Global small-cap fund capacity: no small matter

Blog post

June 15, 2017

In recent years, pension funds around the world increasingly have shed their home bias and made global small-cap allocations. As we noted in our last post, institutional investors have been driven by several reasons: the long-term historical premium offered by small caps, a diversification benefit and the ability to reflect the complete opportunity set. However, pension funds still fall well short of the 14% global small-cap weighting found in the MSCI ACWI IMI.

Even as pension funds move toward the 14% small-cap target allocation, they face a potential roadblock: There are not enough small-cap funds investing outside the U.S. to meet potential institutional demand. Pension funds may need to look at both indexed and active managers to fill what we calculate could be nearly a $750 billion gap in non-U.S. small-cap equity fund capacity.

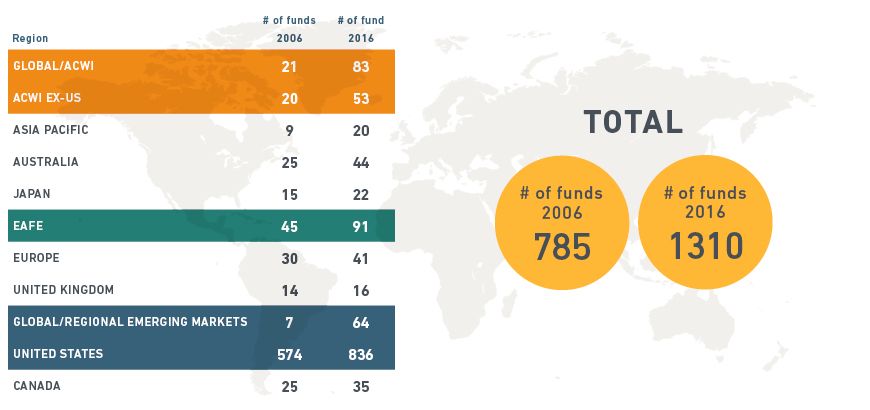

In the decade from 2006 to 2016, there was striking growth in the number of institutional small-cap funds available globally, according to the Evestment database. However, it is clear that U.S. small-cap funds still dominate the global landscape, accounting for nearly two-thirds of total institutional small-cap funds.

The global small-cap funds landscape

Source: Evestment as of December 2016

While it appears that there is adequate capacity available in open U.S. small-cap funds to absorb potential demand, the shortfall may occur in funds that invest in smaller stocks outside the U.S. We have tried to estimate this shortfall.

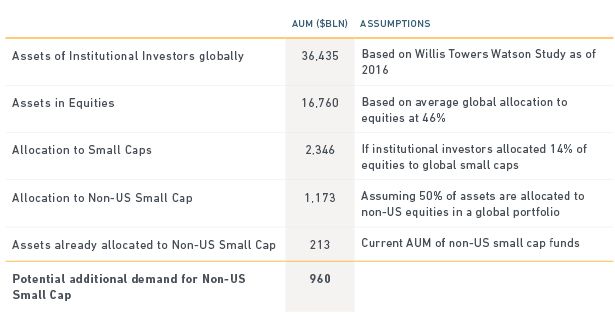

First, we tried to calculate the potential demand based on a 14% equity allocation to global small cap. Based on $36.4 trillion in total pension assets, we find that their global small-cap allocation would have been $2.346 trillion at year-end 2016 (see our assumptions in the below table). Pension funds would have allocated about half of that figure — or $1.173 trillion to non-U.S. small cap funds. From that figure, we net out $213 billion that pension funds have already invested in active non-U.S. small cap funds. The resulting net demand is $960 billion.

Potential pension fund demand for non-U.S. small-cap equities

Source: Evestment as of December 2016; Willis Towers Watson Study 2016

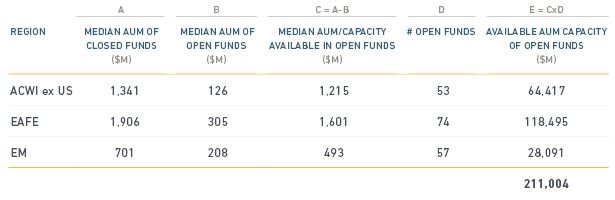

How does the capacity needed to meet this potential demand compare to the capacity now available in open global small-cap funds? To calculate needed capacity, we assume that all open funds (of various types) will close at the same level of assets as other closed funds in their region. By multiplying the median available capacity of open funds by the number of open funds, we calculate there is $211 billion in available capacity. Subtracting this figure from the $960 billion figure, pension funds could face a $750 billion shortfall in available capacity to meet the 14% average global allocation to small-cap stocks. (The $750 billion figure is an estimate of the shortfall assuming pension funds allocated only to active non-U.S. small cap funds. Pension funds also might opt to implement through other vehicles, such as indexed approaches, exchange-traded funds or separate accounts, reducing the potential shortfall.)

Non-US Small Caps: Available Capacity

We assume open funds will close at the same levels as closed funds in each region. We estimate the potential available capacity of open funds for each region by subtracting what has already been allocated to open funds from the assumed median level.

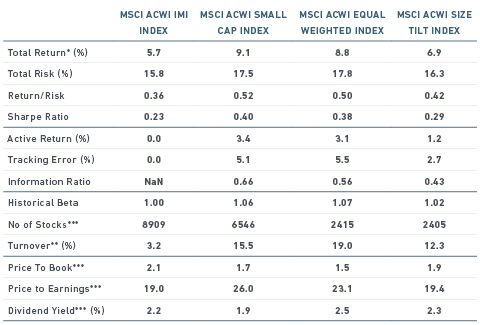

There are two key ways to bridge the gap: Asset managers can launch more active funds or pension funds can use indexed vehicles that aim to replicate available indexes such as MSCI's suite of global small-cap indexes. Our previous research shows that replicating such indexes have offered effective and investable ways of obtaining exposure to the size premium. Over the past 20 years, these indexes have produced excess returns over MSCI ACWI IMI, with superior risk/reward and Sharpe ratios. Characteristics of these indexes can be seen below.

Global Small-Cap Index options

Period: 31 Dec 1998 to 31 Mar 2017

*Gross returns annualized in USD

The scarcity of available funds for pension funds looking to invest in small-cap equities outside the U.S. has created opportunities for both active and indexed managers. Now, it's up to asset managers to bridge the gap.

Further reading:

Why global small-cap stocks are becoming an important part of institutional portfolios

How to think bigger about small cap investing

One size does not fit all

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.