Game of Homes: Is winter coming for the domestic-equity bias?

Blog post

April 30, 2019

U.S. wealth advisers' allocation models have a considerable overweight to U.S. equities when compared to a capitalization-weighted benchmark. Although historical signals of a U.S. slowdown show signs of abating — including last month's inversion of the U.S. yield curve — asset allocators with a U.S.-equity overweight could still be exposed to additional source of equity risk: home-bias risk.

In this post, we borrow concepts from institutional-investor benchmarks and address two questions related to the risk and return of a U.S. home bias for wealth advisers: Can we quantify this risk in an allocation? And, what has happened when U.S. stocks ended previous multiyear runs of outperformance?

Return of the MAC

Model portfolios have gained traction with wealth advisers as starting points to meet clients' return objectives. At its simplest, an allocation model consists of indexes and target weights, to which tactical views and active management can be added. In this respect, a model serves a purpose similar to an institutional investor's reference benchmark.

To measure risk, we compare an allocation model with a U.S. home bias and one without, both with a moderately aggressive allocation of 60% equity and 40% fixed income. We represent the equity portion of our no-bias allocation using the MSCI ACWI IMI, which contains no home bias, and BofAML 7 to 10-year Global Government Bond Index for our fixed-income allocation. This serves as our reference allocation model throughout the exercise, with data as of February 2019.

We next impose a 15% overweight to U.S. equities, funded by a 10% and 5% underweight to international and emerging-market stocks, respectively. This serves as our home-biased allocation model.

