How e-commerce is reshaping the future of retail properties

Blog post

March 13, 2018

Although e-commerce has disrupted industries once considered staples in retail properties, certain retail assets are thriving. Simply put, some goods and services cannot be purchased over the internet: Working out at a fitness center or dining at a restaurant cannot be replicated by online transactions. And while some companies sell groceries online, most food shopping still takes place in stores. Our findings show that experience-oriented tenants, such as movie theaters and restaurants, and internet-resistant retailers, such as supermarkets, dominated the top-performing retail assets in 2017.

In a recent paper,1 we examined the extent to which ecommerce is affecting the investment returns from retail assets across the U.S. We found that recent returns were similar across retail property segments,2 suggesting that any impact ecommerce may have had is lost in these broad market averages. Here, we use MSCI data to examine the relationship between a retail asset's tenant mix (e.g., apparel, restaurants) and its corresponding total return. If the retail segment wasn't a significant driver of relative return in 2017, was tenant exposure the catalyst?

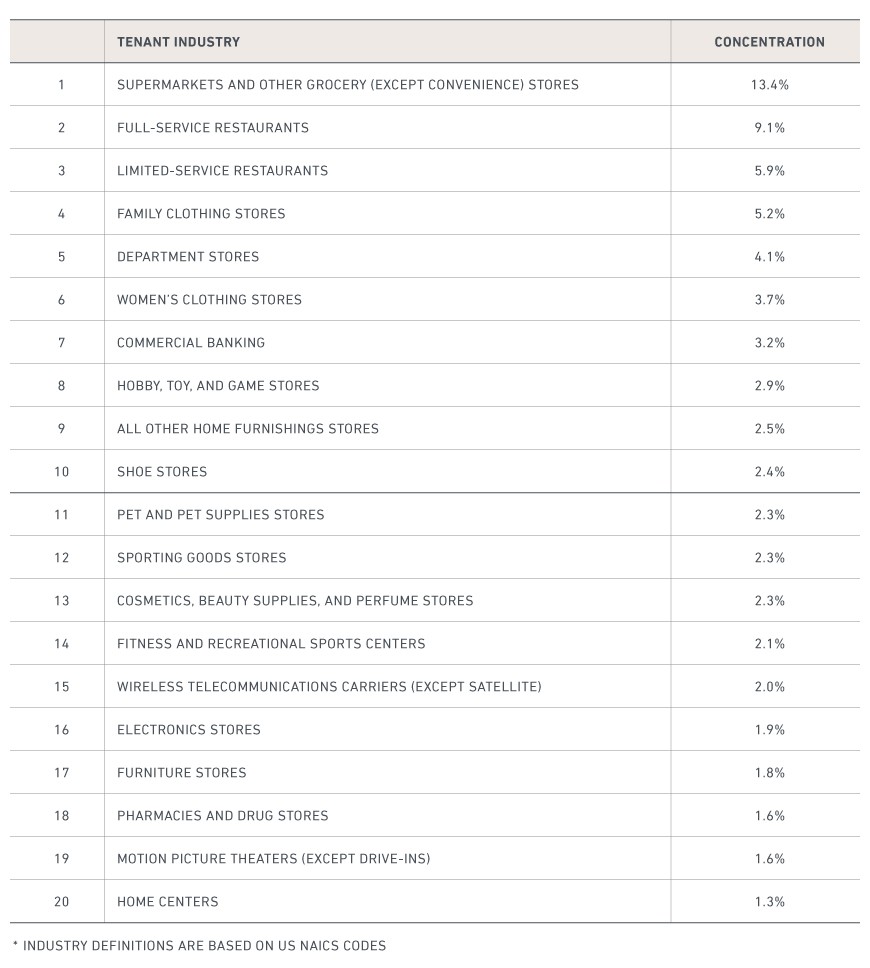

First, let's identify which industries prevailed among retail assets. The exhibit below shows the top 20 tenant industry concentrations based on total revenue across this data set of retail properties.3 Supermarkets, restaurants and apparel dominated the top 10, with fitness centers and movie theaters making the top 20.

Top 20 tenant industries within retail properties

Source: MSCI IRIS, PAS. Based on December 2017 revenues for super/regional malls, community/neighborhood centers and power centers.

