Home bias in fixed income: Has it helped or hurt?

Blog post

July 29, 2019

- Asset allocators for defined-benefit plans must decide whether to allocate between domestic or global bonds in their overall asset mix — and, if globally diversified, whether to hedge the currency or not.

- Our empirical analysis finds that investing in domestic bonds dominated as a strategy if the goal was to minimize risk versus a fixed-liability benchmark denominated in the local currency.

- Portfolios with higher allocations of global bonds had higher "active risk," defined as the volatility of tracking error (or return difference) between the portfolio and liability benchmark.

Home, sweet home

DB plans promise fixed, long-term payments (often inflation-adjusted) in local currency to plan members at retirement. For DB plans, these payments represent liabilities that resemble fixed-income portfolios. This resemblance is an important consideration when building a liability-driven investment (LDI) strategy: The portfolio reflects the nature of liabilities, and a tilt toward the domestic fixed-income market may be a logical choice.

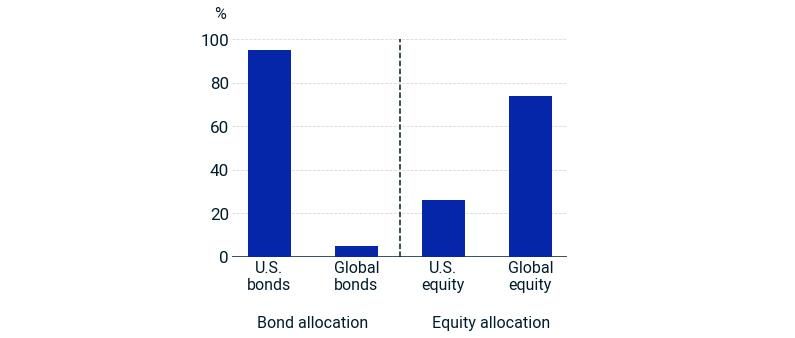

When we looked at the 20 largest U.S. DB plans, we found that their asset allocations showed two distinct patterns: home bias for bonds and global diversification for stocks, according to recently available financial reports.1 Plan investments in public assets typically pursued the well-known allocation strategy of 60% equity and 40% fixed income. Within the fixed-income portfolio, about 95% of the allocation was in domestic government and credit sectors, while the remaining 5% was invested globally. In contrast, in the equity portfolio, 74% of the allocation was linked to global benchmarks, demonstrating that country diversification played an important role in allocating equity assets.2

US pension plans showed pervasive home bias in fixed income, but not in equities

Yes, total risk was higher for the US bond portfolio, but ...

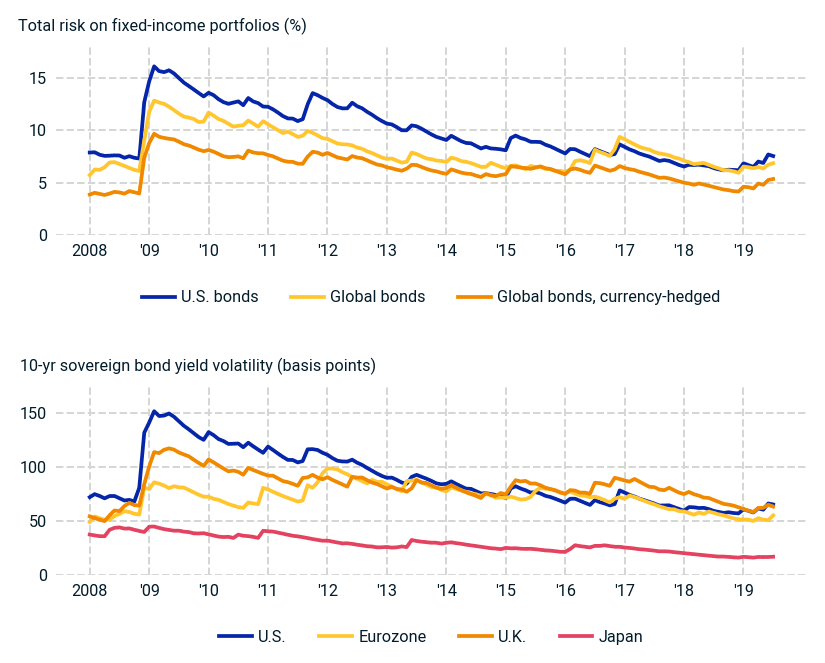

We used MSCI yield curves to quantify ex-post return volatility (or total risk) of a hypothetical U.S. Treasury portfolio and currency-hedged and -unhedged global government portfolios, between January 2008 and May 2019.3 These portfolios were chosen to hedge out the interest-rate exposure of an assumed liability benchmark.4 The currency-hedged global fixed-income portfolio consistently displayed lower total risk (see the exhibit below), and the U.S. Treasury portfolio generally had higher total risk.

The U.S. portfolio's higher risk partly reflected U.S. bonds' generally higher historical yield volatility. Additionally, in the global portfolios, yields in one country did not always move in the same direction as those in other countries. This lack of correlation between different countries' yield curves further reduced the total risk of the global portfolios.