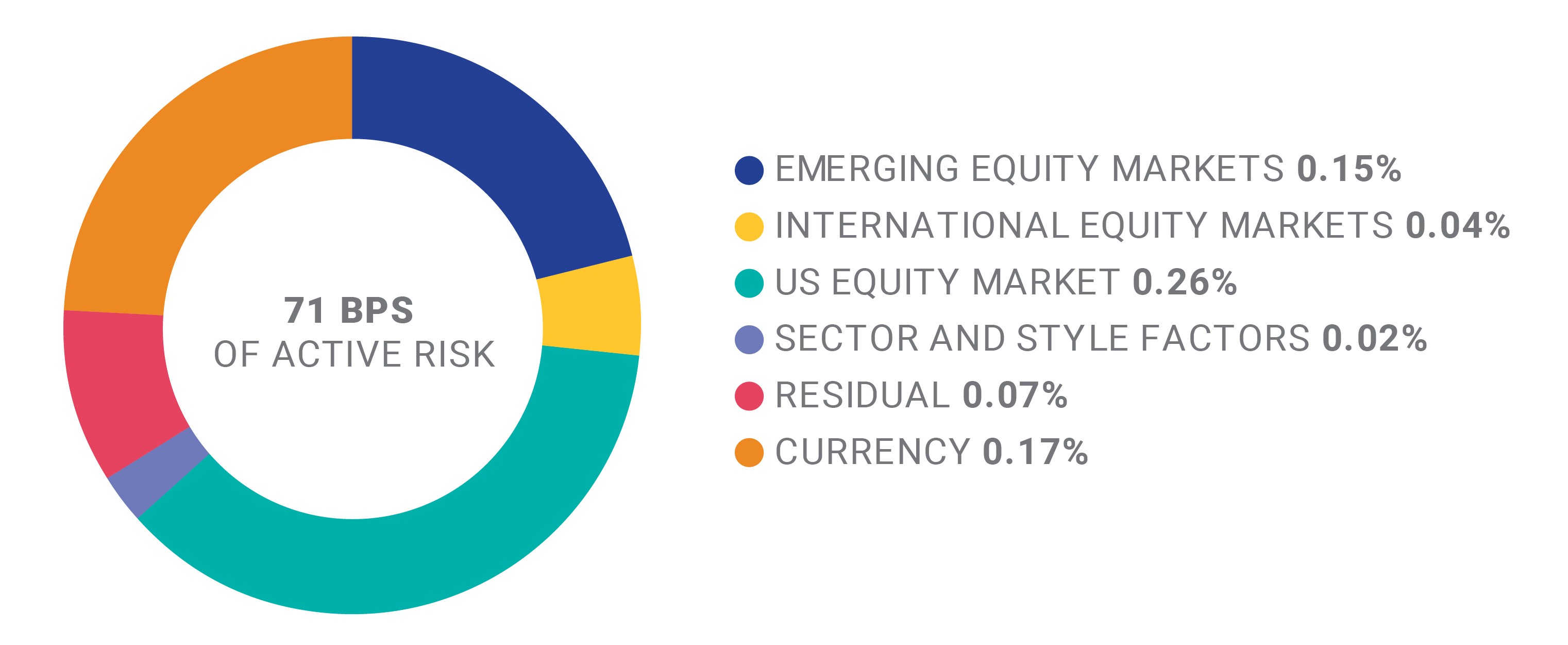

Our first comparison attributes the active risk of the home-biased model to the reference allocation model, using the MSCI Multi-Asset Class Factor Model (MAC). Risk models link our hypothetical decision (overweight the U.S.) to an investment outcome (active risk). The results are shown below.

Home-bias added significant active risk

The exhibit above likely gives pause: Home bias alone added over 70 basis points (bps) of active risk. This is before

any active managers are added or any tactical views to the equity or fixed-income allocations are implemented.

A bias toward U.S. equities also introduced this market's overweights to certain sectors, such as information technology and financials, and to style factors, such as momentum. Yet, the active risk due to sectors and style factors (the exhibit's orange region) was dwarfed by that of country decisions (the exhibit's blue regions).

But did country decisions influence returns?