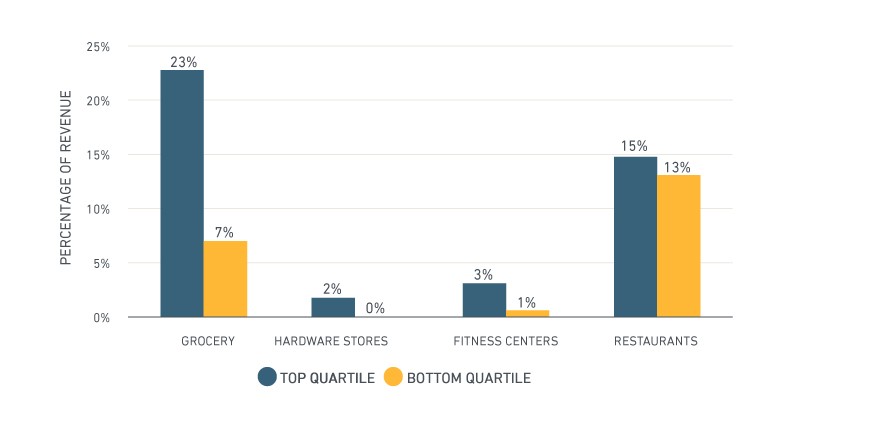

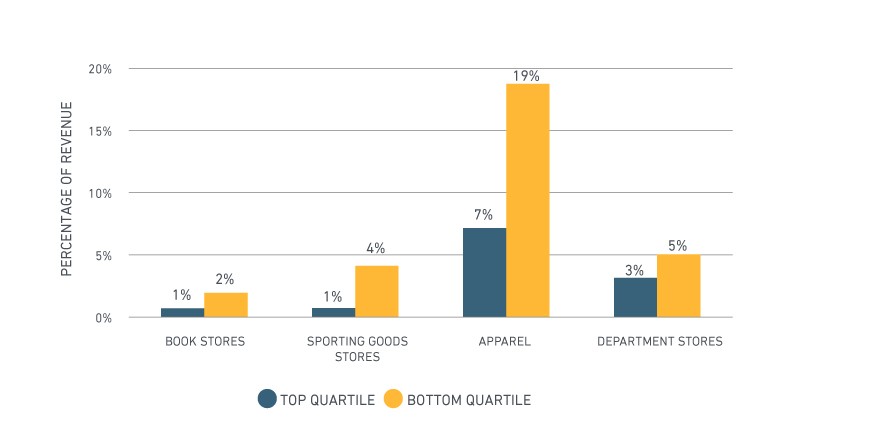

The share of certain tenant types varied strikingly between the best- and the worst-performing assets, as seen in the next exhibit. In the first exhibit, we see that top-quartile assets derived more revenue from experience-oriented and internet–resistant industries such as restaurants, fitness centers and supermarkets. Grocery exposure, in particular, seemed to produce a significant difference in asset performance. Online penetration in this sector has so far remained low in the U.S. Conversely, we see in the second exhibit that industries more vulnerable to online competition were prevalent in the bottom quartile. Unsurprisingly, apparel comprised a large proportion of under-performing industries for bottom-quartile assets.

Retail industries where over exposure is associated with asset outperformance

Source: MSCI IRIS, PAS. Based on December 2017 revenues for super/regional malls, community/neighborhood centers and power centers. Quartiles based on 2017 one-year asset total returns

Retail industries where over exposure is associated with asset underperformance

Source: MSCI IRIS, PAS. Based on December 2017 revenues for super/regional malls, community/neighborhood centers and power centers. Quartiles based on 2017 one-year asset total returns

Implications for retail owners and landlords

We observe three key characteristics among top-quartile retail properties:

• Internet Resistance: The top quartile had a smaller exposure to book, sporting goods and apparel stores. These industries have experienced the most penetration from online retail. Conversely, the best-performing retail formats had higher exposure to grocery stores. Grocery tenants attract the everyday shopper and increase the frequency of shopping center visits.

• Restaurants: Restaurants were an important segment for shopping centers and represented 15% (full-service restaurants accounted for 8.5%) of the total revenue for the top quartile versus 13% (full-service: 8.1%) for the bottom quartile. Restaurants, particularly full-service, are a popular tenant as they attract traffic and keep consumers at shopping centers longer.

• Entertainment and Leisure: While top-quartile assets included a higher concentration of fitness centers than the bottom quartile, entertainment establishments are increasingly becoming an important element in shopping centers because of the experience they offer consumers.

The data shows that for retail properties to succeed, consumers need a compelling reason to visit. For some assets, this may mean focusing on convenience and necessity where the online offer is less attractive such as grocery and hardware. For others, the solution may be to evolve from simple retail properties into shopping, dining and entertainment centers. Increased foot traffic and time spent at properties provide opportunities for retailers to interact with their customers on a deeper, more experiential level rather than simply providing a transactional environment.

While this analysis is based on U.S. data, similar trends are affecting real estate performance around the globe. The ability to understand the interaction between lease and tenancy dynamics and overall investment performance potentially may be increasingly important as the industry evolves over the coming years.

1 "Retail Apocalypse: Should Mall Owners be Worried?" MSCI Research Insight.

2 Super/regional malls, community/neighborhood centers and power centers

3 Retail properties for which there is full year 2017 performance data as well as IRIS tenancy information

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.