Have High-Yield ETFs Created Liquidity Risk?

Blog post

March 27, 2019

In the fourth quarter of 2018, redemptions of high-yield ETFs soared to approximately 25% of these funds' assets under management (AUM), according to data provider IHS Markit. This wave of redemptions provided an opportunity to assess the strength of liquidity in the high-yield market — a portion of the fixed-income universe where there's less transparency and market participants may be more likely to affect spreads through purchases and sales. So what can bond investors glean from the fourth-quarter selloff about whether high-yield-bond ETFs pose liquidity risk? Our analysis suggests that concerns over high-yield ETFs and liquidity risk may be overblown.

LIQUIDITY MISMATCH FOR INVESTORS AND INTERMEDIARIES

Investors buy and sell ETFs in a comparatively liquid and transparent way: by trading on exchanges. But market intermediaries such as authorized participants use the less transparent and less liquid over-the-counter (OTC) market for transactions in individual bonds. ETF investors may close their positions during market selloffs, with the result that intermediaries may offload their holdings into the OTC market. If the market in high-yield bonds isn't liquid enough to absorb the increased supply, bond investors could face a liquidity shortage that exacerbates the market selloff.

ETFs currently account for slightly more than 2.7% (or a total of USD 34 billion invested) of the high-yield-bond market, according to IHS Markit data. But could investor redemptions of even 5% of that amount have a significant impact on the high-yield market, which has a daily average trading volume of approximately USD 7 billion?

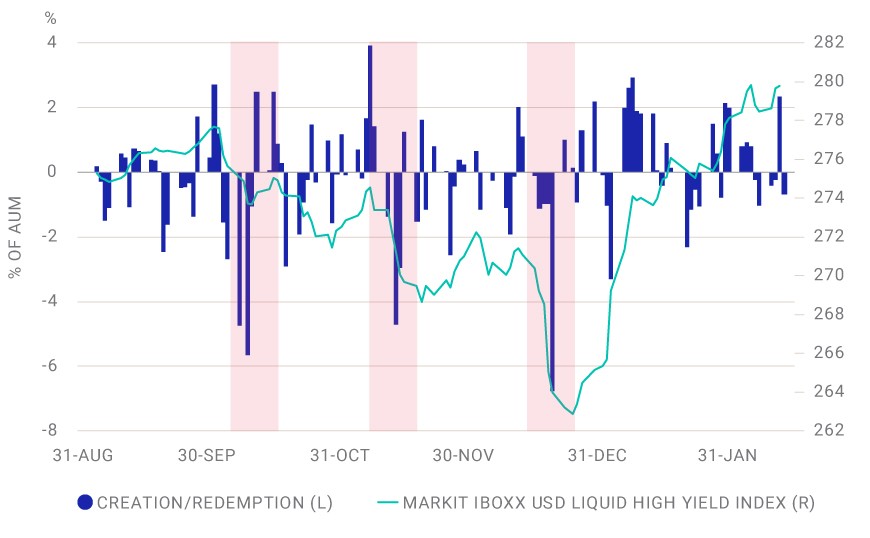

ETF REDEMPTIONS SPIKED IN RESPONSE TO MARKET SELL-OFFS

ETF REDEMPTION WAVE TESTED HIGH-YIELD LIQUIDITY

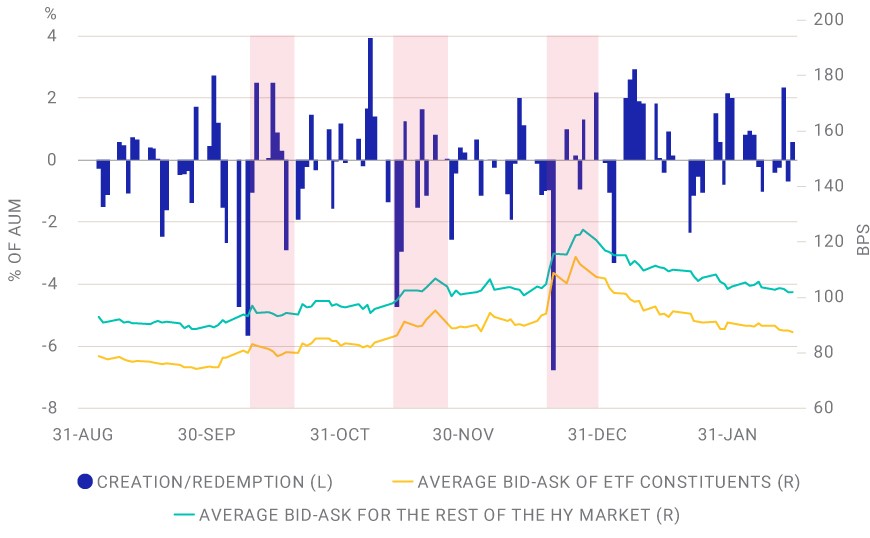

The bid-ask spread generally widened in the high-yield sector during the fourth quarter, as credit spreads widened and market volatility increased. But how much of this bid-ask widening might have resulted specifically from ETF redemptions?

In looking at the fourth-quarter sell-off, we focused on four days — Oct. 8 and 10, Nov. 14 and Dec. 21 — when net redemptions of high-yield ETFs exceeded 4.5% of AUM, according to IHS Markit. Each of these days immediately followed trading days with significant negative price returns in the broad high-yield market, as shown in the exhibit above.

To isolate the effect of ETF redemptions on bid-ask spreads — i.e., to gauge high-yield ETFs' liquidity risk — we looked at the high-yield bonds held in ETF portfolios, while we used non-ETF high-yield bonds as our control group. If ETF redemptions did result in significant liquidity deterioration, we would expect the ETF constituents to experience more bid-ask widening than the non-constituents during periods with large amounts of redemptions.

On three of the days, there was minimal difference in bid-ask impact on the ETF and non-ETF constituents. On Dec. 21, however, the bid-ask difference did narrow moderately (from 14 to 7 basis points), suggesting ETF redemptions had some impact on liquidity during the subsequent period.

ETF REDEMPTIONS' MINIMAL EFFECT ON HIGH-YIELD HOLDINGS

In sum, heavy redemptions of high-yield ETFs during the fourth quarter do not appear to have had a large impact on the constituent bonds' bid-ask spreads. On balance, we interpret the data as suggesting that redemptions did not generally result in impaired liquidity in the high-yield-bond market. Nevertheless, looking forward, investors may want to pay attention to ETF redemption levels, since redemption spikes could have an impact on bond-market liquidity in highly stressed conditions.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.