to look at spreads between underlying AVG and CG at various points in the real estate investment cycle. We also look at data from different markets to see what the spread was like on a country and sector level. The analysis shows that investors may want to be cautious about making blanket assumptions about capex, because there has been wide historical variation between markets.

AVG-CG SPREAD NARROWS AND EXPANDS OVER CYCLE

Since its inception in 2000, the MSCI Global Annual Property Index has produced average annual CG and AVG of 1.4% and 2.7%, respectively — a spread of 131 basis points (bps) — but the cyclical nature of real estate markets means that the spread has fluctuated over time.

Globally, the spread between AVG and CG was on a generally downward trajectory during the 2000s, before bottoming out during the global financial crisis. In the years after the crisis, as real estate markets recovered, the spread widened as capex spending picked up, peaking in 2015. This shows how the amount of capex spending has been influenced by cyclical factors.

AVG-CG SPREAD FLUCTUATED THROUGH CYCLE

Source: MSCI Global Intel

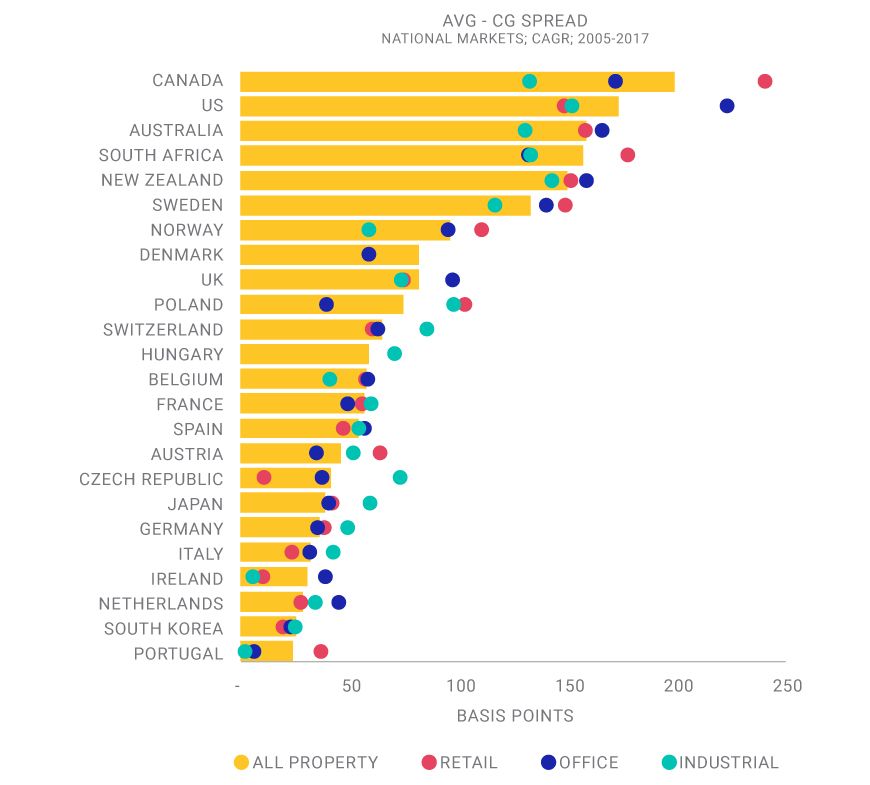

AVG-CG SPREADS HAVE VARIED ACROSS MARKETS AND PROPERTY SECTORS

Throughout the cycle, the spread between AVG and CG for the MSCI Global Annual Property Index varied between 83 and 235 basis points; but looking at individual national markets, we can observe that the spread between AVG and CG varied considerably. Part of this spread is due to different cyclical patterns at the national level. But accounting standards and market practices are also important considerations, because they influence the amount of capex and (therefore) the spread between AVG and CG.

Differences in the capex intensity of different property types can also be important. Looking at the retail, office and industrial sectors, over the full history of the MSCI Global Annual Property Index, we can see that retail assets have seen the widest spread (160bps annualized) and office assets the lowest (129bps annualized). However, within national markets, this pattern did not always hold.

Since 2005, Canada has seen the largest AVG-CG spread on aggregate. There was, however, a marked difference between the spread of its retail and industrial sectors. The U.S., on the other hand, saw its spread being driven by its office sector, while retail and industrial properties lagged — as also happened in Australia and New Zealand. Meanwhile, markets such as France, South Korea and Spain saw very little difference between the AVG-CG spread of the underlying property sectors.

To demonstrate how sector-level spreads in a country can vary, consider that Portugal (the lowest spread at an all-property level) saw a wider spread in its retail sector relative to markets such as the Czech Republic and Ireland. We can see how differences in the amount of capex, and thus the spread, can vary from country to country and between different property types in the exhibit below.

AVG-CG SPREAD VARIES ACROSS COUNTRIES AND SECTORS

Compound annual growth rate for standing investments. Source: MSCI Global Intel

CG IS MORE THAN THE CHANGE IN VALUE

What ends up in the investor's pocket as CG is often more complicated than the simple change in an asset's value. Investors may want to better understand the role of capex and the building blocks that make up CG, as well as the wide variation in capex intensity between different countries and sectors. Doing so may, in turn, help investors better understand the capex profile of their portfolios.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.