What's gone up has come down

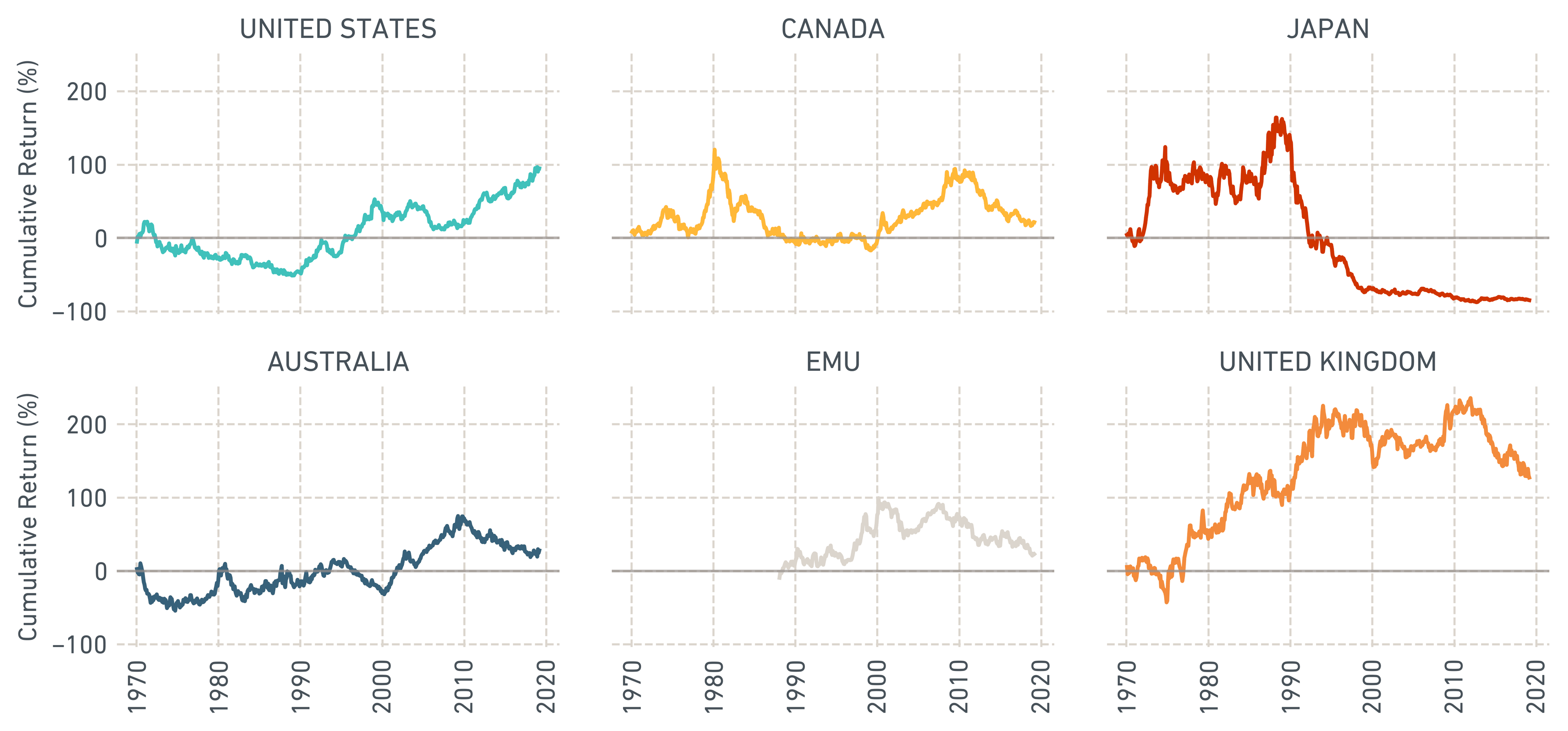

Before we can answer that, let's look in more detail at historical home biases around the world. Below, we plot returns to a 100% home bias for the major developed markets. Each plot can be interpreted as the relative return of the respective representative country index (i.e., the MSCI USA IMI) over one covering the rest of the world (i.e., the MSCI World ex USA IMI).

Over the last two decades a U.S. bias showed significant outperformance, albeit with periods of sharp declines. This cyclicality was closely correlated with the broad equity market, as well as commodity and real estate returns.

But a different picture emerges when looking at the deeper history and across markets. When the U.S. suffered an extended stock slump during the 1970s to the 1990s, Japanese stocks soared, and then gave back all their gains during the subsequent decades. Canada's stock market suffered through a rapid rise and fall during the early 1980s.

Country-specific rallies have come with drawdown risk

Home-bias return calculated as the difference in return of the MSCI country index and the MSCI World index excluding that country, in local currency terms. Data for all indexes begin in January 1970 and end in February 2019, except for the EMU region, which begins in January 1988.

