How COVID-19 could impact private real estate values

Blog post

April 20, 2020

- Longer investment horizons and a reliance on appraisals may mean that private real estate does not react to shocks as rapidly as public markets. However, this does not mean the asset class is immune to those shocks.

- As the COVID-19 pandemic continues to take its human toll and disrupt global economies, many real estate investors have been seeking to understand what impact the crisis could have on their portfolios.

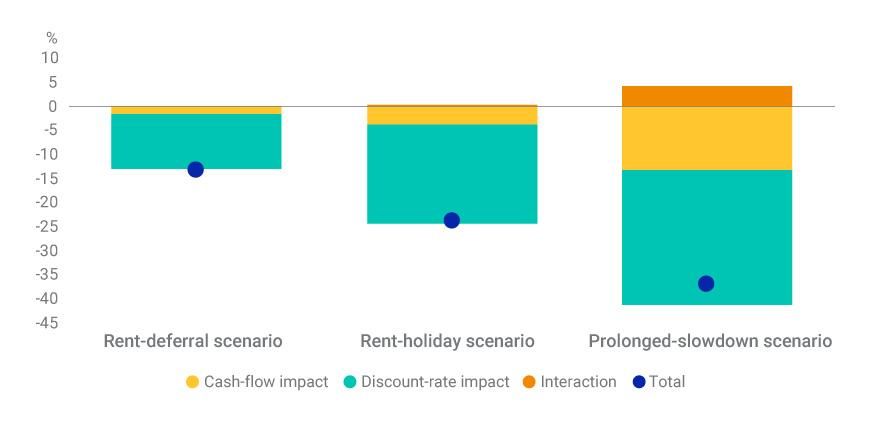

- We used MSCI's Valuation Scenario Model to show how discounted-cash-flow models could be used to explore the impact the crisis could have on asset values. In the hypothetical scenarios we created, asset values declined between 13% and 37% highlighting how sensitive the outcomes can be to changes in assumptions.

Defining and comparing discounted-cash-flow scenarios

To demonstrate this approach, we define several hypothetical scenarios in the MSCI Valuation Scenario Model and compare them against the result of a hypothetical base case. The MSCI Valuation Scenario Model is a DCF-based tool. It derives cash flows based on growth expectations over short, medium and long horizons, which follow an auto-regressive process with mean-reverting features and discounts forecast cash flows with the expected risk-free rate and risk premium. By comparing valuations from scenarios with varying projections for growth and discount rates, the model analyzes the impact of growth shocks and discount-rate shocks on valuations.

Much of the media's discussion to date has focused on the negotiations taking place between tenants and landlords and the potential for landlords to grant tenants relief in the form of rent deferral or rental holidays. For that reason, we have built our scenarios around these possibilities.

- In the base case, cash flows are assumed to grow at 3% per year and are discounted with a risk-free rate of 1% and a risk premium of 6%.

- In the first hypothetical scenario, we model a rent deferral where 95% of cash flows from the first six months are deferred. The risk-free rate falls to 50 basis points (bps), but the risk premium increases to 7%.

- In the second hypothetical scenario, we model a rent holiday with the same 95% reduction in cash flows over the first six months but the foregone income is not recovered. The risk-free rate falls 50 bps, but the risk premium increases to 7.5%.

- The final hypothetical scenario is the same as the rent holiday, but we model a more prolonged slowdown by reducing medium-term growth to 2% and increasing the risk premium to 8%.

Comparing the hypothetical scenarios to the base case shows the potential impact on asset values

Scenario | Total | Cash-flow impact | Discount-rate impact | Interaction |

|---|---|---|---|---|

Scenario Rent deferral | Total -13% | Cash-flow impact -2% | Discount-rate impact -12% | Interaction 0% |

Scenario Rent holiday | Total -24% | Cash-flow impact -4% | Discount-rate impact -21% | Interaction 0% |

Scenario Prolonged slowdown | Total -37% | Cash-flow impact -13% | Discount-rate impact -28% | Interaction 4% |

The cash-flow impact and discount-rate impact are not linear, so they will not always sum to the total. This difference is captured in the interaction term. Source: MSCI Valuation Scenario Model.

One thing to note in this analysis is that, while much of the public discussion to date has focused on the potential short-term disruption to income, the cash-flow impacts from the rent-deferral and rent-holiday scenarios, as modeled, are relatively small. Reductions to longer-term cash-flow expectations or changes to the discount rate had a much bigger impact on the results. This illustrates why some may want to consider what effects these variables could have on portfolios, in addition to the immediate disruptions to near-term cash flows.

Addressing uncertainty

With the situation evolving rapidly, there is still much uncertainty about how the crisis will impact the cash flows of real estate assets and financial-market conditions.

The above scenarios are not meant to be predictions, but to illustrate how investors can use tools like the MSCI Valuation Scenario Model to explore how sensitive a portfolio might be to changes in assumptions about growth and discounting. This sort of approach could be applied to the overall portfolio, but also to different segments within a portfolio. For example, the office exposure could be analyzed separately to the retail exposure, or the analysis could be applied to individual assets. In defining scenarios for this kind of analysis, investors can draw on their own internal underwriting assumptions, but the use of historical market data may also be helpful. It could be used to either define scenarios based on previous shocks or contextualize the assumptions applied to the current crisis.2

Further Reading

Subscribe todayto have insights delivered to your inbox.

1For example, in 21 national market corrections we explored, the median peak-to-trough timing was 3.5 years. Reid, B. “What’s the downside in real estate?” MSCI Blog, Oct. 4, 2019.2For an example of how historical data can be used to provide context to scenarios, see: Reid, B. “What out of-of-cycle write-downs may mean for real estate yields.” MSCI Blog, April 3, 2020.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.