US bond portfolio generally had higher total risk than global portfolios

... active risk may matter more

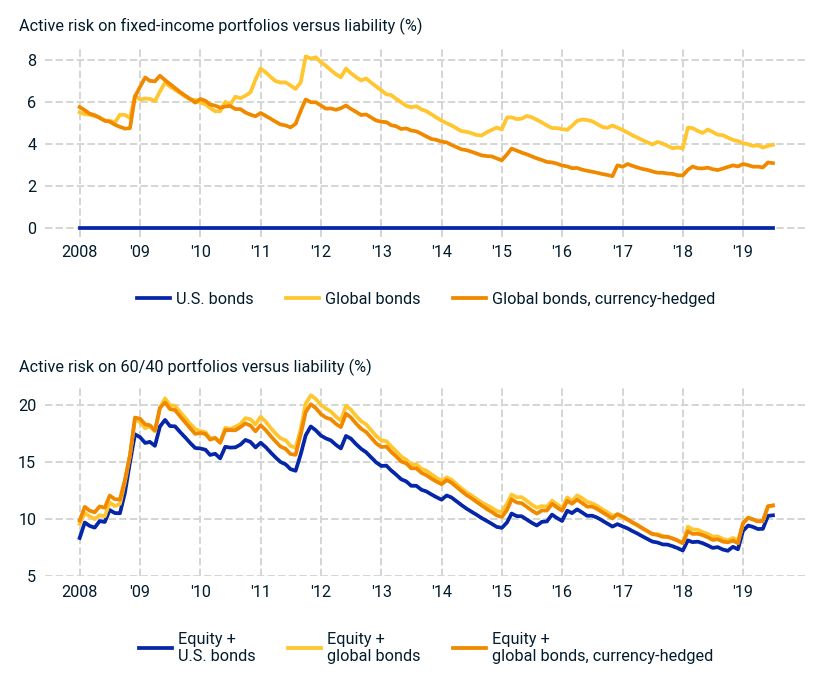

Lower total risk is not always a good thing. Indeed, active risk may be the more important risk metric for DB plans managing against a liability benchmark.

Over the time period of our analysis, our backtests show that home bias in pension plans' fixed-income allocations consistently resulted in lower ex-post active risk. The active risk of the global fixed-income portfolios ranged from 250 basis points (bps) to almost 800 bps (see exhibit below). In contrast, the U.S. Treasury portfolio exactly hedged the liability benchmark, resulting in zero tracking error.

We then looked at active risk on multi-asset-class portfolios with 60% allocated to global equities and 40% to fixed income.5 The allocation toward U.S. fixed income again consistently resulted in lower active risk. In short, home bias in fixed-income investing reduced active risk when managing assets measured against a liability benchmark consisting of fixed cash flows denominated in local-market currency.

Active risk was lower when using US bonds

One last note

Our analysis has focused on risk minimization, but asset allocators may also have views on expected returns of global versus domestic bonds. Allocators who believe global bond markets offer value over the domestic market might weigh the return benefit against the increase in active risk. Such allocators may still prefer to invest only in the domestic market to avoid breaches of the portfolio risk budget.

1 The sample consisted of 15 public pension plans and five private plans headquartered in the U.S.

Source of fund ranking: "The P&I/Thinking Ahead Institute World 300." Pensions & Investments, Sept. 3, 2018.

Source of allocations: MSCI, based on plans' reported data from 2017 and 2018. 2 Global equity benchmarks usually include U.S. securities as well. 3 We computed monthly returns and return volatilities from MSCI's country-specific government-bond yield curves. Our global bond portfolios used fixed country weights of 40% for the U.S., 29% for Japan, 24% for the eurozone and 7% for the U.K. For the eurozone countries, we assumed an equal weighting of 6% for France, Germany, Italy and Spain. We computed volatilities and risk using exponential time decay with a half-life of one year. The analysis assumes monthly rebalancing and currency hedging through the use of one-month forward contracts on foreign exchange. 5 Equities are represented by the MSCI ACWI Index.

Source of fund ranking: "The P&I/Thinking Ahead Institute World 300." Pensions & Investments, Sept. 3, 2018.

Source of allocations: MSCI, based on plans' reported data from 2017 and 2018. 2 Global equity benchmarks usually include U.S. securities as well. 3 We computed monthly returns and return volatilities from MSCI's country-specific government-bond yield curves. Our global bond portfolios used fixed country weights of 40% for the U.S., 29% for Japan, 24% for the eurozone and 7% for the U.K. For the eurozone countries, we assumed an equal weighting of 6% for France, Germany, Italy and Spain. We computed volatilities and risk using exponential time decay with a half-life of one year. The analysis assumes monthly rebalancing and currency hedging through the use of one-month forward contracts on foreign exchange. 5 Equities are represented by the MSCI ACWI Index.

Further Reading

Subscribe todayto have insights delivered to your inbox.

4 Interest-rate exposure is represented by the key-rate duration profile of the liability benchmark. We assumed the liability benchmark had a duration of 12 years and exposure to only U.S. term-structure risk.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.