Examining the last time the U.S. underperformed international markets

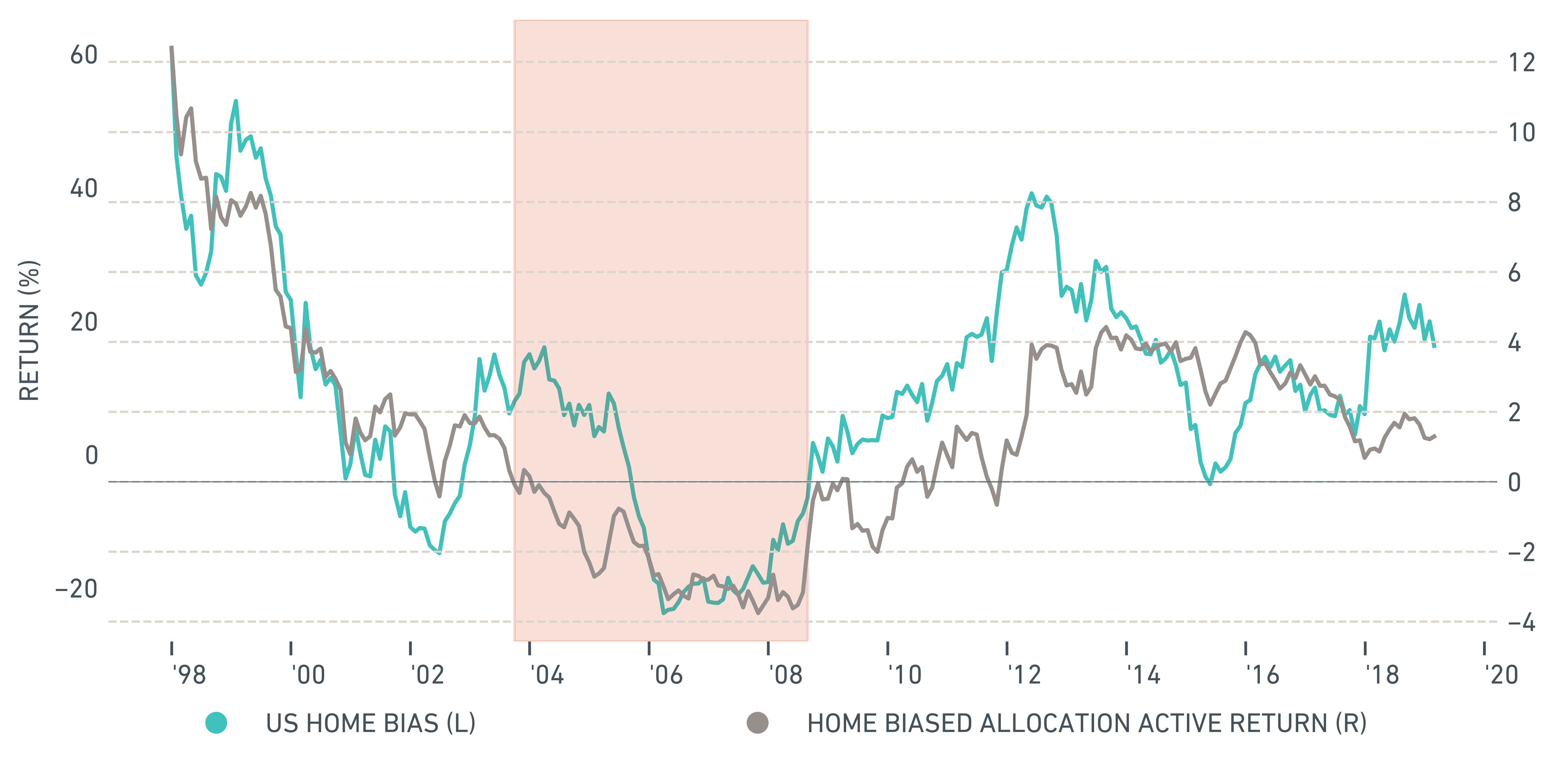

To quantify how much the home-biased allocation trailed the reference allocation, we use a recent period of drawdown in the U.S. home bias.

The exhibit below shows the rolling three-year returns for the U.S. home bias and the rolling three-year returns relative to the reference allocation model, from January 1995 to February of 2019. As expected, the two return patterns were closely related.

The highlighted portion, following the dot-com bubble through the financial crisis of 2008, corresponds to an extended period when U.S. stocks trailed international stocks. By mid-2008, they had fallen behind by 20%. The home-biased allocation model followed suit, trailing the reference model by 4% at its trough.

Over the course of this five-year period, the home-biased model trailed the reference allocation model by 70 bps annually, with 100 bps of active risk, comparable to the level of active risk highlighted in the first exhibit.

Rolling 3-year return of U.S. home bias vs reference allocation model

Returns are cumulative rolling over the prior three-years. The home-biased allocation return (gray) is relative to the reference allocation.

Equity allocations with significant U.S. bias have enjoyed a long summer of outperformance. But history has shown that winds can shift and grow cold, and usher in an extended winter of negative relative returns.

The author thanks Limin Xiao and Andrew DeMond for their contributions to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 Hube, K. “Asset Picks From Top Wealth Management Firms.” Barron’s, March 26, 2016.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.